Nike Stock Spikes on Fiscal Q1 Earnings Beat: Key Takeaways

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Nike stock (NYSE: NKE) is trading higher in US premarket price action today after reporting its fiscal Q1 2024 earnings. While the sneaker giant missed consensus revenue estimates for the first time in two years – it was more than offset with better-than-expected margins and profits.

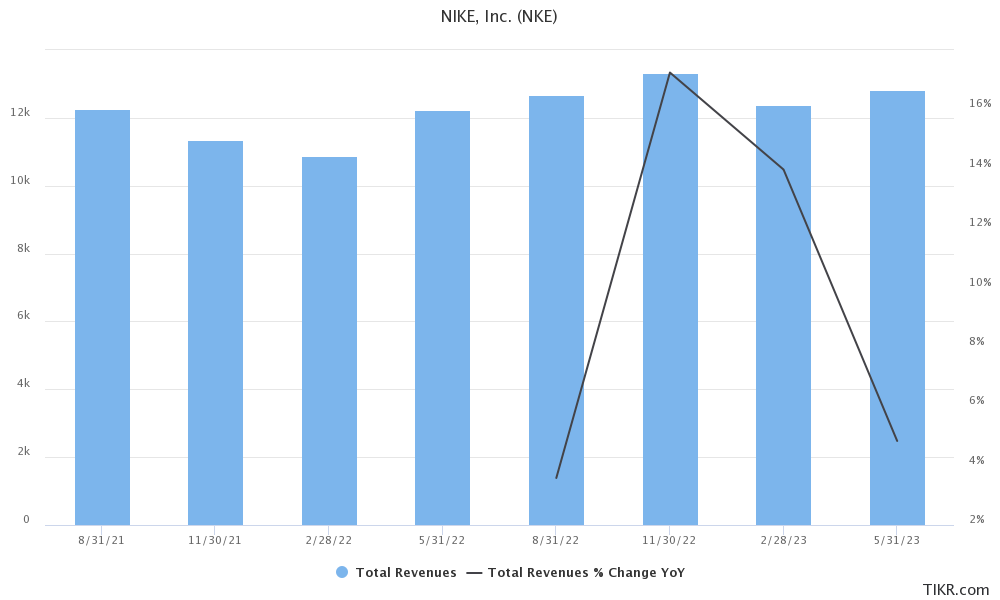

Nike reported sales of $12.94 billion in the fiscal first quarter that ended on August 31. The metric rose only 2% YoY and was slightly below the $12.98 billion that analysts expected.

In line with the company’s strategy of focusing on the direct channel as compared to wholesale, Nike Direct sales rose 6% YoY to $5.4 billion while Wholesale channel sales were flat over the period.

Commenting on the Direct channel, Nike’s CFO Mathew Friend said, “We continue to see that consumers want to connect directly and personally with our brands and in fact, member engagement within our direct business is up double digits versus the prior year with increasing average order values.”

Nike missed consensus revenue estimates in Q1

Looking at the geographical breakdown, Nike’s sales in Greater China rose 12% YoY – the second consecutive quarter of double-digit sales. The sales however increased only 5% in currency-neutral terms and the metric came in at $1.73 billion which was below the $1.8 billion that analysts expected.

The company’s sales in North America fell 2% while it rose 8% in the EMEA (Europe, Middle East, and Africa) region. Its sales in Latin America and Asia Pacific also rose 2% YoY.

Meanwhile, Nike’s CEO John Donahoe sounded optimistic about China and said during the earnings call and said that Nike “feels good” about the Chinese market and its position in the country – emphasizing that the company increased its market share there.

Donahoe added, “Frankly, a couple things stand out. One, sport is back in China, you can just feel it, and that gives us great confidence about the future and the Chinese consumer in our segment, regardless of the macroeconomic outlook there.”

Speaking further about the market, Donahoe said, “Greater China sets the execution standard for us, and our goal is to scale their success across all of our geographies, every sport and every dimension of our business. And that’s how we win over the long term.”

Analysts on NKE stock

According to Forrester Research analyst Sucharita Kodali, “The China story is probably the biggest one here for Nike.” She added, “The challenge is that Nike has been very dependent on the Asian market, certainly on the Chinese consumer. Not only do you have issues with the softening of the Chinese consumer and their spending ability but also just a lot of geopolitical risk that is there.”

Notably, Nike is among the companies who are at risk from growing US-China tensions and Donahoe has traveled to the country twice this year in a sign of its importance for Nike.

Nike posted better-than-expected earnings

While Nike’s gross margin fell slightly to 44.2% in the quarter it was nonetheless better than the 43.7% which analysts expected. The company’s EPS of 94 cents was also higher than the 75 cents that analysts had forecast. Markets gave a thumbs up to the earnings and margin beat even as the company posted its first revenue miss in two years.

NKE maintained its guidance

The company maintained its fiscal year 2024 guidance and still expects revenues to rise mid-single digits in the year and a gross margin expansion of between 1.4% and 1.6%. Friend stressed, “We’re closely monitoring the operating environment, including foreign currency exchange rates, consumer demand over the holiday season, and our second half wholesale order book.”

In the fiscal second quarter, it expects revenues to rise only slightly as compared to the last year due to the high base year effect.

Friend was upbeat on the earnings outlook and said, “we are focused on improving our marginal cost of growth, with more modest increases in operating overhead this fiscal year following two consecutive years of double-digit growth in this area. We are doing this by unlocking speed and productivity as we transform our operating model to build a faster, more efficient Nike.”

Nike is also optimistic about its long-term financial projections of hitting high teen EBIT margins. While Friend said that the target is “achievable” he emphasized that it’s difficult to predict the timeline given the uncertain macro environment.

Nike’s inventory levels come down

One of the headwinds for Nike was the massive surge in inventories. However, the company noted that its inventories in dollar terms were 10% lower YoY at the end of Q1. Friend emphasized, “We continue to feel very good about our position. NIKE inventory dollars are down 10% versus the prior year. Our total inventory units across the marketplace, including NIKE and our wholesale partners, are down double digits versus the prior year.”

He added, “Partner-owned inventory units are in line with the previous year, with levels planned to remain lean through our second quarter, a meaningful accomplishment after higher levels of wholesale sell-in during fiscal ’23. On the whole, we are very comfortable with the level of inventory in the marketplace in relation to the retail sales that we’re seeing as we begin increasing levels of wholesale sell-in in our second half.”

Nike posted negative free cash flows

Nike has a strong balance sheet. It had cash and cash equivalents of $8.8 billion at the end of August which was $3.1 billion lower than the corresponding quarter last year. While it generated positive operating cash flows, they were more than offset by higher capex and an almost $1.7 billion shareholder payout which includes $1.1 billion in share repurchases.

Nike stock is up almost 8% in US premarket price action today which is a welcome break for investors as the stock has looked weak in 2023. The shares hit their all-time highs in 2021 and have since fallen sharply. Nike hasn’t participated in the market rally in 2023 either and has lost almost a quarter of its market cap based on yesterday’s closing prices.