5 Best Airline Stocks to Buy in July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Airlines have been one of the most battered segments of the economy during the pandemic, with the health crisis forcing all of these companies to take significant debt to boost their liquidity in order to survive the crisis.

Now that the world is progressively heading out of the contingency on the back of en-masse vaccinations, the following five picks display attractive pre-pandemic profitability margins and robust balance sheets to possibly deliver solid gains in the following years.

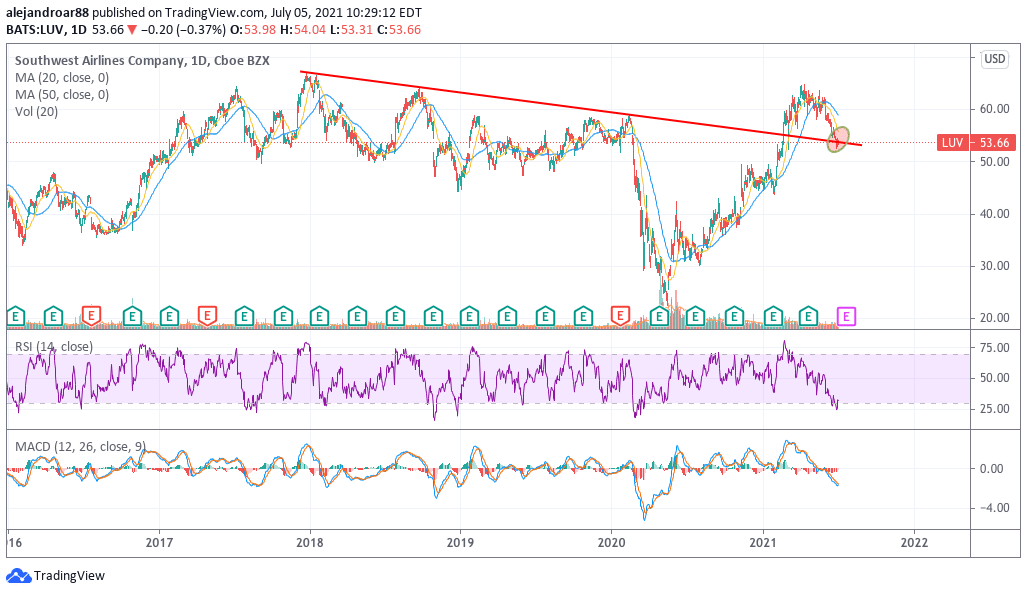

1. Southwest Airlines (LUV) – Top airline pick

Before the pandemic stroked, this US-based low-cost airline had been proud of delivering positive earnings for more than 35 consecutive quarters amid its relentless focus on operating efficiently.

However, the pandemic forced the company to swing to losses temporarily during all fourth quarters of 2020 although it has started 2021 on a positive tone as it has swung to profitability once again.

Before the pandemic, Southwest managed to grow its sales from $12.4 billion to $15.4 billion from 2015 to 2019 at a 4.4% CAGR. Meanwhile, even though profit margins declined steadily during that same period, the firm’s net margin landed at 10% by the end of 2019 – the best among its peers.

Meanwhile, despite having to resort to a significant amount of debt to withstand the pandemic downturn, Southwest’s balance sheet remains conservatively financed with long-term debt of around $12 billion on total assets $35.5 billion including $14.35 billion in cash and equivalents that may not need to be used if the firm keeps generating profits and positive operating cash flows moving forward.

At the moment, Southwest’s cash at hand accounts for 45% of the firm’s $32 billion market cap while the airline managed to ramp up its revenues to $2.05 billion in the last quarter. Meanwhile, analysts are expecting to see sales landing at $15.2 billion by the end of the year which would result in a price-to-sales (P/S) ratio of 1.1 – a fairly conservative multiple for a company that has such an outstanding track record of profitability.

Chances are that, once the pandemic is fully over, valuation multiples for Southwest will continue to expand on the back of a renewed confidence in the firm’s ability to thrive in a post-virus scenario.

67% of all retail investor accounts lose money when trading CFDs with this provider.

