Zoom Video Communications Stock Price Falls 12% – Time to Buy ZM Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Zoom Video Communications (ZM) stock was trading almost 12% lower in US premarket price action today after reporting its fiscal second-quarter earnings. The post-earnings volatility is quite common for the video calling company and it tends to rise or fall sharply after the earnings report.

Even before the crash today, Zoom stock is down 3% for the year and is underperforming the markets by a wide margin. While US stock markets are near their all-time highs, it’s been a different story for the so-called “stay-at-home” stocks which are trading at a steep discount to their 52-week highs. What’s the forecast for Zoom shares after the massive underperformance and should you buy ZM stock now?

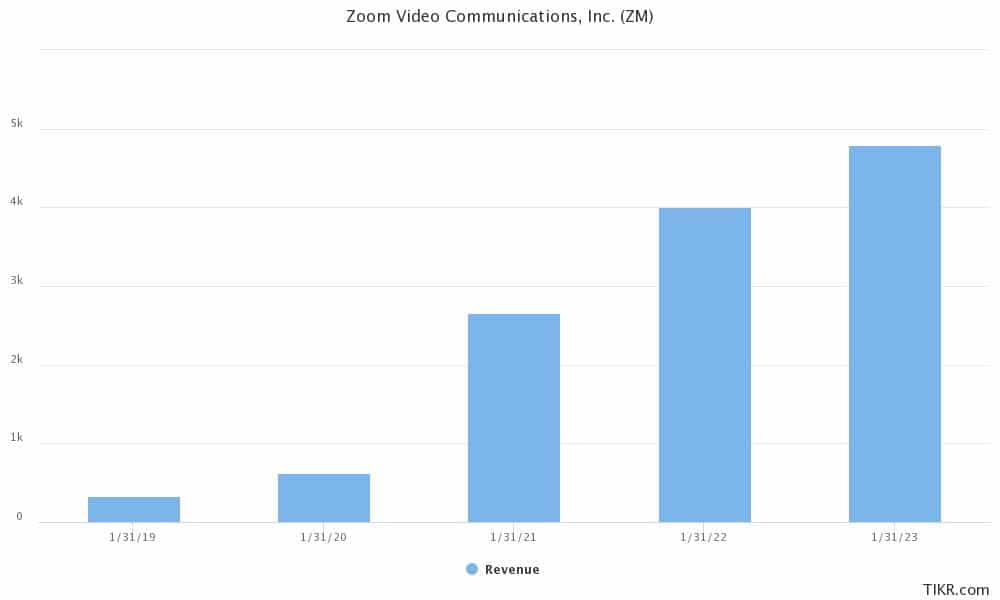

Zoom earnings

Yesterday Zoom released its fiscal second-quarter 2022 earnings for the quarter that ended in July. The company reported revenues of $1.02 billion in the quarter which were ahead of what analysts were expecting. The revenues were also higher than the $985-$990 million that Zoom had guided for during the first-quarter earnings call. Notably, during the quarter, it reached the milestone of $1 billion quarterly revenues for the first time in its history.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Stay-at-home winner

The video calling company has come a long way since its IPO in 2019. The COVID-19 pandemic, and the resultant lockdowns, helped propel the demand for companies like Zoom. However, sales growth rates for the pandemic winners are coming down. Recently, Fiverr stock had also tumbled after it warned of a growth slowdown. Even FAANG names are not immune to the growth slowdown and Amazon and Netflix had also fallen after the second-quarter earnings release after they said that growth in the back half of 2021 would slow down.

Zoom price guidance was below expectations

Zoom’s earnings were better than expected on both the topline as well as the bottomline. However, its guidance spooked investors. For the fiscal third quarter, the company gave revenue guidance of $1.015-$1.020 billion. The guidance was barely in line with street estimates, which often tend to be conservative. Zoom expects to post an adjusted EPS of $1.07-$1.08 in the current quarter which is slightly below the $1.09 that analysts polled by Refinitiv were expecting.

Meanwhile, after the strong performance in the fiscal second quarter, Zoom also raised the forecast for the full year. It now expects to post revenues between $4.005-$4.015 billion in the year which was in line with estimates. The previous guidance called for fiscal 2022 revenues between $3.98-$3.99 billion.

Morgan Stanley

Interestingly, earlier this month, Morgan Stanley had issued a bullish note on Zoom and had said that slowdown concerns are overblown. “While we think that Zoom is certainly building a durable platform for growth, our call is less on the multiyear durability of the platform or LT competition threats and more about overdone concerns currently on SMB (small and medium business) churn against a backdrop of investors who want to be more positive,” it had said in its note.

