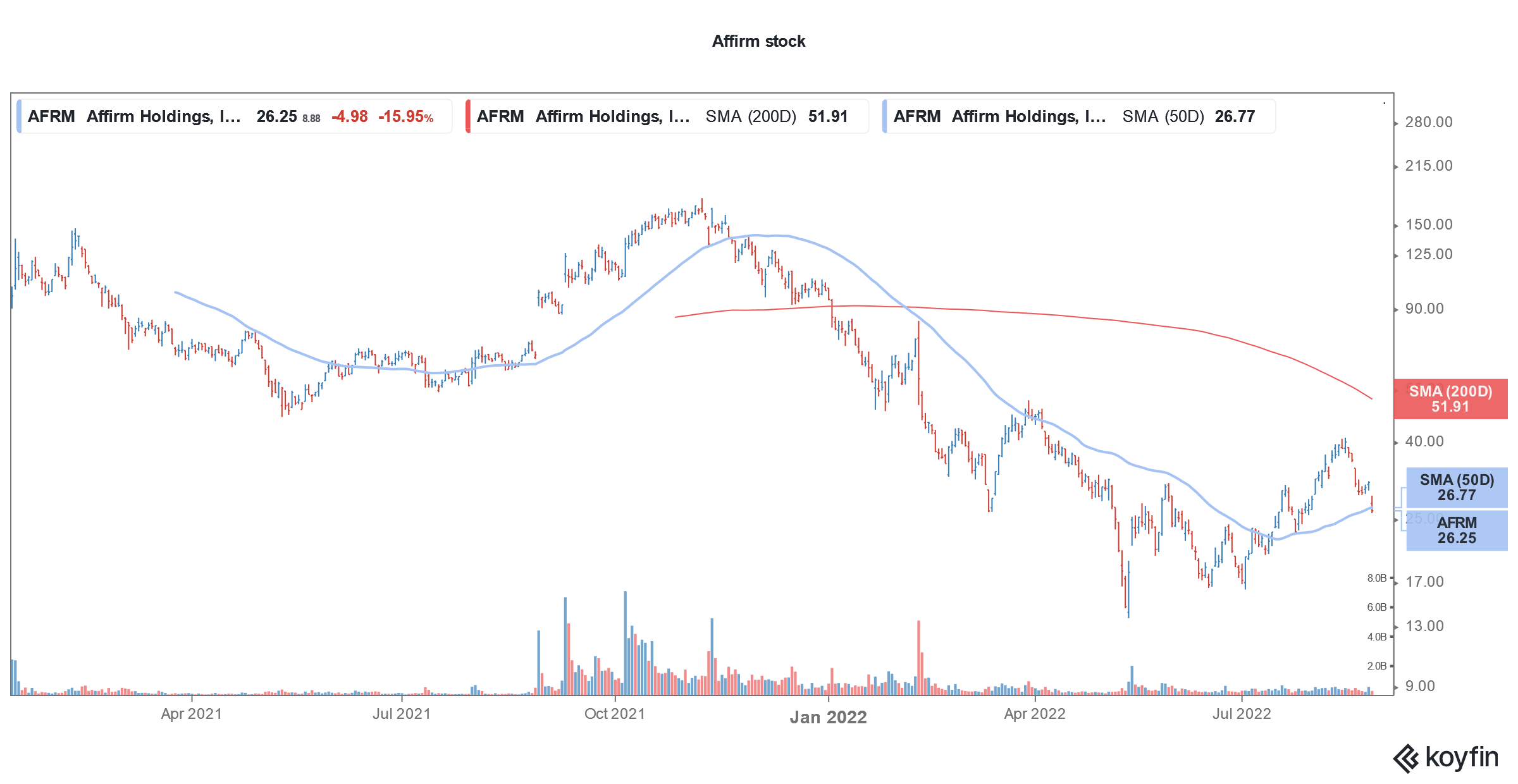

Affirm Stock Tumbles on Massive Loss & Tepid Revenue Guidance

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Affirm (NYSE: AFRM) stock is trading sharply lower in US price action today after it posted a massive loss in the fiscal fourth quarter of 2022 and gave lower-than-expected guidance for the fiscal year 2023.

In its fiscal fourth quarter of 2022 which ended in June, Affirm reported revenues of $364.1 million, which were 39% higher YoY. The metric however was slightly below what analysts were expecting. However, its per-share loss increased from 38 cents to 65 cents over the period and was higher than the 58 cents that analysts were expecting.

Fintech earnings

Affirm’s earnings are in stark contrast to SoFi, another fintech company that listed in 2021. SoFi not only posted better than expected earnings and revenues but also raised its revenue guidance for the full year.

Affirm is a BNPL (buy-now-pay-later) company. The industry has been attracting a lot of interest from financial as well as tech companies. Last year, AFRM announced a partnership with Amazon under which buyers on the platform would be able to able to pay using Affirm’s flexible payment options. It expanded the partnership later in the year and would remain Amazon’s exclusive BNPL partner for 2022.

Affirm partnered with Amazon

Amazon has been expanding its partnerships and earlier this week entered into an agreement with Peloton under which the latter would sell its products on Amazon. Meanwhile, the deal with Amazon hasn’t been as pathbreaking for Affirm as markets had initially expected.

Apart from Amazon, Affirm has also partnered with several other companies like Peloton and Shopify.

Affirm gave lower-than-expected guidance

Affirm guided for revenues between $1.63-$1.73 billion in the fiscal year 2023 which was well short of the $1.9 billion that analysts were expecting. For the fiscal first quarter, it gave revenue guidance of $345-$365 million which was also short of the $386 million that analysts were expecting. Commenting on the guidance, Affirm’s CFO Michael Linford said, “In light of the uncertain macroeconomic backdrop, we are approaching our next fiscal year prudently.”

He however said that the company expects its profitability to improve in the fiscal year 2023 and forecasted “a sustained profitability run rate, on an adjusted operating income basis, by the end of fiscal 2023.”

Affirm’s active customers more than doubled to 14 million in the quarter while active merchants rose to almost 235,000. It reported a 139% increase in transactions of which 85% were from repeat customers.

Affirm reported better than expected GMV

The only bright spot in Affirm’s earnings was the 77% increase in GMV (gross merchandise value). The metric came in at $4.4 billion which was ahead of the $4.08 billion that analysts were expecting.

The BNPL space saw a lot of action last year. While Apple was rumored to enter the industry, Square, which is now known as Block, went ahead and acquired Australian BNPL company Afterpay. The deal was at a massive premium and signaled the massive appetite for BNPL companies.

Credit quality

While Affirm was optimistic about its credit quality, delinquencies might increase amid a slowing US economy. In response to an analyst question on the stress in credit quality, Linford said that the situation is “extremely manageable.”

After the earnings release, RBC lowered its target price for Affirm. However, Morgan Stanley reiterated its overweight rating. It said, that Affirm “is pushing through economic and credit cycle turbulence, even if those forces are having modest adverse impact on near-term growth trajectory.”

Rising interest costs

Meanwhile, Affirm stock fell even deeper into the red after Fed chair Jerome Powell reiterated that the US Central Bank would continue to raise rates to tame inflation. Last Friday also, US stocks slumped after Fed July minutes dashed hopes of a Fed pivot from rate hikes to rate cuts.

The Fed has raised rates four times this year including two consecutive 75 basis point hikes. As interest rates rise, borrowing costs for BNPL companies would also rise