Zoom Stock Down 45% in 2021 – Time to Buy ZM Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Zoom stock collapsed last year amid a confluence of negative catalysts that ended up pushing the valuation of the company to its lowest level since June 2020 – back when the pandemic was starting to act as a tailwind for the video conferencing developer.

Tough competition from companies including Microsoft (MSFT), whose Team app directly competes with Zoom’s software, fears about an upcoming interest rate hike, and a fading pandemic tailwind are among the factors that weighed on the performance of Zoom stock in 2021.

Meanwhile, the termination of a proposed merger with Five9 also contributed to this decline as the transaction could have helped Zoom in diversifying its revenue stream.

“While we were excited about the benefits this transaction would bring to both Zoom and Five9 stakeholders, including the long-term potential for both sets of shareholders, financial discipline is foundational to our strategy”, stated Eric S. Yuan back in September in regards to why the deal was canceled.

Moreover, in late December, US Treasury yields started to climb and that pushed the valuation of risky assets including growth stocks lower. In this regard, 10-year Treasury yields have climbed from a 3-month low of 1.357% seen in the first few days of last month to 1.647% just yesterday.

What could be expected from this tech tock in 2022 and forward? In this article, I’ll be assessing the price action and fundamentals of Zoom stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

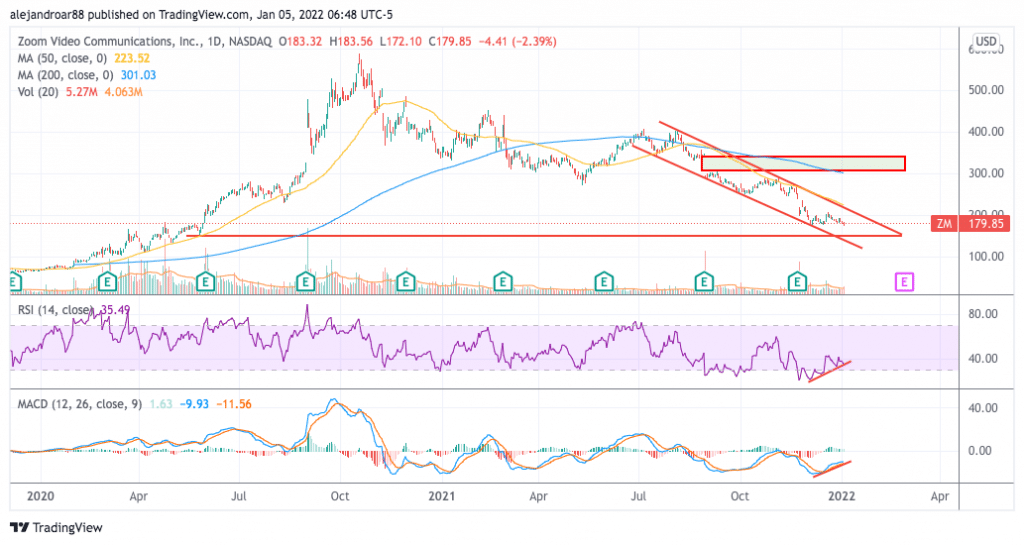

Zoom Stock – Technical Analysis

Zoom stock has been on a sharp downtrend during the second semester of 2021 as the tailwind provided by the pandemic that once lifted the performance of its business seems to be clearly fading on the back en-masse vaccinations and a recently approved antiviral treatment.

Even though Zoom has managed to live up to the market’s expectations in terms of revenues and earnings, market participants appear to agree that the company will eventually succumb to the tough comparables of both 2020 and early 2021. This means that it will eventually report negative revenue and earnings growth rates.

The termination of the Five9 deal favored this bearish outlook as it may have provided an item that would have lifted the financial performance of the company in the future amid the addition of the target company’s results to its consolidated financial statements.

That said, even though the trend is still heading downwards, both the Relative Strength Index (RSI) and the MACD are displaying a moderate bullish divergence as the two indicators are heading higher despite the price remaining relatively range-bound.

The outlook at the moment is neutral-to-bullish amid the appearance of these divergences. However, if the price breaks below the next relevant horizontal support area found at the $152.5 level, chances are that the downtrend will accelerate.

On the other hand, a break of the descending triangle formation shown in the chart could lead to a short-term rebound if bulls manage to push the price above the 50-day simple moving average – which currently stands at $223.5 per share.

Zoom Stock – Fundamental Analysis

Even though Zoom is still being expected to grow its top-line results in the following years, the rate at which its revenues will expand will be much slower compared to the past.

In this regard, estimates are pointing to a 50% jump in Zoom’s revenues in 2022 followed by a 16% increase in 2023. In previous years, Zoom managed to report year-on-year revenue growth rates of 80% or higher.

Meanwhile, the firm’s adjusted earnings per share are expected to stay flat at around $4 and $5 per share in the next two years.

In the past 12 months, the company produced approximately $1.6 billion in free cash flows resulting in an FCF margin of around 41%. In 2022, based on the market’s consensus estimate of $4.9 billion for the firm’s revenues, Zoom could generate at least $2 billion in free cash flows.

At its current market capitalization of $53.6 billion, the firm is trading at 27 times that forecasted cash flow figure. Even though this is a conservative multiple for a company in the tech sector, Zoom’s expected struggles to deliver positive top and bottom-line growth in the following years justify the current valuation to some extent.

Unless the firm manages to convince Wall Street that it can keep growing its business in the future – either organically or via some strategic acquisition – chances are that the valuation will remain depressed for what remains of the year.

Buy ZM Stock at eToro with 0% Commission Now!