India’s Chit Fund Crisis: Indicative Of A Global Market Failure?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The recent chit fund scam in India saw thousands of depositors, mostly poor people in villages and small towns, lose their hard-earned money after Saradha Group, who were believed to be running a wide variety of collective investment schemes, collapsed. As the case demonstrates, there is still a clear need for more transparency, corrections & regulations in not just India, but at the highest levels of global financial markets.

The recent chit fund scam in India saw thousands of depositors, mostly poor people in villages and small towns, lose their hard-earned money after Saradha Group, who were believed to be running a wide variety of collective investment schemes, collapsed. As the case demonstrates, there is still a clear need for more transparency, corrections & regulations in not just India, but at the highest levels of global financial markets.

So chit funds are back again in news and unfortunately for wrong reasons. Our sympathies with the hapless citizens robbed by Saradha(a chit fund company) and other such funds. Also it is time for some serious introspection to mitigate risk for the investors; and identify and fix the real reasons behind the mushrooming of such funds across India.

The biggest reason has been the failure of our banking network to channel funds for the needy customers. Dearth of such institutional options has exposed the gullible customers to Chit Funds and other similar formats for higher returns and need for funds – Not to say that they are all useless, but surely a risky option considering the way the funds are managed.

The story unfolding in the last two weeks leaves us with mixed feelings. On one side, we feel sorry for the helpless investors; yet we wonder if they should have been more prudent. Also a sigh of relief for the fact that we don’t have to deal with such risky instruments.

But is our assumption valid that regulations are only required at such small levels of chit funds? And are we not overconfident that our monies are safe? And is our knowledge sufficient enough to assume that our funds have no threats? There are lots of such questions we must evaluate for the safety of our hard earned money.

[quote]To my mind there is more need for transparency, corrections & regulations at the highest level (which includes the central bank and the most powerful financial institutions) than any other. Because what we have witnessed in the last five years is a clear testimony of the perils of unbridled markets. And it has shown us repeatedly that irrespective of whether the market, product or process is regulated or unregulated; our effort to manage it has failed. At the same time the financial markets have always resorted to subterfuge coming up trumps while leaving the globe scathed.[/quote]In fact, the issues pertaining to financial markets are so pressing that if not addressed with utmost priority, it can plunge the whole world into darkness. And hence it is just not the fate of these small investors of chit funds but the entire globe, which is at risk of being pushed to bankruptcy again. And there are enough evidences from recent past to highlight the efficacy of the above claim.

Table of Contents

The Gold Plunge

Let us start with the recent example of gold price plunge. In India and across the globe, a huge number of households (middle class and above) hold gold in some form or the other. And the nature of gold (as an asset) is such that its price is expected to grow with time and so attaches a notional value of increasing returns with time. Given the universal acceptance of this asset, should it not be obvious that the price movement of such a product be determined by market forces (demand and supply) only? It has been some time now since gold price almost capitulated 15 percent in 2 days but the jury is still out on it.

There is no one reason that two authorities would agree upon. Such is the nature of collapse that one does not know whether to buy, hold or sell it. Does it not leave us all vulnerable to the vagaries of financial markets, especially when there are forces beyond market dynamics working round the clock to run down our assets?

Related: Cyprus Finance Minister Admits To Plans To Sell Gold Reserves

Related: Infographic: Should You Invest in Gold?

But wait; because the rabbit hole goes a little deeper and we must go further down to know for sure how bad the mess is; and how things are absolutely out of our control.

The Wild West

We just spoke about the unregulated world of chit funds without appreciating the fact that they are so innocuous compared to the complex fancy products used so rampantly in the West.

One such “unregulated” product is CDS (Credit Default Swap). Warren Buffet calls it “the financial weapon of mass destruction”. If Chit Funds can fleece some thousand odd, CDS can bring down few nations.

CDS can be simply understood as an insurance undertaken on bonds to hedge against the issuer defaulting. Sounds mundane and harmless, but get into the complexity of it and you would have to bite the bullet. In fact, the entire Eurozone is still reeling under the dark clouds of CDS, notably an unregulated product with trillions of dollar exposed to it. It has all the potential of bringing back the memories of 2008-09. So doesn’t it warrant the authorities to immediately diffuse this time bomb at the earliest; or ideally not allow such products to hit the market?

Related: “Naked Truth” on Default Swaps on Wall Street and Germany

Having said that, it is just not the unregulated products, which are doing the damage. In fact the ones, which are regulated, are equally failing us.

Almost a year ago, a huge scam called the LIBOR Gate was uncovered. LIBOR as we know is a benchmark interest rate of the world issued by the top 18 banks; and apparently decides the interbank and commercial lending rates of all kinds across the globe. It is a dynamic rate, which is the average of daily borrowing rate of each bank with other banks. Close to $10 trillion of loan and $350 trillion of derivatives are tied to it.

This so called haloed rate was never ever questioned before the story broke out that it was being rigged; that certain banks including Barclays, RBS et al were manipulating the rates for their benefits. That so much was hinged on it, that even a small fraction of a percentage here and there would mean a scandal of billions of dollars.

This presumably has shaken most nations and the credibility of London as a financial hub has taken a big beating. Already hundreds of lawsuits have been filed against these banks amounting to billions of dollars. The matter is so serious that even some municipalities & U.S states have sued these banks for deceit.

When such rip offs can impact states and nations, how can individuals and their money be safe? While this was uncovered almost a year ago, a few days back another disaster came out tumbling regarding the interest rate swaps being manipulated. And this would mean that there was manipulation on interest rate (Swap Rate) on interest rate (LIBOR rate); and that too when close to $500 trillion is hinged to it. Knowing all this is extremely suffocating and leaves us with a feeling of helplessness. And much more distressing is the fact that these are just some private hands directly in control of our monies and our fate.

