Krispy Kreme Stock Price Forecast November 2021 – Time to Buy DNUT Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Krispy Kreme (DNUT) went public earlier this year only and has had a tough ride as a publicly-traded company. What’s the forecast for DNUT stock and should buy the dip in the stock?

Krispy Kreme priced the IPO at $17 per share, which was way below the original price range of $21-$24. Companies have to lower the IPO price when the market response is tepid to the IPO. Conversely, if the market response is favorable, companies hike IPO prices, at times multiple times during the IPO process. Meanwhile, despite having priced the shares below the guidance, Krispy Kreme trades at a discount to the IPO price. Here it is worth noting that it was the second listing for DNUT. It was a publicly-traded company until 2016 before JAB Holdings took it private.

Krispy Kreme recent developments

Last month, Krispy Kreme released its third-quarter earnings. The company reported revenues of $342.8 million in the quarter which were ahead of the $337.7 million that analysts were expecting. The company’s organic revenues, which excludes the now exited Wholesale business, increased 14% as compared to 2020 and 22% compared to 2019.

Sounding positive on the performance, CEO Mike Tattersfield said “Our third quarter results demonstrate the benefits of our omni-channel and global expansion strategy, which allow us to meet consumer demand with premium, fresh doughnuts, in a capital-efficient manner.” He said, “We are seeing positive momentum continue into the seasonally strong fourth quarter, as consumers sought out our sweet treats throughout October for Halloween and are expected to do so through the holidays.”

68% of all retail investor accounts lose money when trading CFDs with this provider.

DNUT is looking to increase prices

He also talked about DNUT’s pricing power and said that the company is considering more price hikes in the fourth quarter. US companies have been grappling with higher input costs which have been further amplified by the rising wage costs. Krispy Kreme’s net loss was $5.7 million in the quarter which was narrower than the $14.9 million that it had posted in the corresponding period last year.

Meanwhile, while Krispy Kreme posted a GAAP loss in the fiscal third quarter, it posted positive free cash flows of $11 million in the quarter. Organic cash flows coupled with the IPO proceeds helped the company lower its net debt. At the end of the quarter, its net leverage ratio was 3.7x which the company expects to fall below 3x over the next year. Over the long term, the company expects to maintain a net leverage multiple of 2x.

Labor issues

Meanwhile, the company talked about various headwinds during the earnings call. “Wage inflation is also impacting our costs as anticipated, along with labor shortages,” said Tattersfield. He added, “In particular, we’re seeing a lack of available drivers to run routes as we continue to build out our hubs and spokes.”

Meanwhile, the company has sought to downplay the impact of the labor shortage. “We don’t have an issue in the fresh doughnut business with growth when it comes to labor availability,” said COO Josh Charlesworth. The company has been on a hiring spree and added a record 2,100 employees in the third quarter.

Wall Street is not impressed with Krispy Kreme

While Krispy Kreme has sought to downplay the labor shortage issues which has been an industry-wide problem, Wall Street is not too convinced. Last week, Truist downgraded DNUT stock from a buy to hold and lowered the target price from $21 to $15. “Acute labor shortages and wage inflation currently occurring in the US will slow the company’s expansion of the company’s hub and spoke model and slow top line growth over the next few quarters. We believe slowing growth will, in turn, keep the stock’s valuation in check if not compress it further,” it said in its note.

Analyst Bill Chappell also pointed to DNUT’s previous stint as a publicly-traded company. He said, “While we believe the revamped model is a vast improvement, the company will need to prove that it can grow at a high rate for an extended period of time before it can be viewed as a growth company and fully shake off its historical baggage.”

Krispy Kreme stock forecast

Last month, HSBC had also downgraded DNUT stock from a buy to hold expressing concern over rising inflation. He also questioned the company’s strategy of moving from a franchise model to a company-owned model. Globally, QSR chains are moving to a franchise model which helps in better returns on capital.

Looking at the consolidated ratings, of the nine analysts covering Krispy Kreme stock, five have a buy rating while four rate them as a hold. It has a median target price of $19 which is a 31.7% premium over current prices.

DNUT stock long term forecast

Over the long term, DNUT is a play on deleveraging and the continued growth in business. While inflation is a short-term concern, the company has the good pricing power to pass on the increased prices to end consumers.

Should you buy Krispy Kreme stock?

