Upstart Stock Down 22% in January – Time to Buy UPST Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Upstart stock has dived 22% in January as a spike in US Treasury yields and weakness in the tech sector as a whole have weighed the valuation of this fintech stock.

On 11 January, Upstart informed that it set a date for the release of its financial results covering the fourth quarter of the 2021 fiscal year. The report is expected to be published on 15 February after the market closes.

For the fourth quarter, Upstart’s management set forth the following guidance:

- Revenue of $255 to $265 million

- Contribution Margin of approximately 47%

- Net Income of $16 to $20 million

- Adjusted Net Income of $48 to $50 million

- Adjusted EBITDA of $51 to $53 million

- Basic Weighted-Average Share Count of approximately 81.9 million shares

- Diluted Weighted-Average Share Count of approximately 96.7 million shares

Meanwhile, the market’s consensus forecast for the firm’s adjusted quarterly earnings per share stands at $0.51.

Upstart has surprised the market by posting above-expected earnings and revenues in the past fourth quarters at least. This increases the odds that the company may beat analysts’ forecasts for the period.

That said, a sustained uptick in US Treasury yields has contributed to depress the valuation of high-flying tech stocks as market participants have adopted a risk-off attitude amid an expected shift in the Federal Reserve’s monetary policy.

The Chairman of the US central bank recently signaled that more aggressive measures may need to be adopted to curve the latest spike in prices. His comments came only hours after it was reported that inflation rose to 7% in the country in December – the highest annualized reading since 1982.

For banks and financial companies, higher inflation is not good news as it erodes their real earnings generation capacity.

What can be expected from Upstart stock ahead of the release of its Q4 2021 earnings report? In this article, I’ll be assessing the price action and fundamentals of UPST stock to outline plausible scenarios for the future.

68% of all retail investor accounts lose money when trading CFDs with this provider.

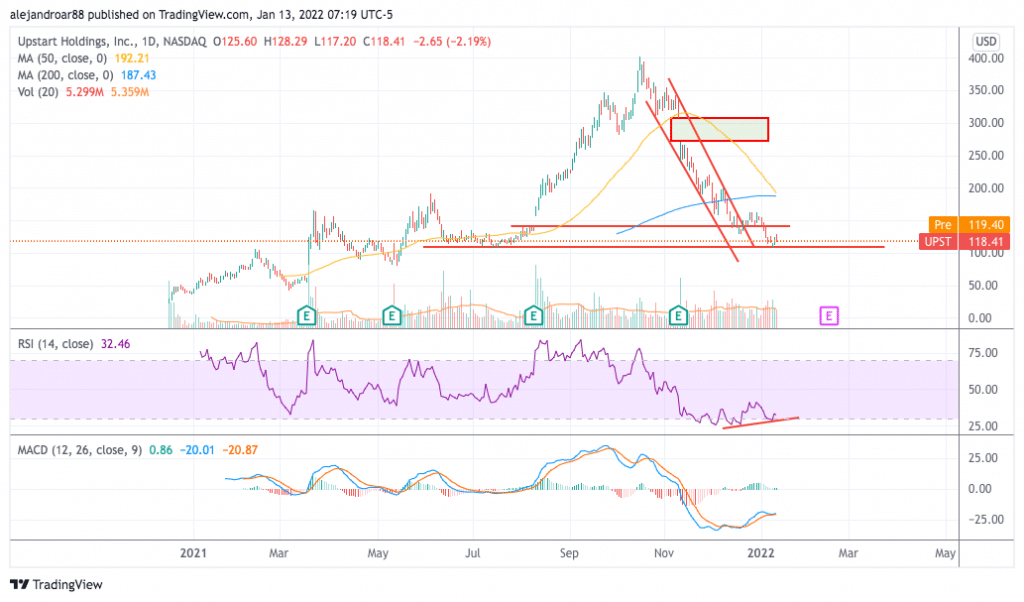

Upstart Stock – Technical Analysis

Back in December when I last wrote about Upstart, I outlined two possible scenarios for the stock based on its technical setup. The first was that the stock could decline to the $110 level if it broke below the $145 support area shown in the chart above and the second was that the stock may trade range-bound following a rebound off this same area.

The first scenario unfolded as expected with the price declining and bouncing off the $110 level for a 24% loss (or gain for short sellers) since the article came out.

This bounce is particularly interesting as it occurred on the day that the company set the date for the release of its Q4 2021 financial results.

Trading volumes exceeded the 10-day average on that day as well and momentum indicators are starting to show signs of a deceleration in the latest downtrend. In this regard, the Relative Strength Index (RSI) is displaying a mild bullish divergence and the same goes for the MACD.

However, a death cross just popped up between the 50-day and 200-day simple moving averages and that favors a bearish mid-term outlook for Upstart stock.

Moving forward, the price could move higher ahead of the release of this financial report. However, the short-term upside potential seems limited as momentum remains quite negative and the stock will soon encounter three different areas of resistance.

With this in mind, it would be plausible to see Upstart rising to the high 100s but rejecting a move above the $200 level in the short term. As a result, the mid-term outlook remains bearish and the stock could trade in a range between $110 and $190 for a while.

Upstart Stock – Fundamental Analysis

The market capitalization of Upstart has declined from a peak of around $35 billion back in October to less than $10 billion as of yesterday.

This has led to a contraction in the once high-flying trading multiples assigned to this fintech company and this calls for a revision of its merits as an investable growth stock considering the firm’s industry-disruptive business model.

For the 2022 fiscal year, analysts are expecting to see revenues for Upstart surging to $1.2 billion while the firm’s adjusted earnings per share are expected to land in a range between $1.7 and $3.6.

One positive factor about this company is that it is already cash-flow positive. In the past 12 months, Upstart generated $240 million in free cash flows resulting in an FCF margin of around 40%.

This was the result of a significant jump in business volumes as Upstart revenues more than tripled during that period. Moving forward, based on analysts’ revenue estimates for the firm for 2022, Upstart could generate around $480 million in free cash flows during this period.

Based on the firm’s current market cap of $10 billion, that results in a forward P/FCF ratio of 20.8x. Meanwhile, the company is also trading at around 9 times its forecasted sales for the year.

This strong cash-flow generation capacity makes the firm’s long-term debt manageable at $650 million on total assets of $1.3 billion including $1 billion in cash.

From a fundamental perspective, the long-term outlook for Upstart stock is bullish. However, negative volatility may continue as long as the situation with the Federal Reserve and its upcoming policy changes remains relatively uncertain.

Buy UPST Stock at eToro with 0% Commission Now!