Roku Stock Down 25% Today – Time to Buy ROKU Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Roku stock is declining nearly 25% this morning in pre-market stock trading action following the release of the firm’s financial results covering the fourth quarter of 2021 as revenues missed analysts’ estimates for the period.

For the three months ended on 31 December, Roku reported total revenues of $865.3 million resulting in a 33% jump compared to the same period a year ago with platform revenues surging 49% while player sales retreated 9%.

The number of active accounts grew 17% on a year-on-year basis at 60.1 million while the number of streamed hours increased 15% compared to the previous year as well. Average revenues per user ended at $41.03 resulting in a 43% year-on-year advance.

Gross margins retreated 310 basis points compared to Q4 2020 and as much as 960 basis points on a sequential basis as negative margins in the player segment have increased as a result of rising manufacturing costs amid the ongoing global supply chain crisis.

In this regard, Roku’s management stated: “Overall TV unit sales are likely to remain below pre-COVID levels, which could affect our active account growth. Account acquisition will remain a priority, and we intend to continue to insulate customers from elevated costs in our player business, which will continue to cause negative player gross margins until conditions normalize”.

Income from operations fell 67% on a year-on-year basis while net income stood at $23.68 million. This resulted in GAAP diluted earnings per share of $0.17. Analysts were expecting GAAP EPS of $0.04 per share for the period. On an adjusted basis, Roku produced adjusted EBITDA of $86.7 million resulting in a 23.6% drop compared to a year ago while EBITDA margins declined 740 basis points to 10%.

For the upcoming quarter, Roku estimated that revenues will land at $720 million while the firm is expected to produce net losses of $30 million and adjusted EBITDA of $55 million resulting in a 7.6% margin. This revenue forecast came below the market’s estimate of $756 million for the period.

The combination of lower margins, disappointing revenue growth, and below-expected guidance is probably the reason why Roku stock is down today.

What could be expected from this tech stock in light of today’s report? In this article, I’ll be assessing the price action and fundamentals of ROKU stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Roku Stock – Technical Analysis

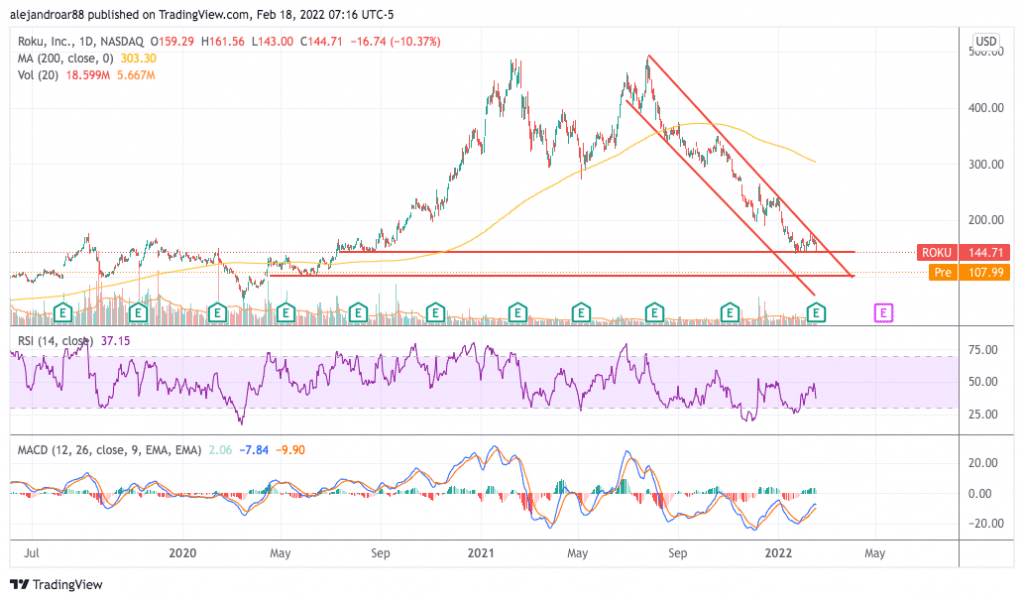

So far in 2022, the price of Roku has declined nearly 37% while the stock is trading 70.5% below its 52-week high of $490.76 per share.

Changes in the macro environment along with weakness in the business’s performance amid a fading pandemic tailwind and the ongoing supply chain crisis are weighing the most on the performance of this growth stock.

Just yesterday, the price went down more than 10% ahead of the release of this earnings report. This decline pushed ROKU to retest an important area of support at $145 per share while today’s drop is pushing the price below this relevant marker.

If this morning’s pre-market downtick spills over to the live session as is, the price would collapse to its lowest level since June 2020.

Momentum indicators at the moment remain bearish as the Relative Strength Index (RSI) has failed to climb above the 50 level multiple times while the MACD is neck-deep into negative territory despite climbing above the signal line in the past few days.

All things considered, the outlook for Roku stock remains bearish and the downside risk based on yesterday’s closing price stands at around 30%.

Roku Stock – Fundamental Analysis

This latest earnings report is not necessarily that bad in terms of revenue and user base growth as the performance of Roku relative to pandemic-era figures is still positive.

In this regard, active accounts have kept climbing at a decent pace while average revenues per user are advancing as well.

However, the deterioration in the firm’s bottom-line profitability amid the negative performance of the Player segment is worth a second look and the markets appear to be spooked by the fact that the management is not yet foretelling when this situation might come to an end.

The combination of these business-specific and macro headwinds may continue to weigh on the valuation of Roku stock for a while and investors should consider the possibility that it might take years for ROKU to recover the losses it experienced in the past few months.

Based on the market’s revenue forecast for 2022, Roku’s forward P/S ratio stands at 4x. Meanwhile, last year, the company produced positive free cash flows of $188 million resulting in an FCF margin of 7%.

Using an estimated FCF margin of 7% to 10%, Roku might produce up to $500 million in free cash flows next year resulting in a forward P/FCF multiple of 39x.

These multiples are relatively conservative for a business that is growing as fast as Roku but that does not necessarily mean that the stock is cheap at the moment as profits may continue to deteriorate if the supply chain crisis takes longer to be solved than the market initially expected.

All things considered, Roku’s valuation at the moment is relatively appealing, especially as the company’s balance sheet is quite robust. However, it might take a lot of time for the stock to recover its lost territory as the current environment remains highly unfavorable for early-stage companies.

Buy ROKU Stock at eToro with 0% Commission Now!