Rivian Stock Down 21% in January – Time to Buy RIVN Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Rivian stock is down 21% so far this month after multiple news seem to have unleashed another wave of negative momentum for the electric vehicle startup.

On 5 January, a deal between Amazon (AMZN) and Stellantis was announced during the 2022 Consumer Electronics Show (CES) where the world’s largest e-commerce platform pledged to buy a large number of the automobile manufacturer’s Ram ProMaster electric-powered delivery vans.

Shares of Rivian went down as much as 11% as the market interpreted this as an interesting turn of events in the relationship between Amazon and the EV startup considering that the e-commerce giant holds a large stake and remains the largest single buyer of Rivian’s commercial to-be-manufactured vehicles.

Meanwhile, Rivian stock is down 4% this morning in pre-market stock trading action following news that the company’s Chief Operating Officer (COO) is stepping down.

According to a statement from the company, Rod Copes’s departure was part of a “phased retirement” that was planned months ago. The spokesperson also said that production should not be disrupted by this leadership change.

Mr. Copes joined the company in March 2020 as the electric vehicle startup accelerated its efforts to ramp up production.

Meanwhile, Rivian shared that it produced a total of 1,015 vehicles in 2021 and delivered 920 of those units. This figure was lower than the company’s initial projections of 1,200 units for the year.

What could be expected from this electric vehicle stock in light of these recent developments? In this article, I’ll be analyzing the price action and fundamentals of Rivian stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Rivian Stock – Technical Analysis

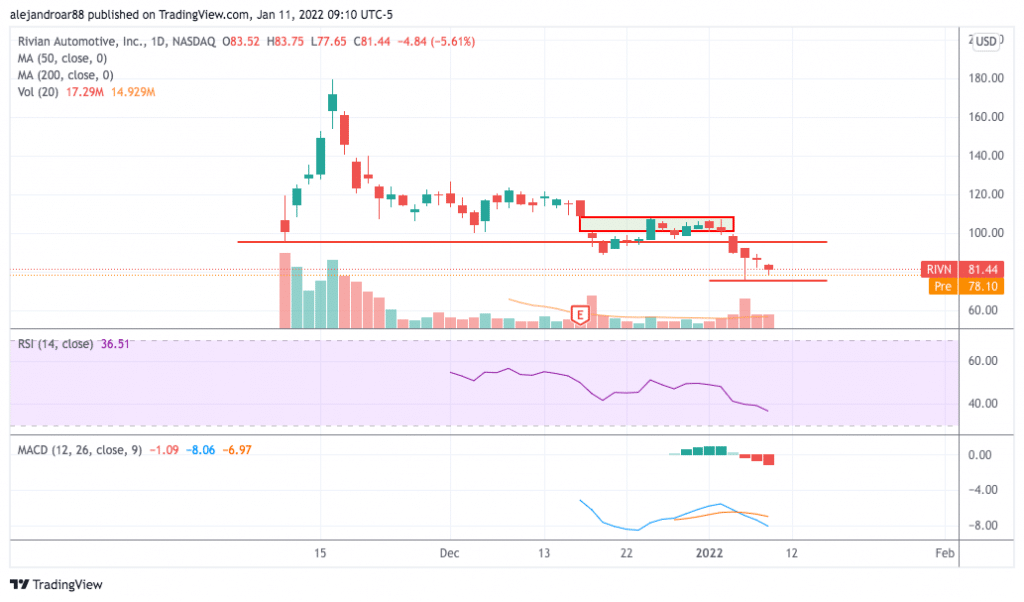

Based on yesterday’s closing price, Rivian is trading almost 55% below its post-IPO high of $179.5 per share while the stock is dangerously approaching its all-time lows from two days ago as well.

The decline that the two news highlighted above are prompting is worrying, especially if they lead to a break below the $75 intraday low of 6 January.

Back then, buyers showed up to scoop a large number of Rivian (RIVN) shares or maybe short sellers took some gains after the pronounced drop that followed the stock’s controversial post-IPO surge.

Since Rivian only became a public company two months ago, its trading history is quite limited and there are still no relevant moving averages to watch that can give us a better understanding of its outlook from a technical perspective.

That said, momentum readings are quite negative at the moment with the Relative Strength Index (RSI) declining to its lowest level since the indicator started to show up while the MACD has drifted below the signal line as well. This move is being accompanied by steadily increasing negative histogram readings.

Interestingly, market participants closed the bearish gap left behind after the company published its first quarterly report and the stock collapsed shortly after the gap was closed. This can be interpreted as further confirmation that the stock will be heading downwards moving forward as that technical threshold will no longer support a rebound.

Using a trend-based Fibonacci projection, the price of Rivian stock could decline to the low 50s if the $75 area is broken resulting in a total downside risk of 37%.

Rivian Stock – Fundamental Analysis

The 920 units that Rivian reportedly delivered in 2021 should have produced revenues of around $63.5 million for the startup based on a Manufacturer’s Suggested Retail Price (MSRP) of $69,000 per vehicle.

The company’s goal for the full 2022 fiscal year is to produce and deliver at least 40,000 units, meaning that the firm could generate around $2.8 billion in revenue. However, that is an ambitious target and the departure of the company’s COO at such a critical time for the startup is not good news.

The company currently operates one manufacturing facility located in Normal, Illinois (the ‘Normal Factory’) and one of its risk factors concerning this aspect of the business is that the firm has “no experience as an organization in high-volume manufacturing of EVs”.

The Normal Factory is reportedly capable of producing 150,000 vehicles per year but the company has not yet assured that the facility is ready to handle that kind of volume.

Overall, Rivian could scale up its production to 40,000 units in 2022 but investors would still be taking a big risk at the current valuation since, even if that goal is met, the company would still be valued at 26 times its forecasted sales for this year despite the significant challenges that lie ahead in its path to become a profitable endeavor.

By the end of September 2021, Rivian had no long-term debt and reported total assets of $8.5 billion including $5.2 billion in cash and equivalents. Meanwhile, the company produced net losses of $2.22 billion and burned nearly $2.9 billion in cash during the first nine months of 2020.

If the company’s annual cash burn is somewhere around $4 billion, Rivian may need to raise more capital later this year as it still has to invest a lot of money to keep strengthening its manufacturing capabilities to meet its production goals.

With that in mind, the current valuation seems unreasonable from a fundamental perspective and this, along with the market’s overall risk-off attitude prompted by a shift in macro factors, favors a mid-term bearish outlook for RIVN stock.

Buy RIVN Stock at eToro with 0% Commission Now!