United Airlines Stock Price Down 16% in July – Time to Buy UAL Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of United Airlines stock is down 16% so far in July while it took a strong 5.5% hit just yesterday amid the broad-market sell-off that took place due to concerns about the impact that the Delta variant of the coronavirus could have on the recovery of the global economy.

The company will be reporting its financial results covering the second quarter of 2021 after the market closes today and it is fairly possible that United will surprise the market as passenger volumes have been recovering during the summer season to around 60% to 80% of where they were during the same period in 2019.

Could this be an opportunity to buy this airline stock at a point when the market is being overly pessimistic about its future? Or is this wave of negative momentum justified based on the severity of the threat posed by this more transmissible and deadly variant of the COVID-19 virus?

In the following article, I take a look at the stock’s price action and fundamentals to possibly answer those questions.

67% of all retail investor accounts lose money when trading CFDs with this provider.

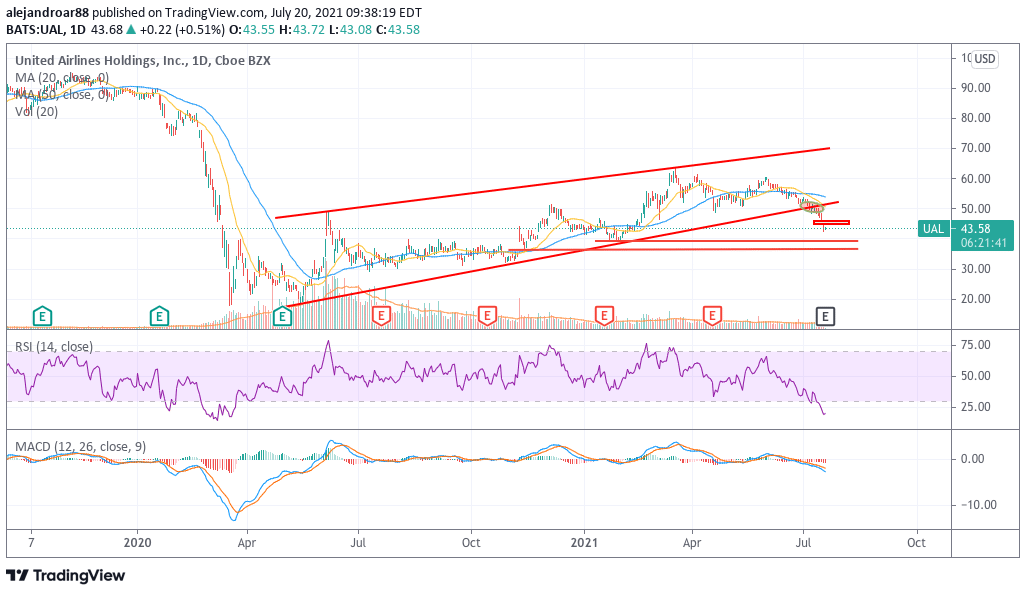

United Airlines Stock – Technical Analysis

Even though United Airlines shares have been recovering progressively from their March lows, the stock remains well below its pre-pandemic levels even before this latest crash happened.

Meanwhile, UAL has entered a bear market already as it is trading 28% below its early June high of $60 per share while it has opened today’s stock trading session in the red zone, this being the sixth consecutive losing day for UAL if it ends the day in negative territory.

Moreover, a break of the long-dated trend line shown in the chart emphasizes the graveness of the bearish momentum the stock is seeing, with readings of the Relative Strength Index (RSI) plunging to their lowest levels since the pandemic crash.

It seems that market participants are more worried than it seems about a potentially prolonged downturn for airlines on the back of a persistent virus threat despite en-masse vaccinations.

These overly bearish readings point to the potential continuation of the current weakness and it would be plausible to expect that UAL stock could dive to lower areas of support – possibly eyeing the $39 and $36.5 levels as landing zones if the current downturn continues for a few more days. That results in a fairly dangerous downside risk of 16%.

United Airlines Stock – Fundamental Analysis

United’s quarterly results have been recovering slowly from the depths of the first two quarters of 2020, back when the firm reported as little as $1.5 billion revenues compared to the usual $9 to $11 billion level.

During the previous quarter, the firm saw its sales dip to $3.2 billion compared to $3.4 billion it brought in during the fourth quarter of 2020 while net losses landed at $1.36 billion or $4.29 per share, which was an improvement compared to the previous quarter.

With passenger volumes recovering to around 60% to 80% of pre-pandemic levels during the second quarter as indicated by TSA screenings, analysts are expecting to see sales surging to around $5.33 billion as per estimates compiled by Koyfin, resulting in around 45% of what the firm brought in during the same period in 2019.

Meanwhile, GAAP losses per share for the period are expected to land at around $4 per share, which would result in a net loss of approximately $1.2 billion. These estimates point to United still burning a significant amount of cash.

For reference, United indicated that it burned an average of $9 million per day back in the first quarter. If that number declines by around 25% on the back of higher sales, that would still result in approximately $600 million burned during the second quarter of the year.

By the end of that period, United had over $13 billion in cash and equivalents, which is more than enough to sustain the current downturn based on that quarterly cash burn. Meanwhile, when the virus situation is fully out of the picture, this excess liquidity can be used to pay a portion of the company’s long-term debt, which is standing at around $30 billion.

However, for now, analysts are not expecting to see United’s sales recovering to pre-pandemic levels until 2023 at least, primarily due to the sustained impact that the virus crisis is having in Latin American countries – a key market for the airline.

Meanwhile, at $44 per share, UAL stock is being valued at 14 times its forecasted EPS for 2022 ($3.15) while the company’s net tangible value per share stood at minus $6.7 per share due to the weight that intangible assets have on the firm’s balance sheet.

At the moment, the short-term outlook for United remains bearish based on the combination of overly bearish momentum and weak fundamentals. Meanwhile, the threat of the Delta variant could prolong the extent of the sales decline for United, which could contribute to keeping the stock price at its currently depressed levels for longer.

Buy Stocks at Vindax FX, the World’s #1 trading platform!