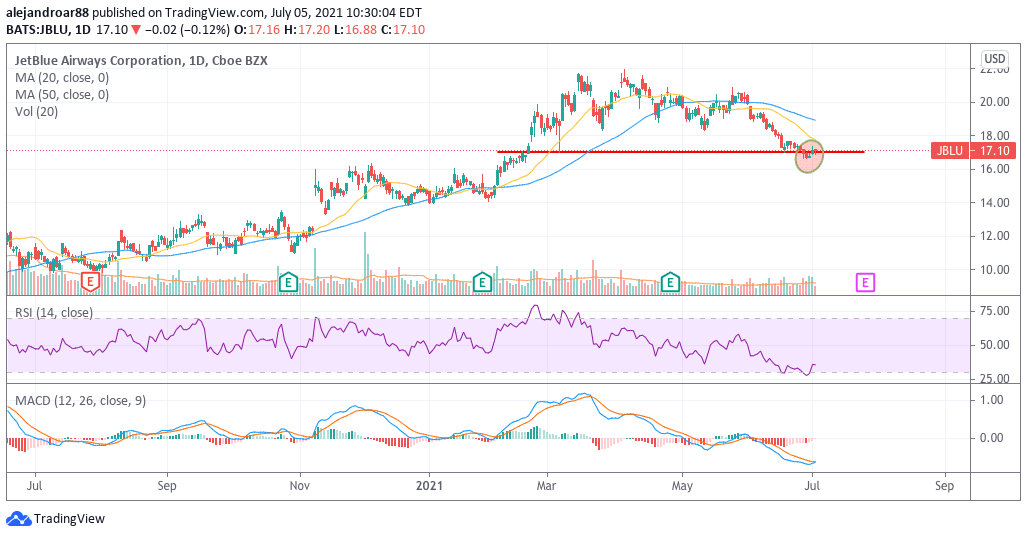

2. JetBlue Airways (JBLU)

Before the pandemic stroked, this New York-based airline had managed to grow its top-line results at a 6% CAGR from 2015 to 2019, with total sales landing at $8.09 billion by the end of that period.

Meanwhile, the company displayed robust gross profit margins of around 35% even though net profit margins were fairly volatile. As for its solvency, JetBlue’s balance sheet by the end of the first quarter of 2021 showed long-term debt of $5.3 billion on assets of $13.7 billion including $3.23 billion in cash and equivalents.

Although the company kept posting losses during these first three months of 2021, sales have progressively recovered to $733 million by the end of this period while analysts expect that the firm should swing to profits by the second quarter of 2022.

At the moment, the company’s cash accounts for almost 60% of its valuation, which results in a P/S ratio of 0.27 times Jet Blue’s 2019 sales and a P/E ratio of 4 times the firm’s 2019 earnings.

Even if one believes that JetBlue will manage to post earnings in 2022 of only a quarter of its 2019’s bottom-line results of $569 million, that would still result in a conservative P/E multiple of 15 – excluding cash – for a firm’s whose business has delivered solid profit margins in the past.

67% of all retail investor accounts lose money when trading CFDs with this provider.

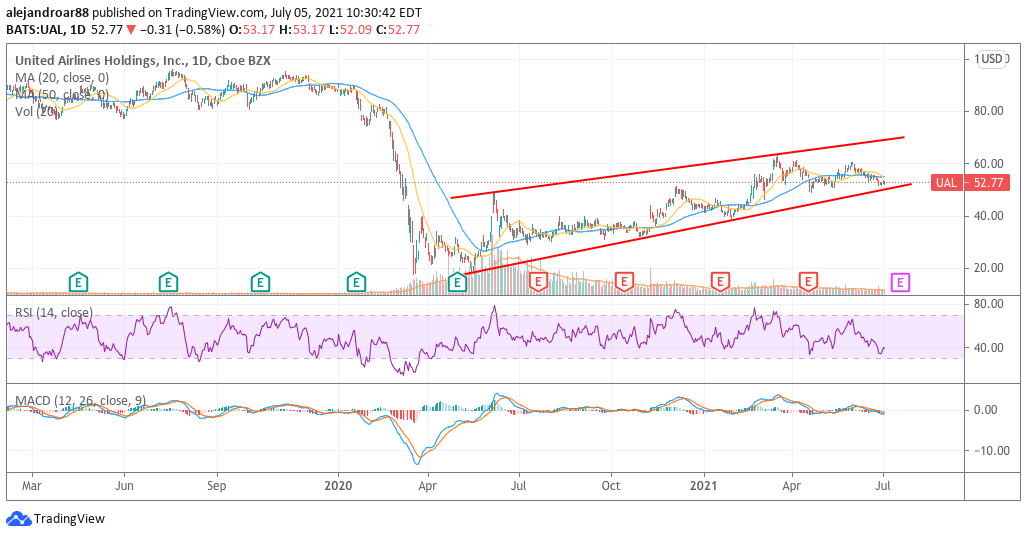

3. United Airlines (UAL)

From 2015 and forward United embarked on a path of decent revenue growth that led to the firm finally breaking the $40 billion threshold, with sales moving from $37.86 billion in 2015 to $43.26 billion by the end of 2019 at a 3.4% CAGR.