Zoom stock price forecast

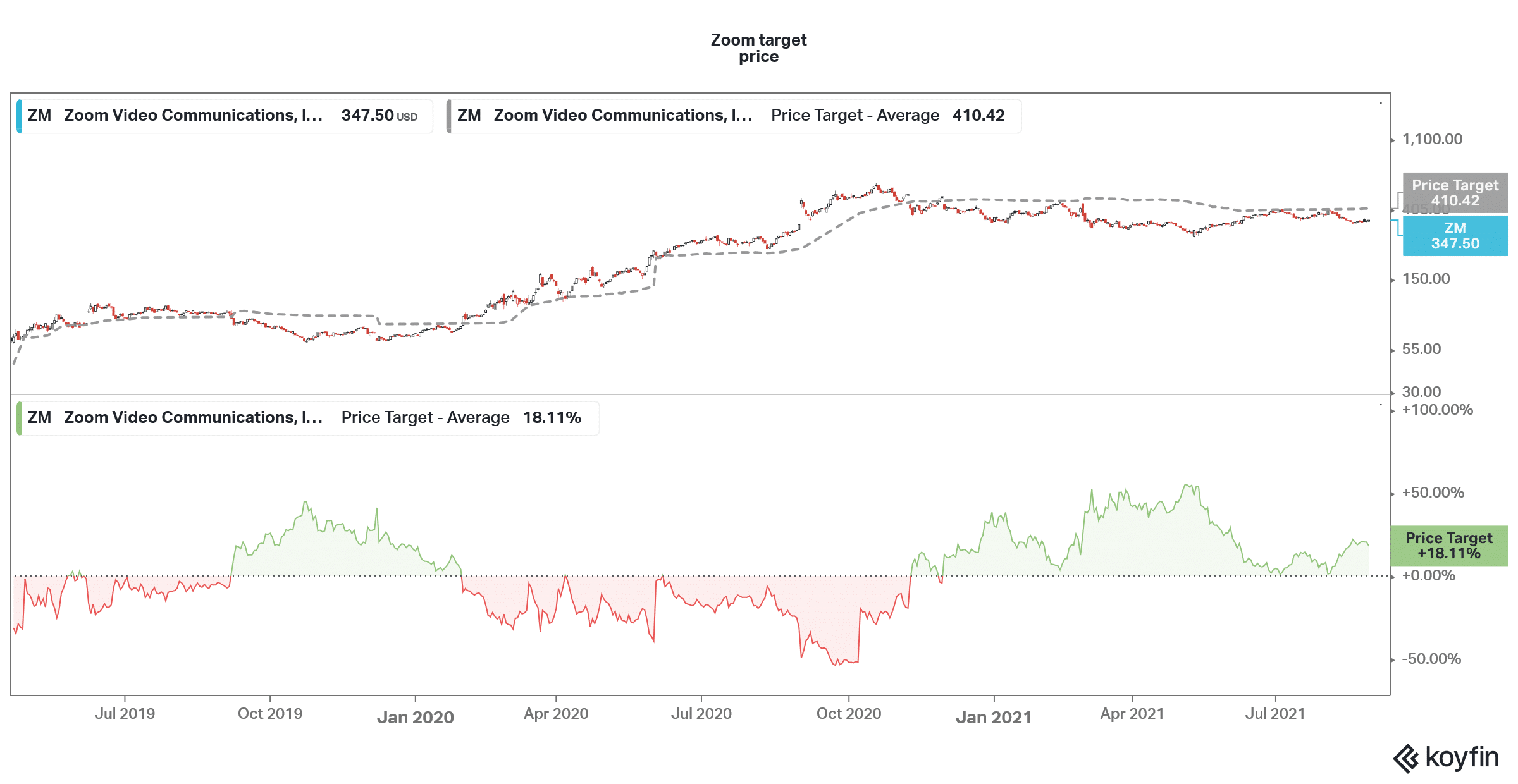

Looking at the consolidated ratings, analysts are split over the outlook for Zoom stock. It has a median target price of $416.50 which is an almost 20% premium over current prices. Its highest target price is $525 which is a premium of 51% while the lowest target price of $242 is a 30.4% discount over current prices. Of the 28 analysts covering the stock, 15 rate them as a buy while 11 rates them as a hold. The remaining two analysts rate them as a sell.

Zoom stock price long-term forecast

The growth rates for Zoom are coming down but the company is trying to grow inorganically. Last month, the company had said that it would acquire Five9 for $14.9 billion. The acquisition would help support the growth and would be financed through an all-stock transaction.

Meanwhile, Zoom is also facing competition from Microsoft Teams which has been trying to expand its market share.

