Zoom Stock Price Up Whopping 20% – Time to Buy Zoom Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Zoom (ZM) stock has gained 20% over the last month and has managed to recoup its 2021 losses. Is it time to buy Zoom stock now?

Zoom stock outperformed in 2020 amid the rally in the so-called “stay-at-home” stocks. ZM was possibly among the biggest beneficiaries of the changed consumer behavior as Zoom calls emerged as an alternative for physical meetings. The stock went as high as $588.84 last year as investors poured money into stay-at-home stocks.

Zoom stock came under pressure

However, the rally in stay-at-home stocks faltered amid positive progress on COVID-19 vaccine candidates. As the economies started to reopen and consumer behavior started to revert towards pre-pandemic levels, stocks like Zoom came under pressure. Despite having bounced back from the lows, ZM stock is down 36% from the peaks and is in a bear market territory having fallen over 20% from the highs.

67% of all retail investor accounts lose money when trading CFDs with this provider.

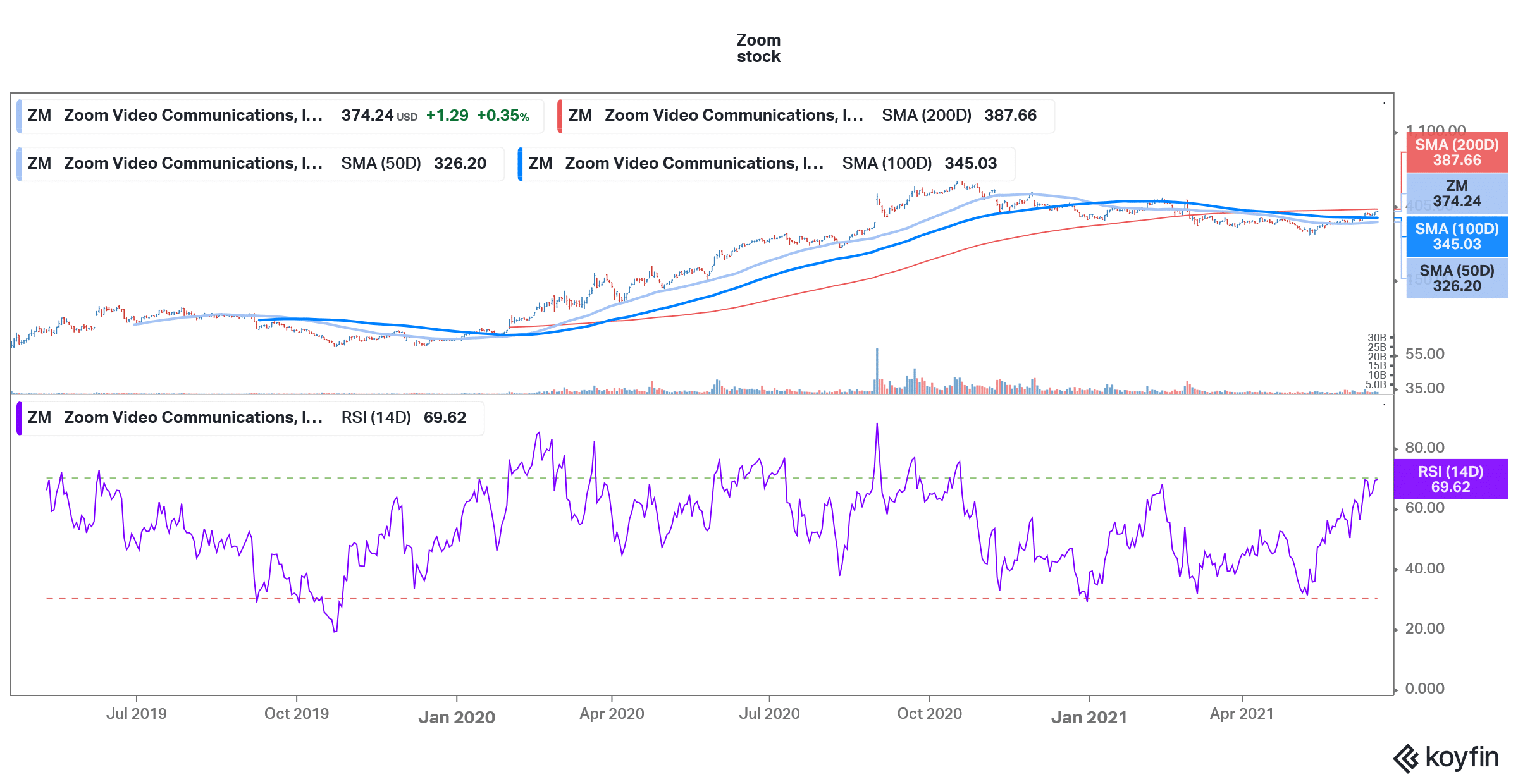

ZM stock technical analysis

Zoom stock is trading above its 50-day SMA (simple moving average) and 100-day SMA which is a bullish indicator. However, the stock has been facing strong resistance at its 200-day SMA which is currently at $387.66. The stock needs to break above the 200-day SMA convincingly for the uptrend to continue. ZM stock is looking overbought with a 14-day RSI (relative strength index) of 69.6. RSI values above 70 signal overbought positions.

Growth slowdown

Zoom’s growth got turbocharged in 2020 as the demand for its services spiked due to COVID-19 related restrictions. The company’s revenues in the fiscal year ended 31 January 2021 increased 326%. However, the growth rates are expected to taper down in this fiscal year. The company expects its revenues to rise about 50% this year and gave a guidance of $3.98-$3.99 billion in revenues. Also, it expects to post adjusted earnings per share of $4.56-$4.61 this year.

