Uber Stock Price Down 22% in 2022 – Time to Buy UBER Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

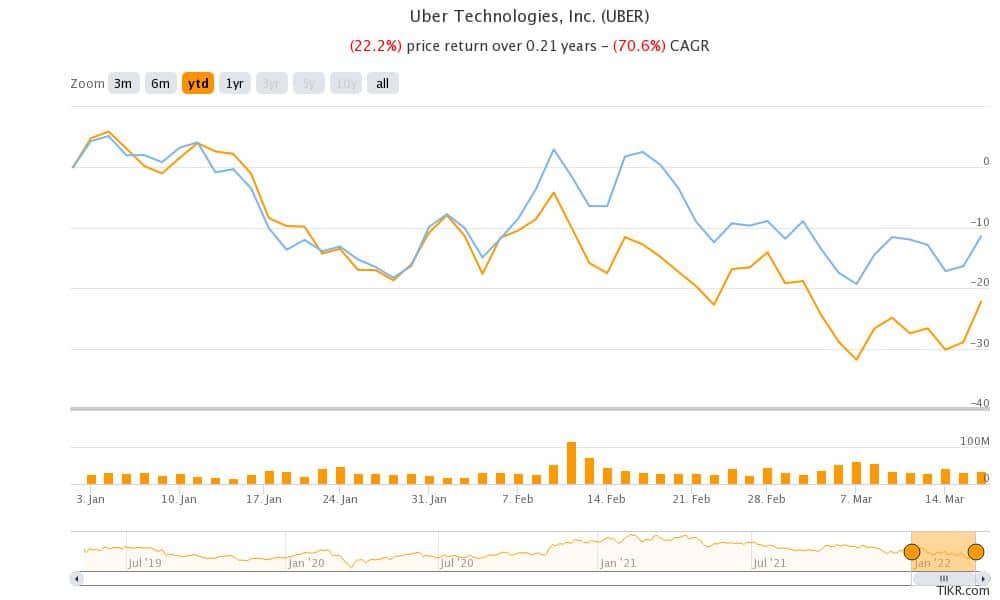

Uber stock (UBER) soared over 9% yesterday. However, it is still down 22% for the year and is underperforming the S&P 500. Rival Lyft is outperforming UBER stock in 2022 and is down about 11.4% for the year.

What’s the forecast for Uber stock and should buy the ride-hailing and food delivery company now?

Uber stock recent developments

Ride-hailing companies have been grappling with the steep rise in gasoline prices. While crude oil prices have come off their 2022 highs they are still up sharply over the last year. Both Uber and Lyft have added a fuel surcharge to compensate drivers for the higher gas prices.

In its release, Uber said, “Beginning Wednesday, March 16, consumers will pay a surcharge of either $0.45 or $0.55 on each Uber trip and either $0.35 or $0.45 on each Uber Eats order, depending on their location—with 100% of that money going directly to workers’ pockets.” It added, “The surcharges are based off the average trip distance and the increase in gas prices in each state. This is temporary for at least the next 60 days, when we’ll reassess.”

The company has justified the price rise citing the increase in inflation. It said, “We know that prices have been going up across the economy, so we’ve done our best to help drivers and couriers without placing too much additional burden on consumers.”

68% of all retail investor accounts lose money when trading CFDs with this provider.

Fed rate hikes

To be sure, rising inflation is not a concern only for ride-hailing companies, but central banks across the world face the tough choice of balancing rising inflation while supporting economic growth. US Federal Reserve has announced a 25-basis rate hike, the first since 2018. The US central bank expects as many as six rate hikes in 2022 as it tries to tame inflation which is almost four times what it targets.

