Nike Stock Turns Negative for 2023 After Guidance Cut

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Nike stock (NYSE: NKE) fell over 11% yesterday and turned negative for the year after the company reported its earnings for the fiscal second quarter of 2024 and slashed its full-year revenue guidance.

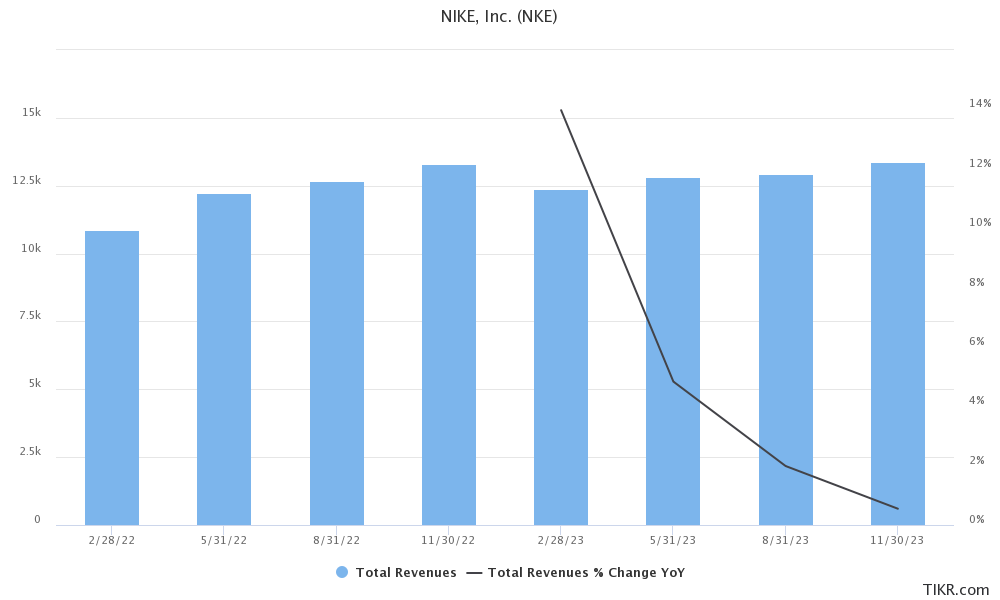

Nike reported revenues of $13.39 billion which were 1% lower YoY on constant currency terms and fell short of the $13.43 billion that analysts expected. This is the second consecutive quarter when the sneaker giant’s revenues trailed estimates making it only the first such instance since 2016.

Table of Contents

Nike stock crashed after Q2 earnings

However, while the shares still rose after the fiscal Q1 earnings release as Nike sounded upbeat on its China business and also maintained its full-year revenue and margin guidance, they fell after the Q2 earnings as the management gave a cautious commentary and also toned down its full-year revenue guidance.

Nike’s previous guidance called for a mid-single-digit revenue increase in the fiscal year but now it expects sales to rise only about 1% in the year.

Commenting on the guidance cut, Nike’s CFO Matthew Friend said during the earnings call, “Last quarter as I provided guidance, I highlighted a number of risks in our operating environment, including the effects of a stronger U.S. dollar on foreign currency translation, consumer demand over the holiday season and our second half wholesale order books. Looking forward, the impact of these risks is becoming clearer.”

Nike slashed revenue guidance

Nike now expects its revenues in the current quarter to be lower YoY which it blamed on tougher comps. It expects sales to rise in the low single digits in the final quarter of the year. Friend added, “This new outlook reflects increased macro headwinds, particularly in Greater China and EMEA adjusted digital growth plans based on recent digital traffic softness and higher marketplace promotions, life cycle management of key product franchises, and a stronger U.S. dollar that has negatively impacted second-half reported revenue versus 90 days ago.”

Meanwhile, even as Nike slashed its revenue guidance the company still expects gross margin improvement between 1.4%-1.6% in the year, after excluding restructuring charges.

Friend said, “As we look ahead to a softer second-half revenue outlook, we remain focused on strong gross margin execution and disciplined cost management.”

It also unveiled a $2 billion cost-cut program spread across three years which among others would lead to layoffs. The company expects a charge of between $400 million-$450 million related to the restructuring which it would book in the current quarter.

NKE to cut $2 billion in costs

Friend said, “In this competitive environment, we need to accelerate our pace of innovation, elevate our marketplace experiences, maximize the impact of our storytelling, and increase our speed and responsiveness.”

He added, “We know in an environment like this, when the consumer is under pressure and the promotional activity is higher, it’s newness and it’s innovation which causes the consumer to act.”

NKE sounds a warning on consumer demand

Nike also gave a warning on consumer demand with Friend saying, “We are seeing indications of more cautious consumer behavior around the world.” Notably, still-high inflation, multi-year high interest rates, and concerns over the health of the economy have taken a toll on consumer sentiments.

Also, like other industry players, Nike is also saddled with excess inventory which stood at $8 billion and while the metric fell 14% it is still above what the company would have wanted. Amid high supply chain inventories, Nike has to do promotional activities to clear the excess inventory.

Nike is however comfortable with its inventory position vis-à-vis competitors and Friend said, “When we look at the level of inventory in our partners relative to their current level of retail sales, we feel good about the weeks of supply that we have there. And what I would tell you, in the — in the large majority of our partners, we also are seeing the highest mix of current season inventory that we’ve seen in many many seasons.”

How did analysts react to NKE’s earnings?

After Nike’s earnings release, TD Cowen downgraded the stock from outperform to market perform and said, “Nike needs improved marketing outside of basketball, streetwear and lifestyle trends. Innovation at the higher end of its assortment is not resonating at scale while the Nike faces disruption from smaller competitors in footwear and apparel.”

Goldman Sachs however maintained its buy rating on NKE stock and said in its note, “On the other hand, we believe today’s update provided ample fodder for bears, with slowing growth momentum as a result of a tougher macro pointing to a more promotional competitive marketplace, and the company now speaking more comprehensively to key franchise life cycle management which will weigh on sales momentum going forward.”

Meanwhile, after the crash yesterday, Nike stock turned negative for the year and is underperforming the markets by a wide margin. The stock peaked in late 2021 and has since fallen as the company’s sales growth has been tepid across key markets.