Related: Post-Libor – Why Bankers Now Face A Legitimacy Crisis: Simon Johnson

Related: Libor Manipulators ‘Should Face Prosecution’: UK Regulator

But the icing on the cake goes to the sub-prime crisis (2008-09) since it all happened under the nose of the regulators; allegedly a party itself in brewing the crisis. All across the globe millions of people lost their jobs, homes and livelihood. They lost money on equities, real estate, commodities, and whole host of products and assets.

Such was the impact that the world was brought to a screeching halt. The buck for the damage clearly stopped at the investment banks. The primary reason was bundling of sub standard mortgages with high rating and hedging them multiple times. The regulators almost were blind eyed and approved of whatever came to their desk. And later on, despite a clear understanding of why and how things went wrong, nothing was done to either correct the model, or to book the perpetrators. The aftermath of the crisis was much more shocking. The bankers who unleashed this calamity got rewarded with incentives and bonuses which actually came from tax payer’s money. This was evidence enough of regulators ineffectiveness and proved once again how toothless it had come to be.

And last but not the least was the food crisis post 2008-09 which led to astronomical increase in food prices (more than 60 percent) in a short period of two years. In countries like Kenya, Somalia, Algeria, Libya, Egypt, Haiti people came on to streets voicing their resentment against the rising food prices. It started with food riots and eventually shaped into full-fledged revolution leading into regime changes. But did the price of food actually increase because of low production? The answer is “No”. It was driven by speculation which we know as futures market. Have we not recently felt the pinch of rising food prices in India? Now isn’t this surprising that the producer of food does not decide the price but the hoarders and speculators do.

[quote]So talks about interventions at such small levels of chit funds are just cosmetic when the entire money & commodity market is rigged & manipulated. Doesn’t the entire system deserve a thorough scan and correction? Until that happens can we live without the threat of losing our jobs, monies and assets? And our silence in not raking up the issue with the desired intensity is only making the matter worse. [/quote]The Impending ‘Financial Tsunami’

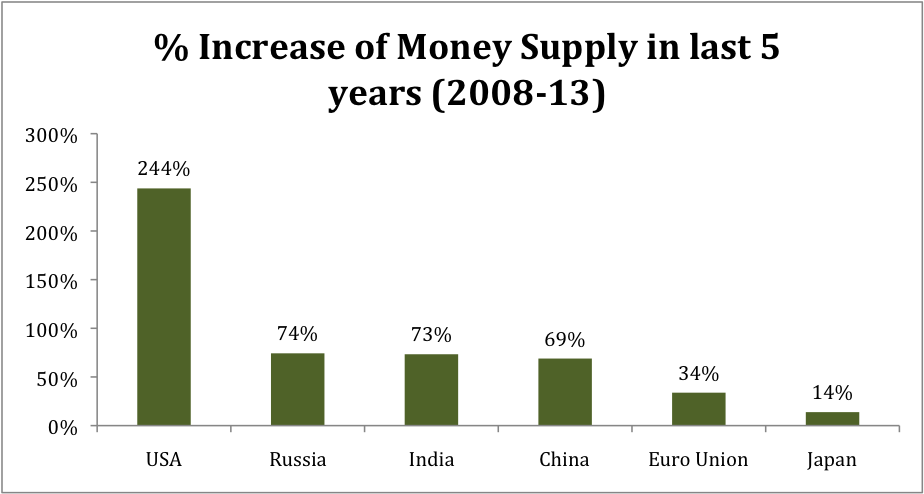

The story would be incomplete without the mention of this impending crisis, – “the biggest financial tsunami”, which is likely to hit us in coming time. In the last 5 years or so, all the big nations have printed and circulated trillions of dollars to clear their way out of trouble. The graph below indicates the money supply growth in local currency in the last 5 years. Japan, which appears humble in the chart, plans to double its monetary base in two years. There is evidently enough nervousness in the market because of this. Fed has shown clear reluctance in continuing with quantitative easing because it does not seem sustainable.

A “currency war” is already underway to gain price advantage over others. It surely is an ominous sign for the globe and can unfold into the worst known man made financial crisis. Just looking at the current global health it is obvious that this money printing business can easily translate into hyper inflationary trends culminating into money contraction leading to deflation. And the consequences would be like an epidemic capable of wiping out the entire values of our holdings (money, assets, commodities, etc). The signs of it we have already seen in countries where inflationary food prices culminated in regime changes. But still the realization has not dawned on us that we are being fooled and robbed by this crooked lobby (private bankers and central banks) which just works for private gains. Unfortunately we did not bother to correct the issue last time, and so the chaos has deepened further.

Related: Capitalism’s Pallbearers: The Companies That Run, & Could Destroy, The Global Economy

Related: Undoing the Bankruptcy of Capitalism: Joseph E. Stiglitz

Given the current mess, it actually might take generations to clear this out. Till that happens some short term measures are an immediate priority and order of the day. One of them is recall of Glass Steagall Act to separate the investment banks from the commercial banks. Other could be tightening the noose around unregulated products, which could mean a clear mandate for banks to hold a minimum reserve before committing themselves to such portfolios. And there are many more such fundamental changes which need to be brought in provided we realize that the current financial models, processes, and markets have not worked and have done more harm than good. And this can only happen if there is education on the subject and increasing discussions around the issues at all levels.

By Sumit Singh

Sumit Singh is currently working as a faculty with St. Joseph’s College of Business Administration in India. Singh holds an MBA in Marketing, with 11 years of Corporate Experience in companies like Bharti Airtel Ltd, ICICI Bank Ltd, Pizza Hut, Manipal Global Education & Lifestyle International Pvt Ltd.

Got something to say about the economy? We want to hear from you. Submit your article contributions and participate in the world’s largest independent online economics community today!