Zoom Video Stock Price Forecast July 2021 – Time to Buy ZM?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Zoom stock was trading lower in premarkets price action today. After the sharp rise last year, ZM is trading flat in 2021 as the so-called “stay-at-home” stocks have fallen out with investors amid the reopening.

What’s the forecast for Zoom stock in July 2021 and is the current weakness a time to buy this stock for the long term?

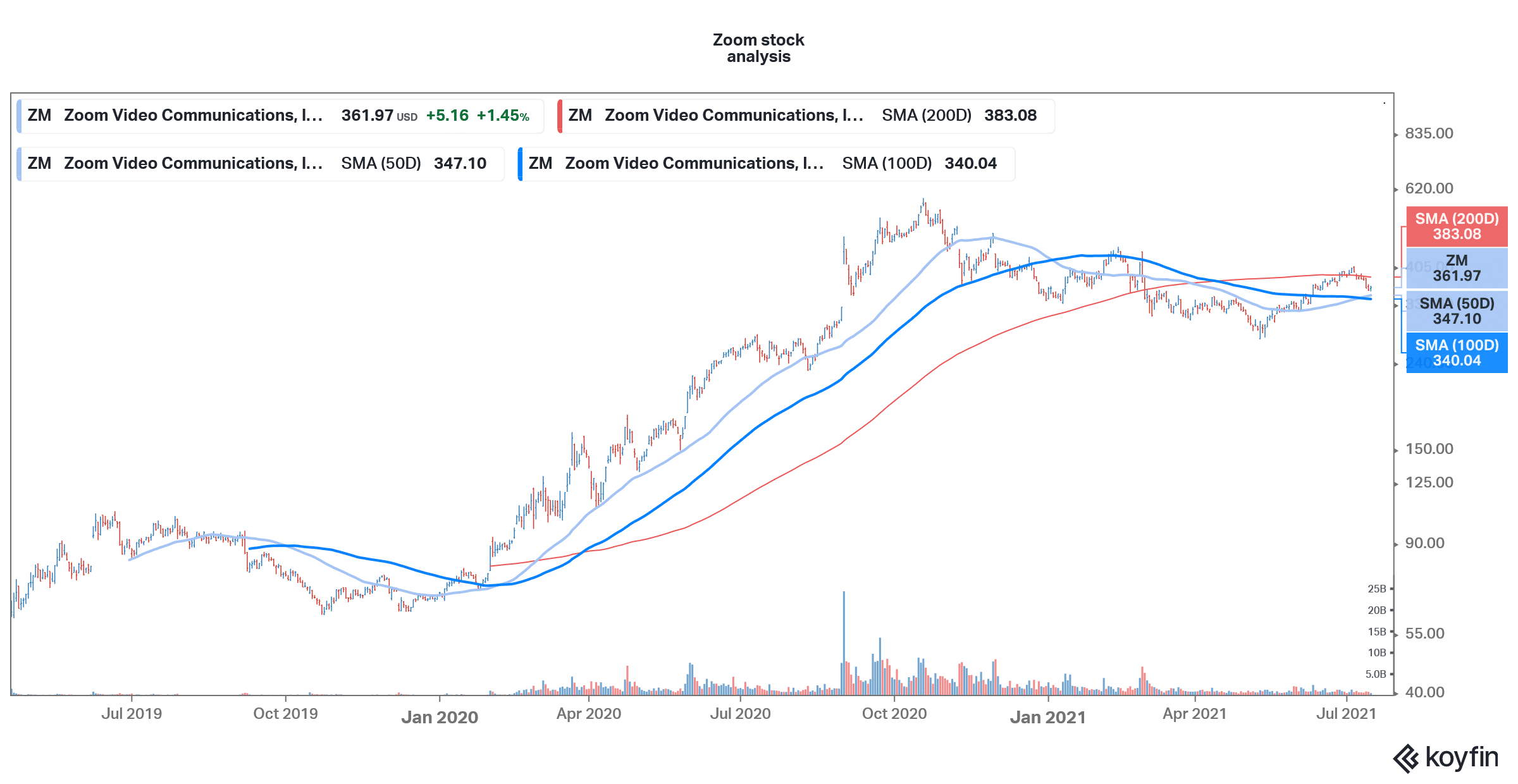

Zoom stock technical analysis

Zoom stock is not looking very bullish on the charts. Earlier this month, it fell below the 200-day SMA (simple moving average) and has since failed to cross above the trendline. The stock is finding support at the 50-day SMA which is currently at $347.50. The stock trades below the 10-day and 30-day SMA. The 12,26 MACD (moving average convergence divergence) also gives a sell indicator. The 14-day RSI (relative strength index) is 45.7 which is neutral and indicates neither overbought nor oversold positions.

