Peloton Stock Price Falls 6% – Time to Buy PTON Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Peloton (PTON) stock fell 6.3% yesterday which took its YTD loss to 35.2%. The stock is now down almost 45% from the 52-week highs and is not far from the 52-week lows of $80.48.

2020 was a good year for so-called “stay-at-home” stocks like Peloton and it surged during the year. 2021 has been a different ballgame though and the stock has looked weak for the most part of the year. What’s the forecast for PTON stock and should you buy the dip?

Why has Peloton stock been falling

Blame the fall in Peloton stock on both macro as well as company-specific factors. There has been a sell-off in all stay-at-home stocks as the economy has mostly reopened. This has led to a fall in sales growth for most of the stay-at-home stocks. Names like Zoom Video Communications and Amazon which benefited from the lockdowns last year have looked weak this year.

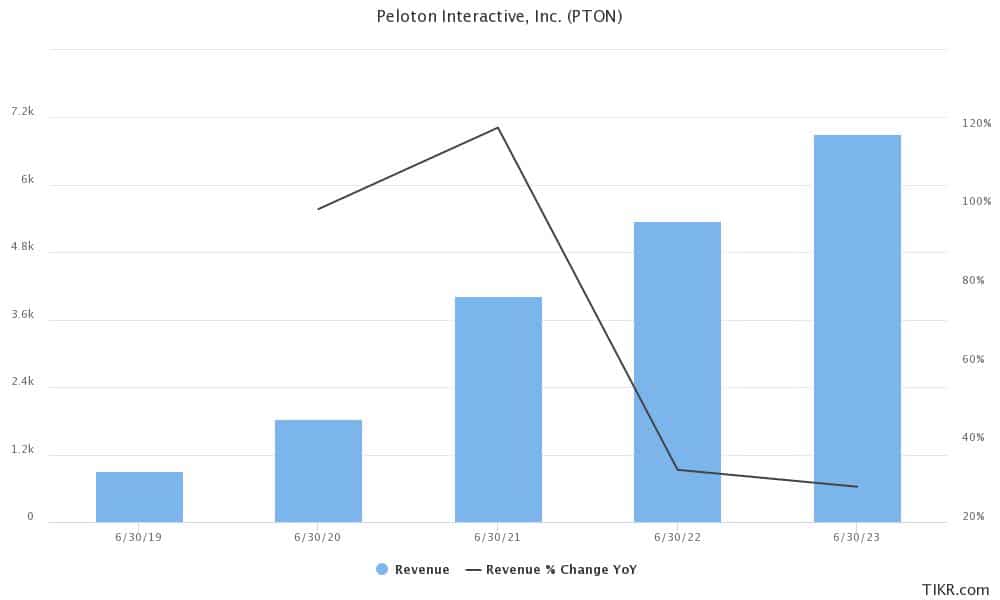

Peloton’s product recalls haven’t helped the stock either. After two recalls, the company has admitted to touchscreen problems in bike and tread. In its most recent quarter, it reported revenue growth of 54%. However, in the current quarter, it expects the topline to fall to $800 million from $937 million in the previous quarter.

67% of all retail investor accounts lose money when trading CFDs with this provider

PTON earnings

Also, in the fiscal fourth quarter, its average monthly workout per connected customer fell to 19.9 from 24.7 in the corresponding period last year. Like many other growth companies, PTON is also making losses and in the fiscal fourth quarter, it reported an adjusted EBITDA loss of $45.1 million with a margin of -4.8%. For the fiscal year 2022, the company has given a revenue guidance of $5.4 billion but expects to post an adjusted EBITDA loss of $325 million which would mean a margin of -6%.

The COVID-19 pandemic helped buoy demand for home fitness companies like Peloton. In its earnings release, it said “The past year represented an inflection point for the connected fitness industry, with significant increases in awareness and demand following the onset of the COVID-19 pandemic.”

Peloton stock recent developments

From the home fitness market, Peloton is now also diversifying into the commercial market. Earlier this year, it had acquired Precor and is now integrating the two businesses to target the hospitality sector. Brad Olson, Peloton’s chief business officer said that “We’ve been selling Peloton bikes into hotels and resorts for years. … But this is really the culmination and one of the big elements of the deal rationale of why we purchased Precor.”

He added, “We know that [having] our bikes in hotels and resorts around the world presents a great opportunity for lead-generation awareness of the Peloton product and content.”

PTON stock forecast

Despite the recent slump and the recalls, most Wall Street analysts have a bullish view of Peloton stock. Of the 31 analysts polled by CNN Business, 23 rate it as a buy while six rate it as a hold. Two analysts have a sell or equivalent rating on PTON stock.

