Merck Stock Down 10% in November – Time to Buy MRK Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Merck stock is down 10% so far in November following news about the higher efficacy of Pfizer’s COVID pill and recent findings that pointed to the lower efficacy of the firm’s molnupiravir treatment.

Shares of the American pharmaceutical company have shed nearly all of their October gains after the first results of this promising drug were released as they showcased efficacy levels of 48% for preventing hospitalization and death among COVID patients.

However, Pfizer’s COVID pill (Paxlovid) displayed nearly twice that efficacy at 89% while recent findings published by Merck and Ridgeback Biotherapeutics led to a downward revision of its initial numbers as molnupiravir was able to reduce hospitalizations and deaths by only 30% during a trial that involved a larger number of patients.

Is the market mispricing MRK stock amid the pessimism instilled by these latest developments or is this decline justified? In this article, I will be assessing the price action and fundamentals of this healthcare stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

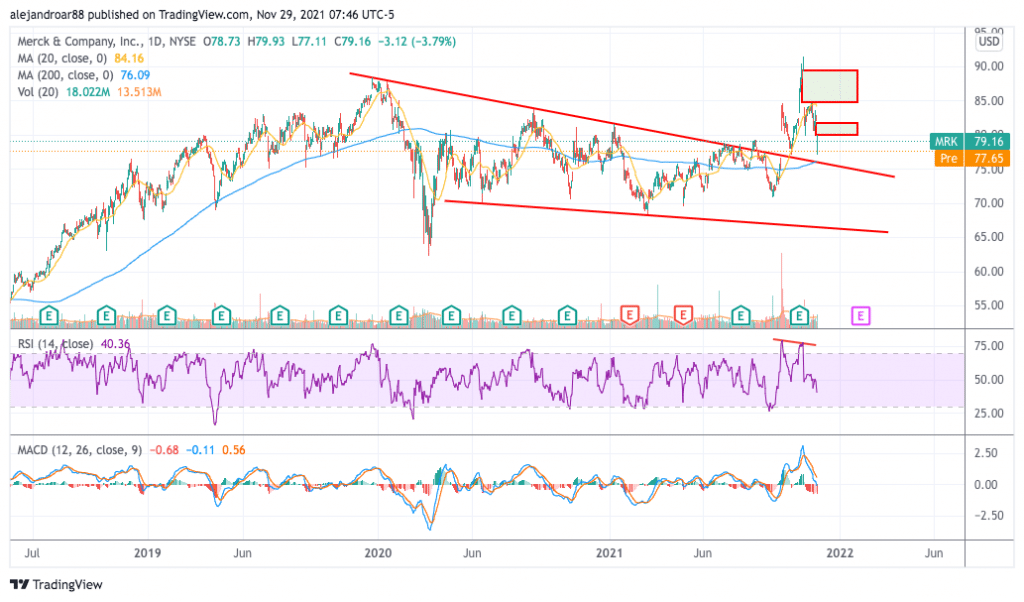

Merck Stock – Technical Analysis

Merck stock is down 2% in pre-market stock trading action today following news that the Omicron variant of the virus may not be as worrying as initially thought. Last Friday, the stock declined nearly 4% but posted losses of up to 6% in intraday action after news about the lower efficacy of molnupiravir came out.

This decline has resulted in a break below Merck’s short-term moving averages while the price is now approaching the 200-day simple moving average. The chart above shows that there is a confluence between this marker and the upper bound of the descending price channel that dominated the price action since 2020 started.

In a previous article about Merck stock, I highlighted that the Relative Strength Index (RSI) was displaying a bearish divergence that increased the odds of a sharp downturn and this risk materialized on the back of the latest negative developments concerning Merck’s COVID drug.

As a result, the outlook for MRK stock is now bearish as momentum has turned negative. In this regard, the Relative Strength Index (RSI) is standing at 40 (bearish) while the MACD has crossed below the signal line while it is moving to negative territory at the same time that negative histogram readings are steadily increasing.

Moving forward, the 200-day simple moving average remains the most relevant support to watch – currently standing at $76 per share. If that threshold is broken, the stock could dive to the low 70s for a total downside risk of approximately 10% based on last Friday’s closing price.

Merck Stock – Fundamental Analysis

Based on my initial estimates, molnupiravir would have brought around $8 billion in revenues to Merck resulting in a 14% jump in the firm’s top-line results. However, those prospects are no longer on the table and, in the current scenario, it seems unlikely that the firm will continue to invest money into developing this treatment amid the low efficacy it has displayed in preventing deaths and hospitalizations.

The reason for this is that a highly effective rival already exists and may get emergency-use approval from the US Food and Drug Administration (FDA) very soon. For Merck, commercializing molnupiravir could be too costly and the price of treatment would have to be lower than that of its top competitor to attract consumers – in this case, Pfizer (PFE).

Overall, it seems highly likely that the stock will be plugged into the descending price channel shown in the chart above again as the market’s overall pessimism about Merck’s outlook should once again dominate the price action.

If the stock does drop to the low 70s, its forward P/E ratio may stand at around 10x and the dividend yield could increase to 3.5%. At that level, Merck would stand out as a top dividend stock as the company displays a robust dividend coverage based on the free cash flows it has produced in the past couple of years.

Other than that, even though its trading multiple makes it seem like a bargain, the company’s future earnings growth does not allow it to qualify as a potential value stock.

Buy MRK Stock at eToro with 0% Commission Now!