67% of all retail investor accounts lose money when trading CFDs with this provider.

ZM stock latest news

Zoom has announced the acquisition of Five9 for $14.9 billion in an all-stock transaction. “We are continuously looking for ways to enhance our platform, and the addition of Five9 is a natural fit that will deliver even more happiness and value to our customers,” said Zoom’s CEO Eric S. Yuan, commenting on the transaction.

The company had raised $1.5 billion through a stock issuance earlier this year and had a cash pile of $4.7 billion at the end of the fiscal first quarter that ended on 30 April. It intended to use the funds for acquisitions.

Zoom enhances its target market

“The acquisition is expected to help enhance Zoom’s presence with enterprise customers and allow it to accelerate its long-term growth opportunity by adding the $24-billion contact center market,” said Zoom in its release. The transaction values Five9 at a premium of 13% premium. As part of the deal, existing Five9 stockholders will get 0.5533 Zoom Video Communications A shares for each share of Five9 shares that they hold.

Zoom has been battling a slowdown in growth rates and acquisitions will help it propel the growth. Several tech companies have gone for inorganic acquisitions over the last year to fuel their growth. These include Salesforce’s acquisition of Slack. Nvidia is also acquiring Arm Holdings in a mostly stock transaction from SoftBank. However, the deal is still to get regulatory approvals.

Zoom stock forecast

Meanwhile, Wall Street analysts have a split rating on Zoom stock and its median target price of $405 implies an upside of 11.9% over current prices. Its lowest target price is $242 which is a discount of over 33% while the highest target price of $525 is a premium of 45% over current prices.

Of the 128 analysts polled by CNN Business, 13 rate ZM stock as a buy while 13 rates it as a hold. Two analysts have a sell or equivalent rating on the stock.

Earlier this month, Benchmark initiated coverage on Zoom stock with a hold rating, and analyst Matthew Harrigan said that the current stock price “already implies heady growth.” Harrigan admitted that the company “may defy skeptics” by increasing its market share. However, he cautioned “immediate stock action hinges on momentum and sentiment, with consensus forecasts and even guidance providing a feeble valuation backbone.” Oppenheimer also reiterated its hold rating on the stock earlier this month.

Needham is apprehensive of the valuations

Needham analyst Ryan Koontz also rated the stock as a hold last month. “While the company issued an impressive F1Q22 report with 191% y/y revenue growth and better than expected GM, we look for continued traction with Phone, particularly in enterprise, evidence of stable churn in small business, further success in the channel and/or more clarity on the monetization timing for Zapps and Zoom Events before gaining more conviction on the stock at its current valuation,” said Koontz in his note.