Even though this trend was disrupted by the pandemic, it would be plausible to see United resuming such growth under the leadership of Scott Kirby even though the path to profitability remains challenging as the firm reported losses of $1.36 billion during the first quarter of 2021.

For United, net margins had ranged between 5% and 7% before the pandemic stroked and analysts are expecting that sales should get back near to where they were before the virus crisis by the end of 2023.

For patient investors, that could result in net profits of around $2.2 billion by then on forecasted sales of $44 billion as per data from Koyfin. Meanwhile, the company held almost $13 billion in cash and equivalents by the end of the first quarter of 2021, which accounted for 76% of United’s market cap.

However, it would be plausible to expect that some of this cash will be burned. Therefore, if we take the market cap as is, regardless of how much cash the company has, that still results in a depressed forward P/E multiple of 8 times the company’s forecasted earnings for 2023. Patience might prove to be very rewarding for those who believe that United can make a comeback in the following 3 years.

67% of all retail investor accounts lose money when trading CFDs with this provider.

4. Ryanair Holdings (RYAAY)

Ryanair had been growing its revenues at a solid 9% CAGR from 2016 to 2020, with top-line results moving from $6.07 billion to $9.36 billion by the end of such period. However, its profit margins had been declining for a while amid strong competition in Europe, which led the firm to slash its prices to keep attracting demand.

This airline could emerge stronger once the pandemic is over and the valuation appears to reflect that as Ryanair’s market cap currently stands at $22 billion, which is more than 2 times the firm’s 2019 sales.

It appears that the firm’s ability to maintain its long-term debt in check regardless of the impact that the pandemic had on its operations has made Ryanair an attractive stock for value investors. In this regard, its financial commitments went up by only $1 billion during the crisis to land at $4.3 billion on assets of $14.4 billion including $3.6 billion in cash and equivalents.

67% of all retail investor accounts lose money when trading CFDs with this provider.

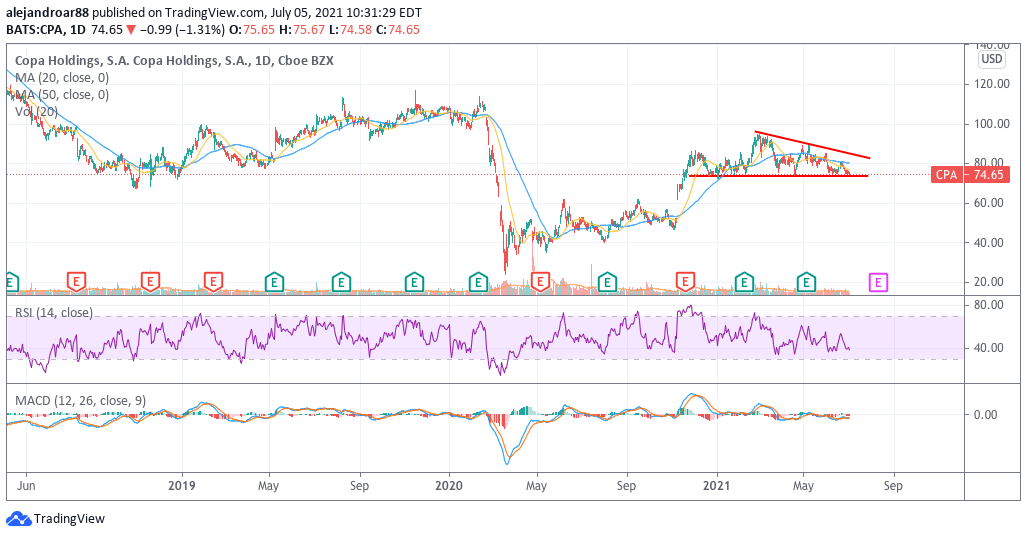

5. Copa Holdings SA (CPA)

Before the pandemic, the Panama-based Copa Airlines had been delivered solid gross profit and net profit margins while its revenues were growing at a decent pace, moving from $2.25 billion in 2015 to $2.71 billion by the end of 2019 at a 4.7% CAGR.

Meanwhile, the airline has managed to trim its losses to $110 million by the end of the first quarter of 2021 and it is fairly possible that it could swing to profits by the first quarter of next year.

Cash reserves currently sit at $1.1 billion and around $500 to $600 million could be drained in the following quarters. That would result in $500 million left that account for 15% of Copa’s current valuation.

Based on those estimates, if Copa manages to turn a profit in the following two to three years of around $100 and $200 million – in line with its historical performance – the current forward P/E ratio for this stock can be considered a fairly conservative one at 14.

Buy Stocks at eToro, the World’s #1 trading platform!