DoorDash Stock Price Up 20% Today – Time to Buy DASH Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

DoorDash (DASH) stock is trading sharply higher in US premarket price action today as investors gave a thumbs up to its quarterly earnings. The stock looks set to recoup some of its recent losses in today’s trading.

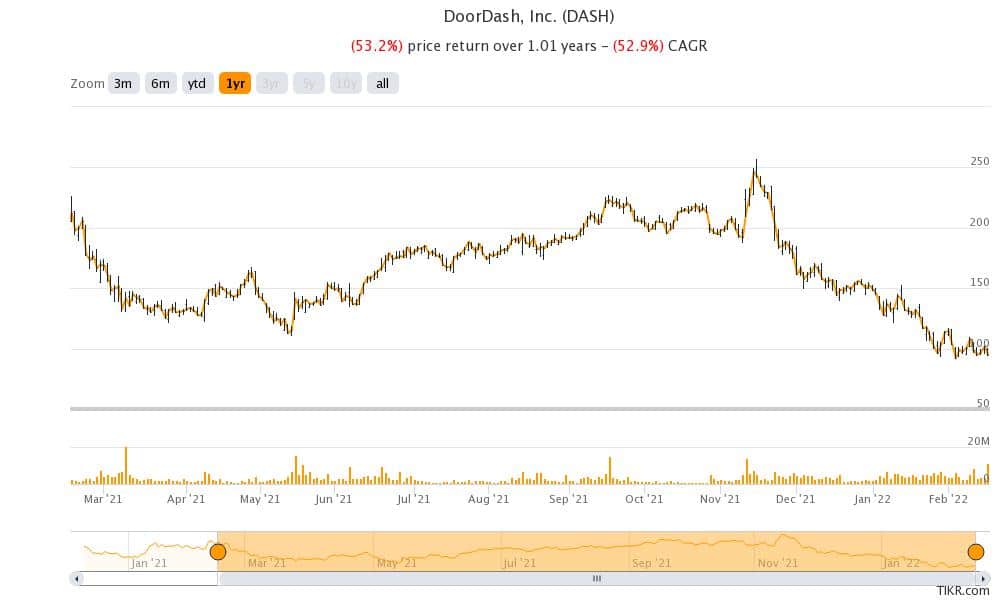

DASH stock has lost over a third of its market cap in 2022 as investors ditched growth names for the stability of mature companies. DoorDash stock is down over 67% from its 52-week highs amid the broader market sell-off. What’s the forecast for DASH stock and should you buy it now?

DoorDash IPO

DoorDash went public in December 2020. It was an exciting year for US IPOs and many doubled on the listing day. Both DASH and Airbnb went public in the same week and both the stocks soared on the listing day. DoorDash priced the IPO at $102 per share, which was way above the initial price range of $75-$85. The company had increased the IPO price range to $90-$95 during the IPO process itself. However, despite the bumped-up pricing, DASH gained 85% on its first trading day.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Analysts have been concerned about DASH’s valuations

DASH IPO pretty much sums up the mood in primary markets in the second half of 2020. Companies were generously increasing the IPO price and even it did not deter investors. Tech IPOs, especially growth companies that were witnessing a bump in sales due to the pandemic were in hot demand. DoorDash commanded a valuation of $39 billion in the IPO, which was over twice its private market valuation at the beginning of the year.

The stock went on to hit an all-time high of $257.25 in November 2021, However, it has since looked weak and now trades below the IPO price. Looking at the pre-market price action, the stock looks set to bounce above the IPO price today. That might not provide much succor to investors as the stock is still way below the all-time highs.

Many analysts were apprehensive about DASH

Even during the IPO process, some analysts were apprehensive of the kind of valuations that DoorDash was seeking. David Trainer, CEO of market research firm New Constructs, termed it “the most ridiculous IPO of 2020.” He pointed to increasing competition, lack of visibility of earnings, and a growth slowdown as the reasons for the bearish stance on the company.

DoorDash reported earnings

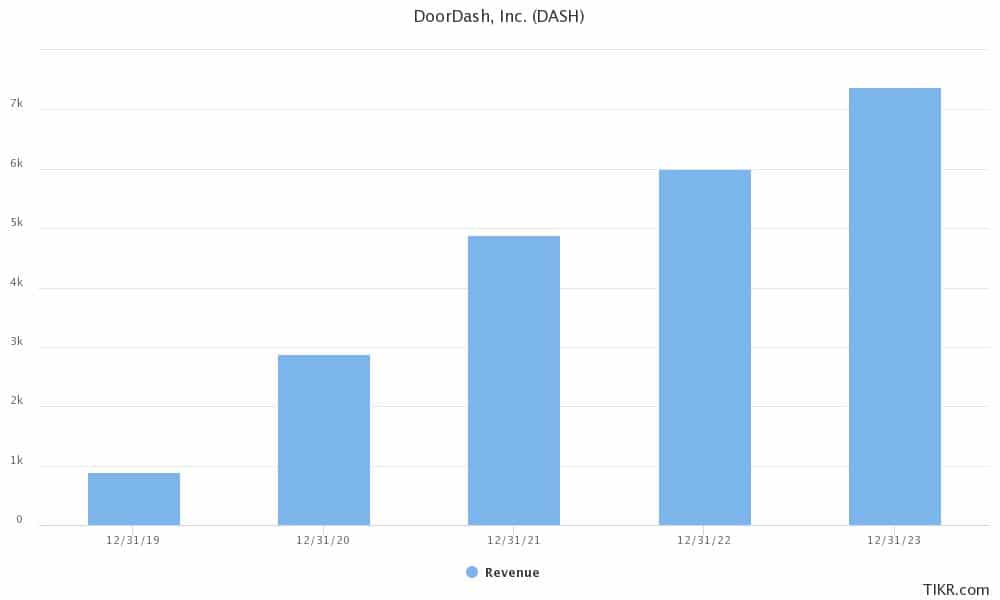

DoorDash reported its fourth-quarter earnings yesterday after the markets closed. The company reported revenues of $1.3 billion which were slightly ahead of the $1.28 billion that analysts were expecting. Its adjusted loss per share was 25 cents in the quarter, which was better than the 45 cents per share loss that analysts were expecting.