Typically, Zoom provides conservative guidance and ends up posting earnings that are higher than its guidance. Meanwhile, the company’s guidance for this fiscal year was way ahead of analysts’ estimates. ZM stock rose sharply after the earnings release as the growth slowdown was less intense than what the market was expecting.

“As we enter FY2022, we believe we are well positioned for strong growth with our innovative video communications platform, on which our customers can build, run, and grow their businesses; our globally recognized brand; and a team ever focused on delivering happiness to our customers,” said Zoom’s CEO Eric Yuan in the fiscal fourth quarter 2021 earnings release.

Zoom stock valuation

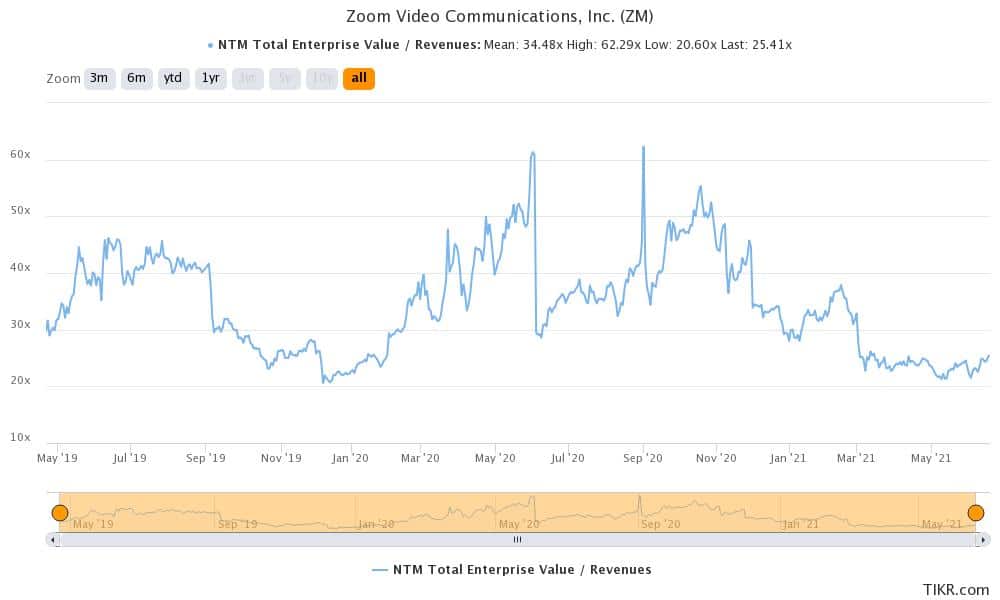

Meanwhile, amid the sharp increase in earnings and correction in the stock price, Zoom’s valuation multiples have also come down. The stock now trades at an NTM (next-12 months) EV (enterprise value)-to-revenue multiple of 25.4x. Since the company went public in 2019, the multiple has averaged 34.5x. It peaked at 62.3x but hit a low of 20.6x towards the end of 2019.

Zoom’s valuation multiples look much more reasonable now after the fall and the stock looks attractive. Also, the company has managed to improve its gross margins and could also look at acquisitions to fuel its growth. It raised $1.5 billion through a stock issuance earlier this year and had a cash pile of $4.7 billion at the end of the fiscal first quarter that ended on 30 April.

Zoom’s financial performance has been improving

Zoom has been improving its financial metrics. At the end of the fiscal first quarter 2021, it had almost half a million customers with more than 10 employees which were 87% higher than the corresponding period last year. Also, 1,999 customers contributed over $100,000 in revenues in the trailing 12 months which was 160% higher than the corresponding period last year. To sum it up, the company has been adding bigger customers that add handsomely to its earnings.

ZM stock forecast

Zoom stock has a median target price of $400 which is a 6.8% premium over current prices. Its highest target price is $525 which is a premium of 40% while the lowest target price of $242 is a 35% discount over current prices. Of the 25 analysts covering the stock, 12 rate them as a buy while 11 rates them as a hold. The remaining two analysts rate them as a sell.

Earlier this month, RBC initiated coverage on Zoom stock with a buy rating and assigned a target price of $450. “The future of work will likely be hybrid and we believe Zoom will be a critical component to enabling that future. We would argue that hybrid and distributed work is a tougher problem to solve than all employees working remote, as meetings will happen across devices (e.g. laptops, mobile phones, hardware meeting rooms,” said RBC analyst Rishi Jaluria.

Higher competition for Zoom

Meanwhile, several investors have been concerned about the increasing competition for Zoom, especially from Microsoft Teams and Google. Both these companies have deep pockets to take on Zoom.

However, Jaluria is not too perturbed by the higher competition. In his note, he said “While we are not dismissive of competition, especially from giants like Microsoft and Google, we view Zoom’s video conferencing as being meaningfully differentiated on its reliability, scalability, and ease-of-use. We believe this and the critical nature of video conferencing will be enough to hold off ‘good enough’ competition, particularly from Microsoft Teams.”

What’re the risks for ZM stock

While the growth rates for Zoom will arguably come down from the 2020 highs, the company should still continue to grow at a fast pace. That said, a faster than expected rise in US interest rates is a risk for growth names like ZM. The Federal Reserve’s dot plot showed two rate hikes by 2023. However, if the spike in inflation is not transitory as many currently believe, the US central bank might have to hasten its tightening. That could lead to a sell-off in growth names that have their earnings skewed towards the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.