CrowdStrike Stock Up 11% Today – Time to Buy CRWD Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of CrowdStrike stock is surging more than 11% this morning in pre-market stock trading action following the release of the firm’s financial results covering the fourth quarter of the 2022 fiscal year as both revenues and earnings exceeded Wall Street’s guidance for the period.

For the three months ended on 31 January 2021, CrowdStrike reported total revenues of $431.01 million resulting in a 63% jump compared to the same period a year ago. Subscription revenues were 66% higher during the period at $405.4 million. This figure exceeded analysts’ consensus estimate of $412.4 million for the quarter.

Annual recurring revenue (ARR) for the firm – a key non-GAAP metric – stood at $1.73 billion resulting in a 65% year-on-year increase.

Subscription gross margins ended 200 basis points higher than a year ago at 76% while, on an adjusted basis, they experienced a 100 basis points jump at 79%.

The firm’s negative GAAP operating margin declined 100 basis points at 5% on a year-on-year basis while CrowdStrike’s adjusted operating margin came in 600 basis points higher at 19% compared to a year ago.

Fully diluted GAAP earnings per share for the tech company stood at minus $0.18 while non-GAAP diluted EPS ended at $0.30 resulting in a 17 cents improvement compared to a year ago. Analysts’ consensus EPS for the period stood at $0.20.

For the next quarter, the company expects to report revenues of up to $465.4 million along with adjusted diluted earnings per share of up to $0.24. As for the entire 2023 fiscal year, the company forecasted total revenues of up to $2.16 billion and adjusted earnings per share of up to $1.13. All of these forecasted figures exceeded the Street’s consensus estimate.

The combination of above-expected quarterly figures and forward-looking estimates are probably the reason why CrowdStrike stock is surging this morning.

What could be expected from this cybersecurity stock after today’s strong earnings report? In this article, I’ll be assessing the price action and fundamentals of CrowdStrike stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

CrowdStrike Stock – Technical Analysis

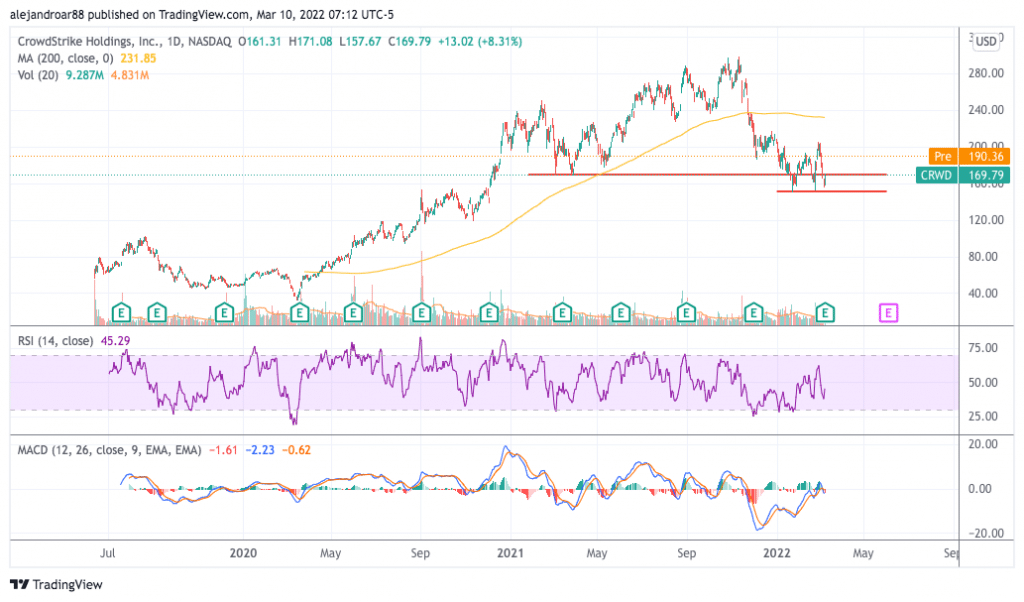

The price of CrowdStrike is down 17% so far this year while the stock is trading 43.1% below its 52-week high from November this year.

This decline has been prompted by a shift in macroeconomic conditions including a pronounced jump in US Treasury yields on the back of elevated inflation readings and an expected shift in the Federal Reserve’s monetary policy.

Even though the stock shed a portion of its value after reporting its Q3 2022 results, its financial performance has continued to be better than expected as it beat revenue and earnings estimates back then as well as it is today.

Just yesterday, the price of CRWD stock rose 8.3% ahead of the release of this report. This move resulted in a tag of the $170 horizontal support while this morning’s pre-market uptick is breaking above this important threshold.

The double-bottom formation highlighted in the chart could still be in play if today’s strong quarterly report ends up catalyzing a sustained jump in CrowdStrike stock.

However, momentum indicators are not fully favoring a bullish outlook as the Relative Strength Index (RSI) is standing at 45 (bearish) while the MACD is standing on negative territory and below the signal line.

Moving forward, the outlook for the stock depends largely on what happens after today. A sustained jump above the $170 mark could lead to another jump toward the $200 area resulting in a 17.7% upside potential based on yesterday’s closing price.

CrowdStrike Stock – Fundamental Analysis

CrowdStrike’s revenues have been growing at a fast pace in the past five years at least and even though growth rates are decelerating that is perfectly understandable considering that the company is now running a $2 billion per year business.

For 2023, CrowdStrike expects to grow its top-line results by nearly 60% while its GAAP operating margins have been progressively decreasing. Stock-based compensation remains an important item in the company’s cost structure representing at least 21.4% of the business’s revenues.

Last year, the company produced $427 million in free cash flows resulting in an FCF margin of 31.4%. If we assume the company will report a similar FCF margin of say 30% for the entire 2023 fiscal year, that would result in total free cash flows of $648 million.

Based on CrowdStrike’s current market capitalization of $38.95 billion, that would result in a forward P/FCF ratio of 60 and a forward P/S ratio of 18x.

Even though these metrics seem a bit stretched at first glance, they appear to be justified if one considers the fast pace at which the company has been growing. Meanwhile, the firm’s long-term debt is quite conservative at $739.5 million on total assets of $3.6 billion including $2 billion in cash and equivalents.

All things considered, the latest decline in CrowdStrike stock has made this tech stock a more appealing investment opportunity in the up-and-coming cybersecurity industry.

Buy CRWD Stock at eToro with 0% Commission Now!