Its gross order value in the quarter increased 36% to $11.2 billion and was ahead of the $10.6 billion that analysts were expecting. The company fulfilled a total of 369 million orders in the quarter which was also higher than the 361 million that analysts were expecting.

DASH guidance

DASH expects its gross order value to be between $48-$50 billion in 2021, which was in line with analysts’ estimates. In the first quarter, the company expects gross order volumes between $11.4-$11.8 billion. In the full year, the company expects to post an adjusted EBITDA between $0-$500 million in the year. However, a breakeven on the net profit level still looks out of sight for the company. In 2021, its net loss widened to $468 million which was higher than the $462 million that it had posted in 2020.

Markets are concerned about a growth slowdown for stay-at-home winners like DASH which are now witnessing a tapering down of sales growth. Taking a swipe at pessimists, DoorDash CEO Tony Xu said “I think we’ve put to rest this question of what happens to demand when diners go back to eating in restaurants.”

The company’s CFO Prabir Adarkar said that growth has “normalized” but is still higher than the pre-pandemic levels.

Analysts on DASH stock

In January, Evercore ISI increased DASH’s target price to $256. “While most of our speculative Tech names have traded off due to interest rate scares, we are buyers of DASH given its strong growth fundamentals and reasonably impressive profitability among Online Food Delivery players,” said Evercore’s Mark Mahaney.

He believes that DoorDash is among the best positioned in the industry to reach profitability. “DASH is the only industry player expected to be profitable in 2022 … which we think will afford DASH more resiliency given potential interest rate hike,” said Mahaney in his note.

DoorDash stock forecast

Wall Street analysts have a split rating on DoorDash stock but it has a consensus buy rating. Of the 25 analysts covering the stock, 13 have a buy rating while 12 have a hold rating. The stock has a median target price of $200 which is a premium of over 110% over current prices. Its street low target price of $118 is a premium of almost 25% while the street high target price of $270 is a 185% premium.

Should you buy DASH stock

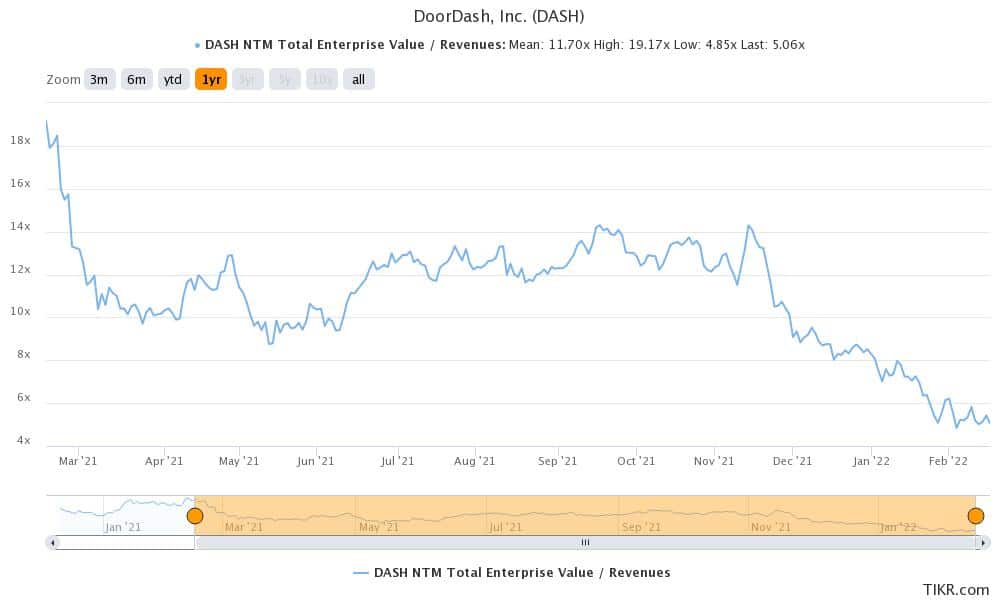

DoorDash stock now trades at an NTM (next-12 months) EV-to-revenue multiple of just above 5x which looks reasonable. DoorDash has been making new partnerships to increase the business. Last year, it announced that it would enter the instant grocery delivery business in New York City. partnered with beauty retailer Ulta Beauty for same-day delivery. Demand for delivery services has been gradually rising even as the growth rates are below pandemic highs. It is also acquiring Finland-based delivery platform Wolt in an $8 billion all-stock deal.

Today’s gains in DoorDash stock might not sustain as the earnings beat is not as spectacular. However, the valuations have now started to look attractive and it looks like a good buy for the long term.

Buy DASH Stock at eToro from just $50 Now!