Krispy Kreme Stock Price Forecast December 2021 – Time to Buy DNUT Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

2021 hasn’t been a good year for IPOs in terms of price action. Krispy Kreme (NYSE: DNUT) stock, which went public in 2021, has largely traded below its IPO price of $17.

However, the stock rose over 10% yesterday and is now back above the IPO price. What’s the forecast for DNUT stock and is it a good buy for 2022?

Notably, it was the second listing for DNUT. It was a publicly-traded company until 2016 before JAB Holdings took it private. The company didn’t have a good ride as a publicly-traded company and saw sagging topline growth. Investors have been worried about the growth outlook for the company now also.

Krispy Kreme recent developments

Earlier this month, Krispy Kreme raised its fiscal year 2021 guidance and said that it expects sales to be between $1.37-$1.385 billion in the year. The guidance was slightly ahead of the $1.34-$1.38 billion that it had previously provided. It also raised the profit guidance and said that the adjusted EBITDA in the year should be between $182-$187 million, which was better than the previous guidance of $178-$185 million.

Commenting on the guidance, Mike Tattersfield, Krispy Kreme’s CEO said “Our global omni-channel business has continued to perform well as we benefit from the sharing and gifting occasions of the holiday season.” He added, “Our U.S. and international businesses have both contributed significantly to our growth this quarter. We have been able to successfully pass-through price increases in the U.S. in September and November addressing inflation.”

Notably, several brokerages have taken a pessimistic view of DNUT stock citing the cost pressures. The guidance raise helped allay some of the fears of margin compression.

68% of all retail investor accounts lose money when trading CFDs with this provider.

DNUT announced a discount offer

Earlier this week, DNUT announced a “Raise a Glazed” offer wherein the company would offer Original Glazed dozens for just $12. The offer would be valid between 30 December to 2 January. The stock jumped after the announcement which might sound surprising.

Krispy Kreme posted better than expected earnings

In November, Krispy Kreme had released its fiscal third-quarter earnings and reported revenues of $342.8 million in the quarter which were ahead of the $337.7 million that analysts were expecting. The company’s organic revenues, which excludes the now exited Wholesale business, increased 14% as compared to 2020 and 22% compared to 2019.

Its net loss of $5.7 million in the quarter was also narrower than the $14.9 million that it had posted in the corresponding period last year. The company has displayed good pricing power and has been able to pass on the increased costs to buyers.

Along with higher input costs and supply chain issues, Krispy Kreme is also battling with the labor shortage situation. Just when the labor supply situation in the US was stabilizing, the omicron virus has complicated the picture. One casualty has been the cancelation of thousands of flights in the country over the last week.

Krispy Kreme forecast

Of the nine analysts covering Krispy Kreme stock, five have a buy rating while three rate them as a hold. One analyst has a sell rating on the stock. It has a median target price of $19 which is a 6.4% premium over current prices. The street low target price of $14 is a discount of 21.6% while the street high target price of $24 is a premium of 34.5%.

Over the last month, several brokerages have downgraded DNUT stock. Earlier this month, Goldman Sachs downgraded the stock from a neutral to sell and slashed its target price to a street low of $14.

Goldman Sachs is bearish in DNUT stock

“We view rising cost pressures across many key inputs for DNUT’s increasingly company-owned model as a key risk for margins, while our consumer survey data suggests the brand may have limited pricing power to offset inflationary headwinds,” it said in its note.

Goldman Sachs added, “The primary inputs for DNUT are edible cooking oils, sugar, and wheat, and each of these items is currently highly inflationary, with some items continuing to accelerate. Prices for edible/cooking oils are up significantly — +86% yoy and +106% vs 2019 — as a combination of higher demand from restaurants and the broader economy along with crop/production challenges for cooking oils.”

Rising costs are a concern

Last month, Truist had downgraded Krispy Kreme stock expressing concern over inflationary pressures. In October, HSBC had also downgraded the stock from a buy to hold expressing concern over rising inflation. It also questioned the company’s strategy of moving from a franchise model to a company-owned model. Globally, QSR chains are moving to a franchise model which helps in better returns on capital.

Krispy Kreme stock long forecast

Over the long term, DNUT is a play on deleveraging and the continued growth in business. While inflation is a short-term concern, the company has the good pricing power to pass on the increased prices to end consumers.

The company recently affirmed its long-term guidance. The company expects long-term revenue growth of 9-11% while forecasting its net income to rise between 18-22%.

Should you buy DNUT stock?

