American Airlines Stock Down 4% – Time to Buy AAL Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of American Airlines stock declined 4% yesterday despite the recovery seen by broad-market indexes after Goldman Sachs conducted a review of the price targets and recommendations for US airlines.

The American investment bank downgraded AAL stock from Neutral to Sell while it slashed its price target from $19 to $18 per share upon highlighting that the company’s elevated operating leverage and weaker mid-term pricing capacity may slow down the pace at which it will swing to profitability.

“We remain positive on the path to profitability recovery for the airlines over the medium-term, but we are reducing our Dec Q 2021/2022 outlooks due to higher fuel/worse short-term revenue trends. Heading into 2022, we are forecasting capacity growth to be elevated and for pricing to lag the recovery in traffic”, stated Catherine O’Brien, the analyst who covers AAL stock on behalf of Goldman.

Could this downgrade plunge AAL stock once again to the $18 level or will market participants ignore this report and keep pushing the price higher on the back of the progressive recovery of the industry?

In the following article, I’ll be assessing the price action and fundamentals of American Airlines stock to possibly answer that question.

67% of all retail investor accounts lose money when trading CFDs with this provider.

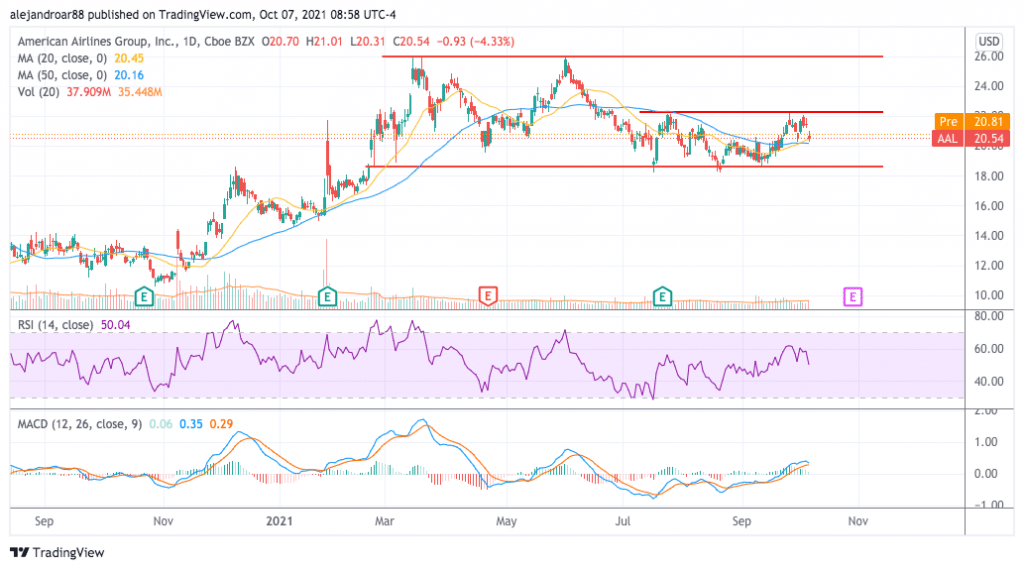

American Airlines Stock – Technical Analysis

The price of American Airlines successfully bounced off its $18 horizontal support on 13 September and had advanced more than 10% since then until this report from Goldman came out.

However, the bounce seems to have been short-lived as the price rejected a climb above the $22 level possibly due to the downbeat tone of this Goldman report.

At the moment, AAL stock is finding support at the 50-day moving average and there is a confluence of three simple moving averages at the current level (20-day, 50-day, and 200-day SMAs).

If the stock bounces off these supports, chances are that another jump toward the $22 level will end up breaking that resistance as that will signal the market’s confidence about the long-term outlook for the stock.

Trading volumes were particularly high yesterday but the share price closed above the session’s low.

Meanwhile, the MACD is pointing to a bearish outlook as positive histogram readings have been steadily declining while the oscillator seems poised to cross below the signal line – typically a sell signal. Moreover, the Relative Strength Index (RSI) is standing at 50 but heading downwards.

Moving forward, the directional path is unclear until we either get a break below the $20 level (bearish) or a strong bounce off this support and a jump above the $22 area (bullish).

American Airlines Stock – Fundamental Analysis

The situation for airlines is still worrying as the rapid spread of the Delta variant is still weighing on the industry’s short-term outlook. However, most of these companies have already seen the demand for their services recover to around 60% or more of pre-pandemic levels. That said, their future profit-generation capacity is still a concern.

Only a few days before Goldman’s report hit the Street, Morgan Stanley shared a positive view about the commercial aviation industry citing waning COVID-19 concerns as a short-term tailwind for stock prices.

“We believe the airline stocks are now poised at a point similar to Oct. 2020 and Feb. 2021 – just past peak sentiment fears when incremental positive headlines drove strong buying in the space”, analysts from MS stated in a note to clients on 4 October.

They added: “We believe peak COVID fears for investors were probably in late August and we have already seen the stocks react positively to headlines on international reopening, the COVID ‘pill’ and even negative pre-announcements”.

The COVID “pill”, as they called it, is the molnupiravir treatment that could be soon introduced by Merck (MCK) upon obtaining positive results during Phase 3 trials. This treatment could be a game-changer for the industry as it will be the first FDA-approved antiviral against the virus.

The combination of en-masse vaccinations and an available treatment for the disease should eventually dissipate concerns about a prolonged impact of the virus in the demand for air tickets and that could have a positive effect on valuations in the near future.

According to American’s latest quarterly report, sales are expected to be 20% below pre-pandemic levels for the third quarter of the year while pre-tax negative adjusted profit margins should range between 3% and 7%.

The company’s long-term debt is at least 70% higher than it was before the pandemic and this means that higher interest expenditures will likely weigh on the firm’s profitability in the future.

By the end of 2019, American’s normalized diluted EPS landed at $4.09 per share. Even in a pessimistic scenario where AAL reports half of that figure in future dates the resulting forward price-to-earnings ratio would be 10 based on yesterday’s closing price of $20.5 per share.

This conservative valuation, the firm’s large cash reserves, which should eventually be used to reduce its outstanding debt commitments, and other positive factors point to American Airlines stock as a relatively undervalued airline stock.

Buy AAL Stock at eToro with 0% Commission Now!