Uber earnings

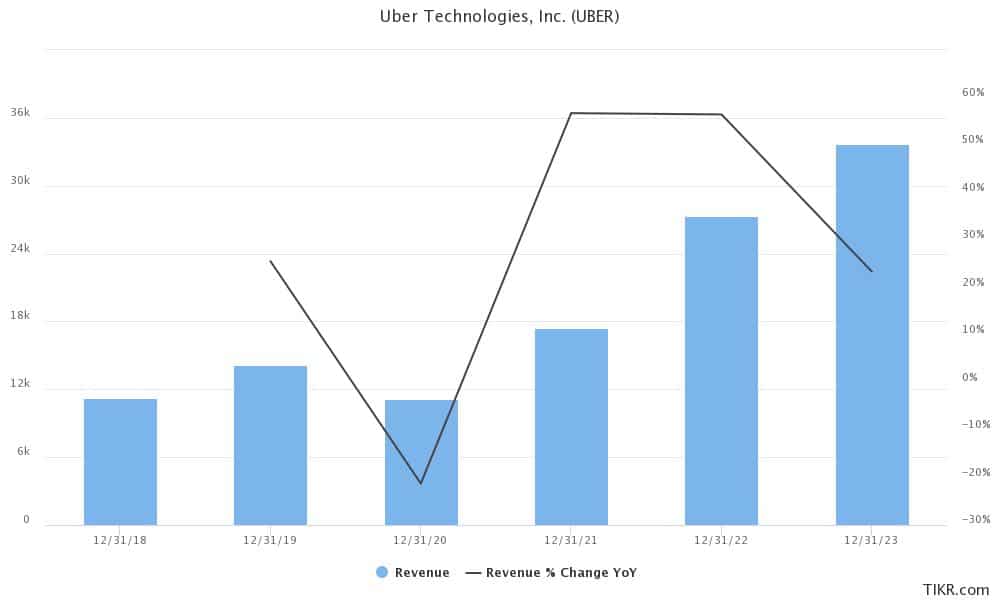

Uber reported revenues of $5.78 billion in the fourth quarter of 2021, which was ahead of the $5.34 billion that analysts were expecting. The company also posted its first profitable quarter and reported a net income of $892 million in the quarter. However, the profits came on the back of a $1.4 billion pre-tax income from equity investments. While it recorded unrealized gains on its investment in Grab and Aurora, it was somewhat offset by unrealized losses on the company’s investment in Didi. Uber is among the biggest stockholders of Didi whose stock has plunged after the company announced a delisting from the US exchanges.

That said, in the current quarter, the company might need to book massive losses on both Didi and Grab. Grab stock has also plummeted after the listing and falls in the penny stock category, falling fallen over 65% from the SPAC IPO price of $10.

Guidance

Uber also provided the guidance for the first quarter and said that it expects gross bookings to be between $25-$26 billion. It expects to post adjusted EBITDA of $100-$130 million in the quarter. The company’s guidance implies a sequential increase in both gross bookings and EBITDA.

Uber stock forecast

Of the 43 analysts covering Uber stock, 39 have a buy rating while three have a hold rating. One analyst has a sell rating. Its median target price of $60 is a premium of 84% while the street low target price of $80 is a premium of 145%. While Wall Street analysts have lowered their target price, they continue to remain bullish on the company.

Yesterday, Needham reiterated its buy rating on the stock citing its survey checks that point to a strong demand. “In our latest Mobility Tracker, pricing and wait times have trended upward back toward our pre-Labor Day sample levels. We view this as a positive for both UBER and LYFT, as we believe these increases are demand-driven and as various consumer data sets are showing a rebound back to pre-omicron levels of activity,” said Needham in its note.

Earlier this month, UBS also reiterated both Uber and Lyft as buys as it sees better demand trends for both the companies.

Long term forecast

Uber has a diversified business model divided between the food delivery and ride-hailing business. The company is now trying to balance growth with profitability. In the prepared remarks during the Q4 2021 earnings call, its CFO Nelson Chai said. “Moving forward, we are poised to continue to grow at scale while expanding profitability.” As part of its efforts to work on profitability, the company has exited several loss-making markets. It sold the autonomous driving business to Aurora and the flying taxi business to Joby Aviation.

At its analyst day last month, the company said that it expects to post an operating profit of $5 billion by 2024. While it was below the $5.7 billion that analysts were expecting, the company’s CEO Dara Khosrowshahi said, “We think it’s a worthwhile target. Could there be upside? Absolutely, but let’s work on that target for now.”

The company expects gross bookings between $165-$175 billion by 2024, which was in line with analysts’ estimates.

Should you buy Uber stock?

Uber trades at an NTM (next-12 months) EV-to-sales multiple of just about 2.2x. As the company works towards achieving sustainable profitability while maintaining a reasonable level of growth, it should see a rerating.

The major risk for Uber and other ride-hailing companies is the growing clamor for classifying gig economy workers as employees. However, that’s more of an industry-wide problem than something particular to Uber. Overall, at these prices, Uber looks like a good stock to buy for the long term.

Buy UBER Stock at eToro from just $50 Now!