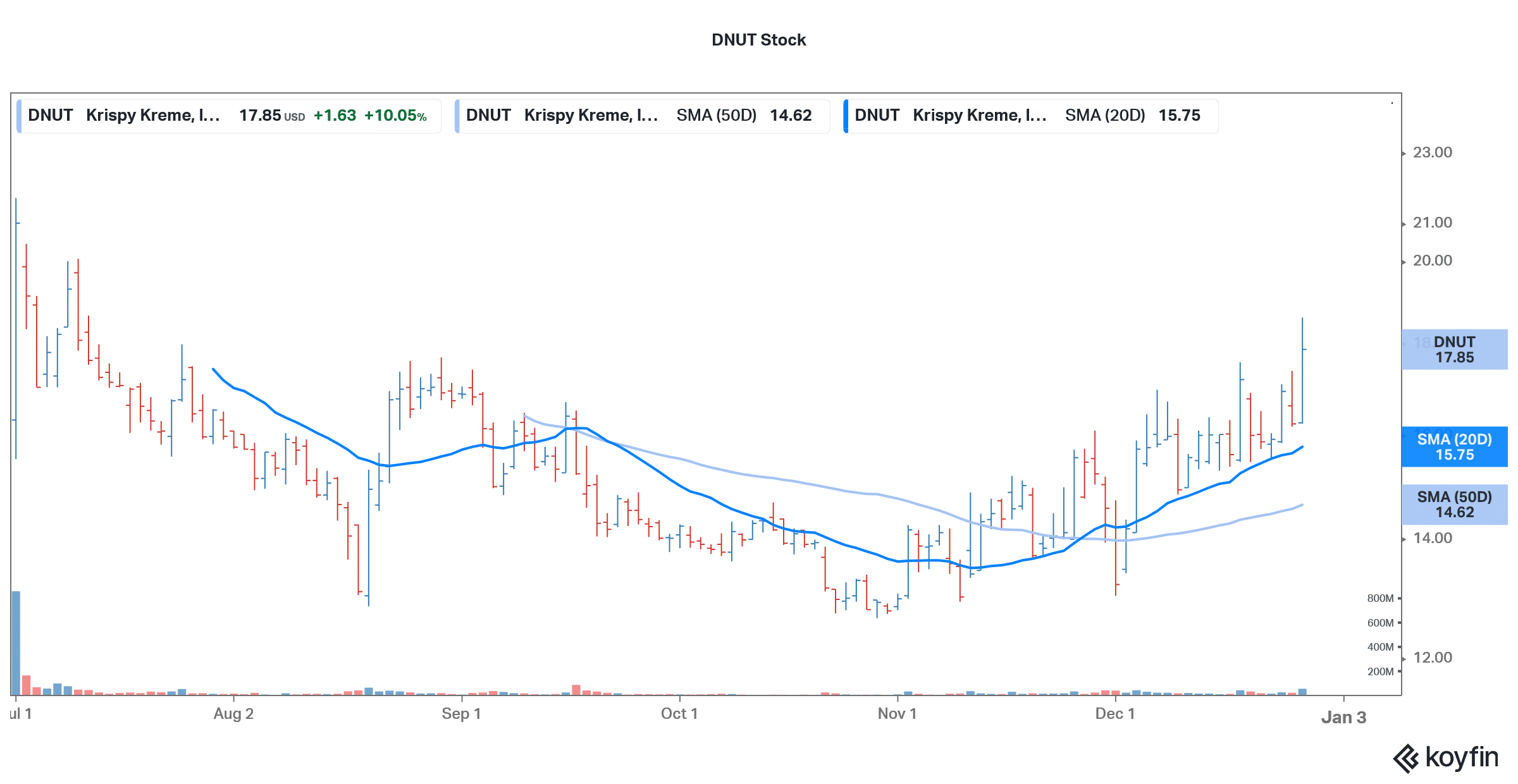

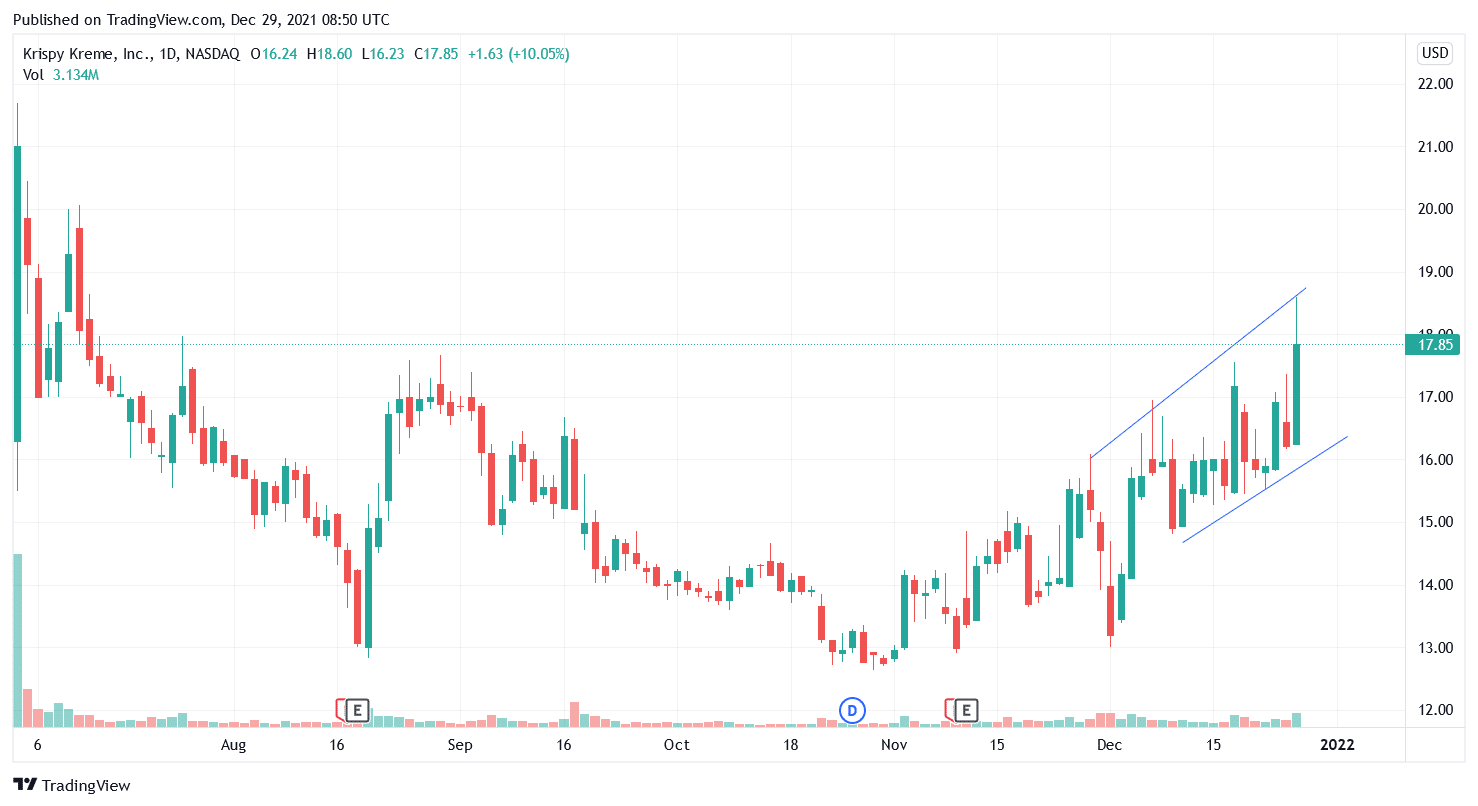

Krispy Kreme stock is looking bullish on the charts and trades above the 20-day, 30-day, and 50-day SMA. The stock has been in an upward trending price channel. The 14-day RSI (relative strength index) is a neutral indicator while the 12,26 MACD (moving average convergence divergence) gives a buy signal.

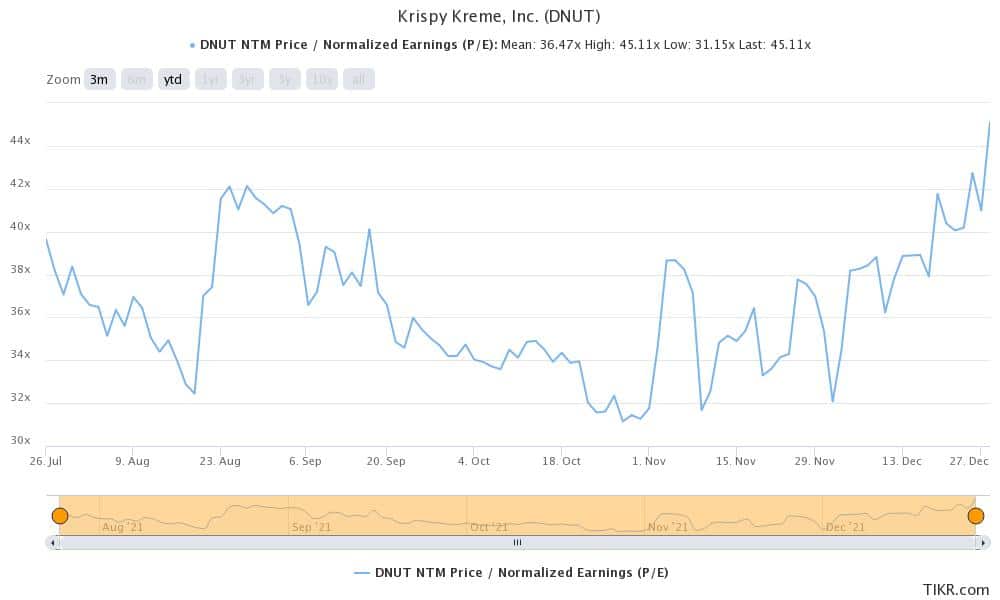

Meanwhile, Krispy Kreme’s valuation multiples have expanded amid the recent rise in its stock. It now trades at an NTM (next-12 months) PE multiple of 45x which appears a bit stretched, especially given the uncertainty emanating from the omicron variant.

While Krispy Kreme stock looks like a good buy for the long term, it might be prudent to take a staggered approach in buying as it might correct somewhat in the short term.

Buy DNUT Stock at eToro from just $50 Now!