Zoom stock long term forecast

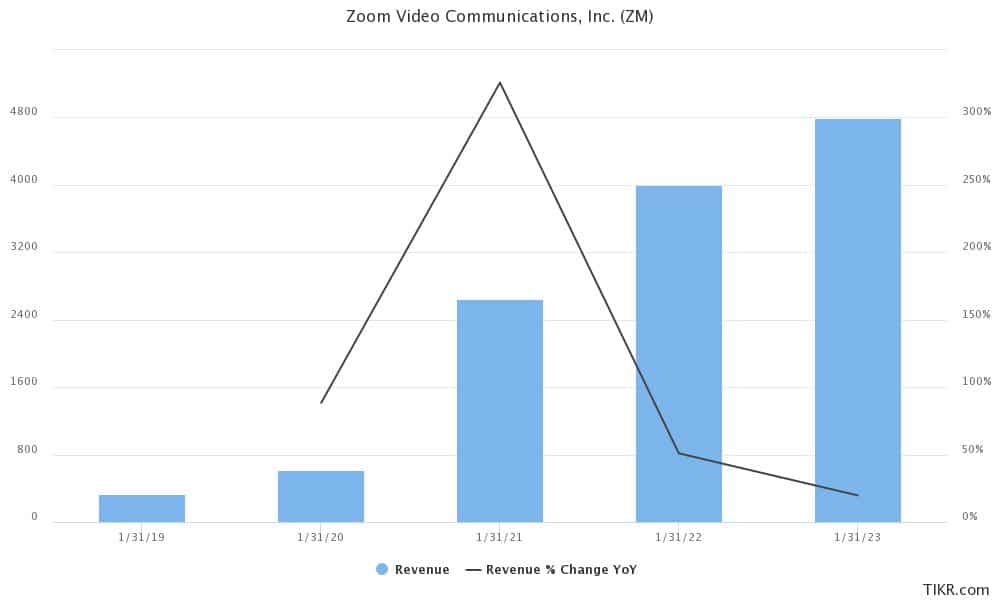

Zoom’s revenues skyrocketed 326% in the last fiscal year amid the lockdown-induced growth. However, analysts expect the growth rate to fall to 51% in this fiscal year and 20% in the next fiscal year. That said, ZM has been improving on the other metrics.

For instance, at the end of the fiscal first quarter of 2021, it had almost half a million customers with more than 10 employees which were 87% higher than the corresponding period last year. Also, 1,999 customers contributed over $100,000 in revenues in the trailing 12 months which was 160% higher than the corresponding period last year. The company has been adding bigger customers that add handsomely to its earnings.

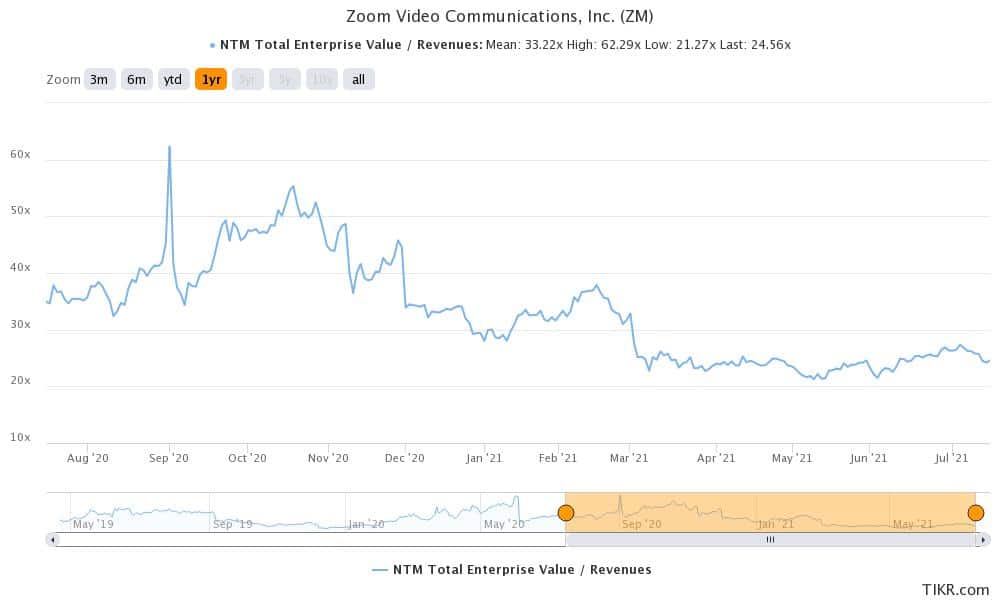

ZM stock valuations

The rally in ZM stock in 2020 was built on the erroneous premise that the growth rates of the year will be sustainable in the long term. However, that wasn’t the case and rising competition and the reopening are expected to take a toll on the growth rates.

Meanwhile, Zoom’s valuation multiples have also come down and it now trades at an NTM EV-to-sales multiple of 24.6x. The multiples have averaged 33.2x since the company went public. While ZM still remains one of the most expensive stocks based on the forward sales multiples, the recent fall could be an opportunity to buy the stock.

Zoom faces the threat of higher competition

There are several risks that the company faces including rising competition from rivals like Microsoft that have deep pockets. However, RBC analyst Rishi Jaluria who has a buy rating on Zoom stock is not too perturbed by the higher competition. In his note, he said “While we are not dismissive of competition, especially from giants like Microsoft and Google, we view Zoom’s video conferencing as being meaningfully differentiated on its reliability, scalability, and ease-of-use. We believe this and the critical nature of video conferencing will be enough to hold off ‘good enough’ competition, particularly from Microsoft Teams.”

67% of all retail investor accounts lose money when trading CFDs with this provider.