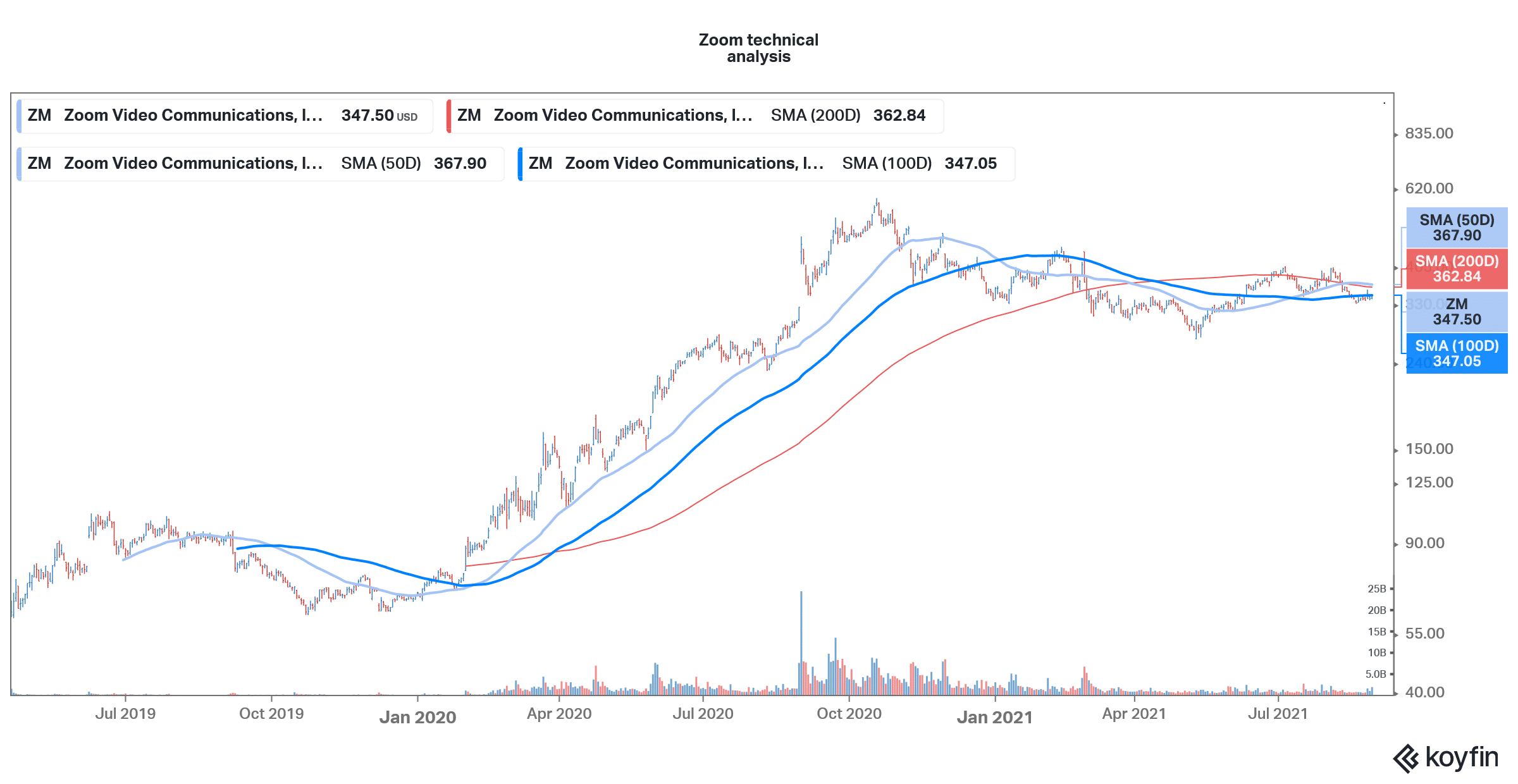

Valuation and technical analysis

Zoom was among the most expensive stocks in 2020. The valuation multiples have meanwhile come down sharply amid the crash in the stock. Also, its earnings have improved over the last year. The stock now trades at an NTM (next-12 months) PE multiple of 78x which is almost the lowest since it was listed.

Looking at the technical indicators, Zoom trades below the 50-day and 200-day SMA (simple moving average). The stock could also fall below the 100-day SMA in today’s price action looking at the premarket carnage. The MACD (moving average convergence divergence) is also a sell signal while the 14-day RSI (relative strength index) is a neutral indicator.

All said Zoom stock looks like a buy at these levels as the slowdown fears seem overblown. The sharp reaction to the company’s earnings looks unwarranted and is a good buying opportunity for long-term investors.

Buy ZM Stock at eToro from just $50 Now!