Krispy Kreme stock currently trades at an NTM (next-12 months) PE multiple of 35.1x. The multiples don’t look high if the company can sustain its sales momentum and manage to protect the margins through price hikes.

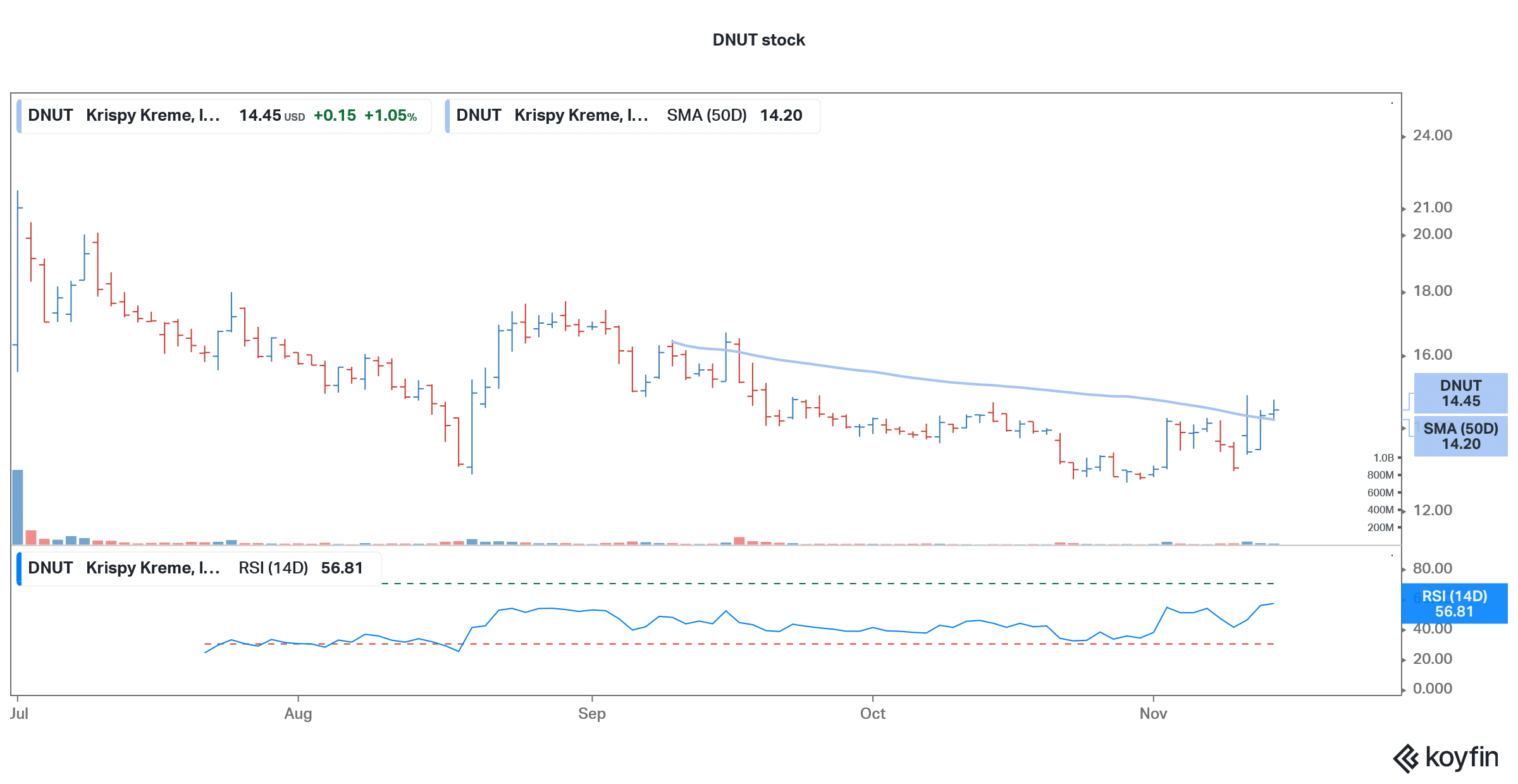

The stock is looking good on the charts also and trades above the 50-day SMA (simple moving average). The 14-day RSI (relative strength index) is 56.8 which is a neutral indicator.

Overall, if you are looking at a fast-growing QSR stock that can offer good returns in the medium to long term, DNUT should be on your watchlist.

Buy DNUT Stock at eToro from just $50 Now!