Seven Questions to Ask Before Refinancing Your Mortgage

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

3 June 2011.

House prices in the US are crashing again. With 18 million households across the country on the verge of defaulting on their mortgage, how will the fall in house prices affect your mortgage?

Related Article: US House Prices: Worse Now Than During Subprime Crash

3 June 2011.

House prices in the US are crashing again. With 18 million households across the country on the verge of defaulting on their mortgage, how will the fall in house prices affect your mortgage?

Related Article: US House Prices: Worse Now Than During Subprime Crash

Well if you own a house for $300,000 with a 90 percent mortgage and house prices fall, the percentage of the house that is covered by the mortgage will increase. However your mortgage repayments will only change if there is a change in interest.

And as lenders are threatened with over-valued mortgages, interest rates may be pushed up. Which means if you’ve maxed your borrowing (and repaying) power, a rise in interest rates and mortgage repayments could cripple you financially – and eventually be forced into foreclosure. But before you throw in the towel and head for foreclosure, consider refinancing your mortgage to save money on interest payments and pay off your home loan faster.

Table of Contents

1. How much are the costs of getting the loan?

When you apply for a loan, you’ll also get estimates on what your total costs for getting the loan are, including title insurance, appraisals, discounts and other costs. Your best bet is to compare estimates and budget 10 percent higher than the estimate to allow for hidden costs and fees and always do crop up.

2. Can I get homeowner insurance?

This is a particularly important question to ask if you live in a disaster-prone area. And thus your premiums may be higher. Homeowner insurance coverage should be top of your list along with finding the best loan.

Find out more about home insurance on EconomyWatch

3. Will I really save money by refinancing?

Most people assume that refinancing their mortgage will save them money. But is that really the case? If you end up relocating or selling your home for other reasons, refinancing becomes unprofitable in the long term. Since refinancing saves you money in the long term, you need to know if you’ll own the home for long enough to come out ahead.

4. Will I get a good rate?

That depends on your credit score. The current interest rates for a refinance quoted on major financial web sites can only give you a general idea of what interest rate you might be able to get. And if you don’t qualify for the best interest rates, is it still worth refinancing?

Related: How To Find The Best Refinance Mortgage Rates

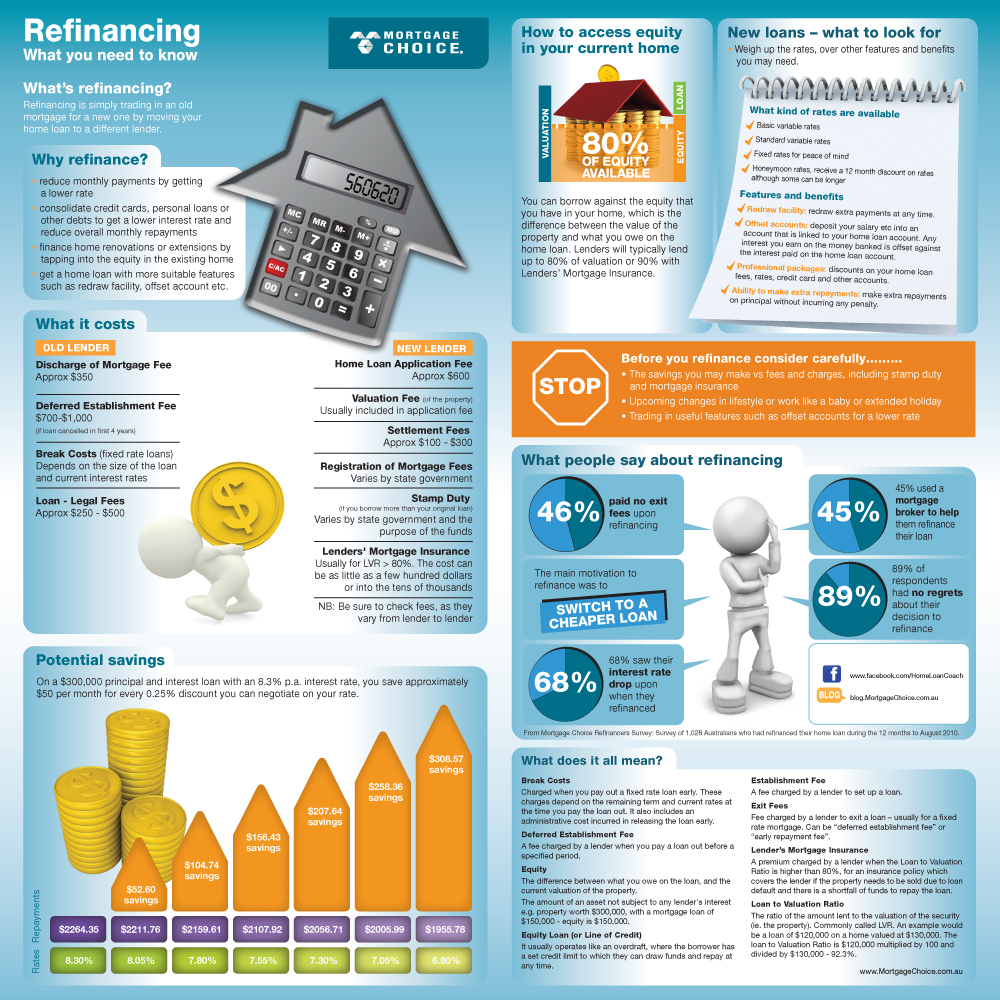

Source: Mortgage Choice

5. Will I be able to make the monthly repayments?

Principal and interest are only part of your monthly payment. Add in private mortgage insurance, association fees, property taxes and homeowner insurance and your range of affordable homes will narrow — to the ones you will actually be able to afford.

Experts often recommend that couples qualify for a mortgage based on one partner’s income. Especially in the current high unemployment environment, at least if one income is lost, you’re sheltered from disaster.

Related: How Much Will I Be Able to Borrow For A Mortgage?

6. Am I packaging other debt into my mortgage?

It might sound like a good idea to pay off some of your other debts by refinancing them into your mortgage. The interest rates are lower, so why not right?

The thing is, if you take a short term loan (like your car loan for example) and turn it into a long-term loan – even with lower interest, you’re likely to end up paying more.

7. Is the deal too good to be true?

Sometimes, a lender may quote one interest rate and set fees on the day you sign – which is totally different. The ‘ole bait and switch trick.

If you know you have a good loan, you may not want to roll the dice and see what you end up with when you refinance. And if you already have a bad loan, refinancing will be useless if you just end up in another bad loan.

Related: Should You Walk Away From Your Mortgage?

Refinancing can be a great way to save money, if you do it right. But a bad refinance can put you in a situation where the only person benefiting is the loan officer.

Find out more about Mortgages on EconomyWatch

Liz Zuliani

EconomyWatch.com