Zoom Stock Down 14% in February – Time to Buy ZM Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Zoom stock has gone down 14% in February as market sentiment toward former pandemic winners and growth stocks as a whole has shifted amid an expected change in the macro landscape.

Just yesterday, the California-based video communications company reported its financial results covering the fourth quarter and entire 2021 fiscal year. For the three months ended on 31 January, revenues landed at $1.07 billion resulting in a 21% year-on-year jump compared to the same period a year ago. This figure was $20 million higher than the market’s estimate for the period.

The number of customers paying over $100,000 in the past twelve months – a key operating metric – ended 66% higher compared to the previous year at 2,725 while customers with over 10 employees actively using the communications tool went up 9% at 509,800.

The firm’s GAAP operating profit slightly decreased to $251.8 million compared to the $256.1 million the firm reported a year ago. This resulted in GAAP operating margins of 23.5% that were 550 basis points lower than the previous year. On an adjusted basis, the operating margin slid 170 basis points at 39.2%.

Net income for the quarter stood at $490.64 million resulting in an 88.2% year-on-year jump. GAAP diluted earnings per share landed at $1.60 while non-GAAP EPS ended at $1.29 or 7 cents higher than Q4 2020. Analysts were expecting adjusted EPS of $1.05 for the period.

Zoom guided for revenues ranging between $1.07 and $1.075 billion for the first quarter of 2022 – slightly lower than the market’s consensus estimate. Meanwhile, for the entire 2022 fiscal year, the firm expects to produce between $4.53 and $4.55 billion in revenue – a figure that was also $160 million lower than the market’s consensus forecast for the period.

Additionally, Zoom announced that its Board of Directors approved a $1 billion share buyback program that will end on February 2024.

The combination of below-expected guidance and decelerating top-line growth seem to be the reason why Zoom stock is down nearly 4% today in pre-market stock trading action.

What could be expected from this tech stock after yesterday’s earnings report? In this article, I will be assessing the price action and fundamentals of Zoom stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

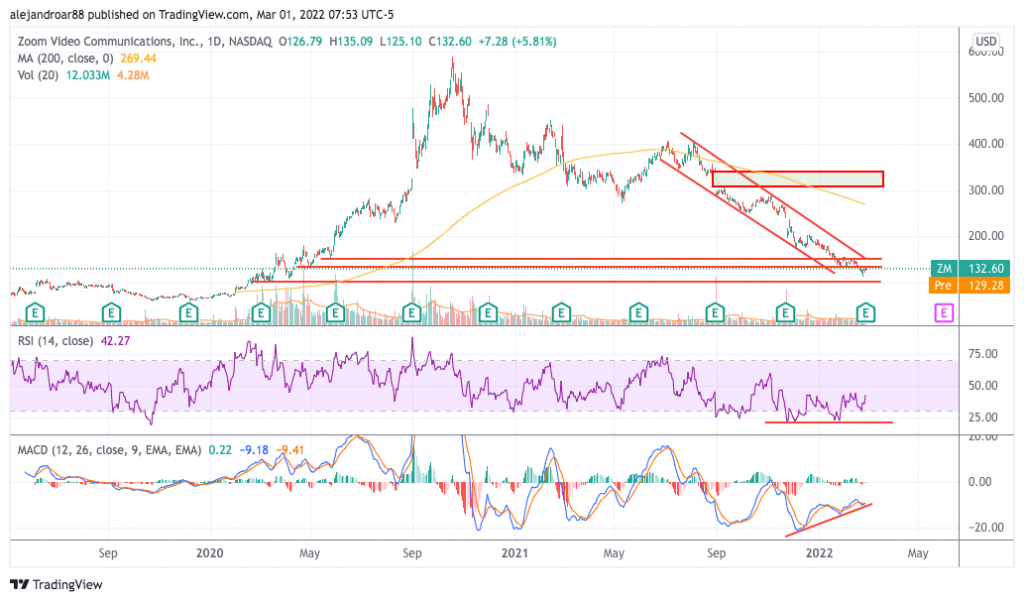

Zoom Stock – Technical Analysis

The price of ZM has declined nearly 28% so far this year while the stock is trading almost 70% below its 52-week high of $440 per share.

This decline has been prompted by multiple negative catalysts including a fading COVID tailwind, the company’s potential struggle to beat its pandemic-era comparables, and a shift in macro conditions including the possibility of multiple interest rate hikes taking place this year in the United States.

The stock remains on a clear downtrend as indicated by the chart above and multiple areas of support have been broken in the past few weeks. That said, there are some reasons to believe that Zoom stock may have bottomed already or could be about to.

In this regard, momentum indicators are displaying bullish divergences. First, the Relative Strength Index (RSI) has not made a lower low since November last year despite the price moving lower. Meanwhile, the MACD has been on an uptrend since then despite the price collapsing.

This means that the strength of the negative momentum that the stock has experienced lately is declining and that favors the view that the price could be nearing a short-term bottom.

Moving forward, the $100 level remains the most relevant area of support to watch while the stock should break above $150 before a bullish short-term outlook can be confirmed.

Zoom Stock – Fundamental Analysis

Revenues for Zoom went up 54.7% last year while net income more than doubled. Net margins also expanded significantly on a year-on-year basis to land at 33.6% on a GAAP basis.

Meanwhile, for this fiscal year, the company is expected to report sales of up to $4.55 billion resulting in an 11% year-on-year jump.

As growth seems to be stalling, Zoom could be progressively becoming more a value stock than a growth stock. Last year, the company produced $1.47 billion in free cash flows resulting in an FCF margin of 35.8%.

Moving forward, based on the company’s forecasted sales for this year, Zoom’s FCF-generation capacity could grow to at least $1.6 billion.

Based on its market capitalization of $39.5 billion by the end of yesterday’s session, the company is trading at 25 times its forecasted free cash flows. This is a decent valuation multiple for a business with sound fundamentals such as Zoom.

However, it is important to note that Zoom faces multiple challenges from a business development standpoint as competition is heating up and the firm needs to find ways to keep growing its top-line results without necessarily harming its current earnings and cash-flow generation capacity.

Depending on how the management tackles these challenges in the future, the valuation might either suffer or be benefitted. For now, there is room for further negative volatility down the road as the company seems to be trading close to its fair value.

Buy ZM at eToro with 0% Commission Now!