Peloton has received a median target price of $135 which represents a potential upside of 42.8% over current prices. Its street high target price is $185 which is a premium of 95.6% over current prices.

Peloton stock target price

Of late, analysts have had a mixed opinion about PTON stock. Earlier this week, UBS reiterated Peloton stock as a sell. “We do not see the launch of private-label apparel a tangible driver of subscriber growth — a key factor driving forward multiples and EV to sales valuation framework for PTON — but a sizable and well-executed private label business could drive further brand awareness and promote a sense of community and increase level of sub engagement,” it said in its note.

Last month, Citi initiated coverage on the stock with a neutral rating. While it sounded bullish on the business model and the long-term growth potential for home gyms, it expressed concern over the near-term growth amid the reopening of the gyms.

PTON stock long term forecast

The long-term outlook for home fitness equipment companies like Peloton looks positive. While the growth rates of 2020 might not be sustainable, the industry should see secular growth over the long term. PTON is also building a factory in the US to support the demand. The company has been facing supply chain issues and a plant in the US would help address the concerns.

Meanwhile, the competition is also heating up and competitors like Beachbody are offering home gym products at a lower price. Peloton’s image as a premium brand has taken a hit amid the recalls. The company would have to regain credibility over the medium term. Wall Street analysts expect the company’s revenues to rise 33.3% in the fiscal year 2022 and 29% in the fiscal year 2023.

Peloton stock valuation and technical analysis

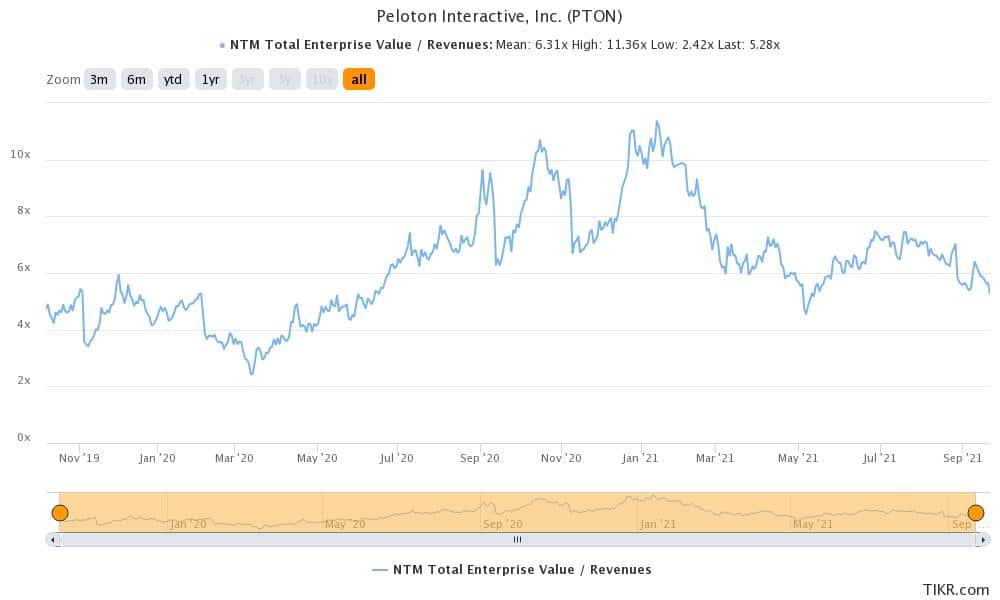

PTON stock currently trades at an NTM (next-12 months) EV (enterprise value to revenue) multiple of 5.3x. The multiples have averaged 6.3x since the company was listed. They bottomed at 2.4x during the March 2020 stock market sell-off and peaked at 11.4x earlier this year.

While the valuation multiples have come down, the company’s growth outlook also looks weaker than what it did some six months back. The recalls have also taken a toll on the multiples. That said, after the recent crash, PTON stock looks like a good buy.

Looking at the charts, PTON stock is looking bearish though. It trades below the 50-day, 100-day, and 200-day SMA (simple moving average). The 200-day SMA has been a key resistance for the stock and it has failed to cross above the price channel. The MACD (moving average convergence divergence) also gives a sell signal. However, the 14-day RSI (relative strength index) of 35.3 is a neutral indicator.

Should I buy PTON stock?

If you are bullish on the home fitness market, PTON is among the best stocks to play the story. It looks like a good stock to buy after the recent weakness and should deliver good returns over the medium to long term.

Buy PTON Stock at eToro from just $50 Now!