PSFE Stock Price Falls 14% – Time to Buy Paysafe Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Paysafe (PSFE) stock was trading almost 14% lower in early price action today and hit a new 52-week low. Why’s PSFE stock falling and should you buy the dip?

Paysafe went public in March through a reverse merger with one of Bill Foley’s SPAC who has been a Wall Street veteran and has been associated with several big financial institutions. Meanwhile, the stock has had a rough ride as a publicly-traded company. While there was a brief surge following the interest from traders on Reddit group WallStreetBets, PSFE stock has failed to hold on to higher price levels.

Paysafe releases quarterly earnings

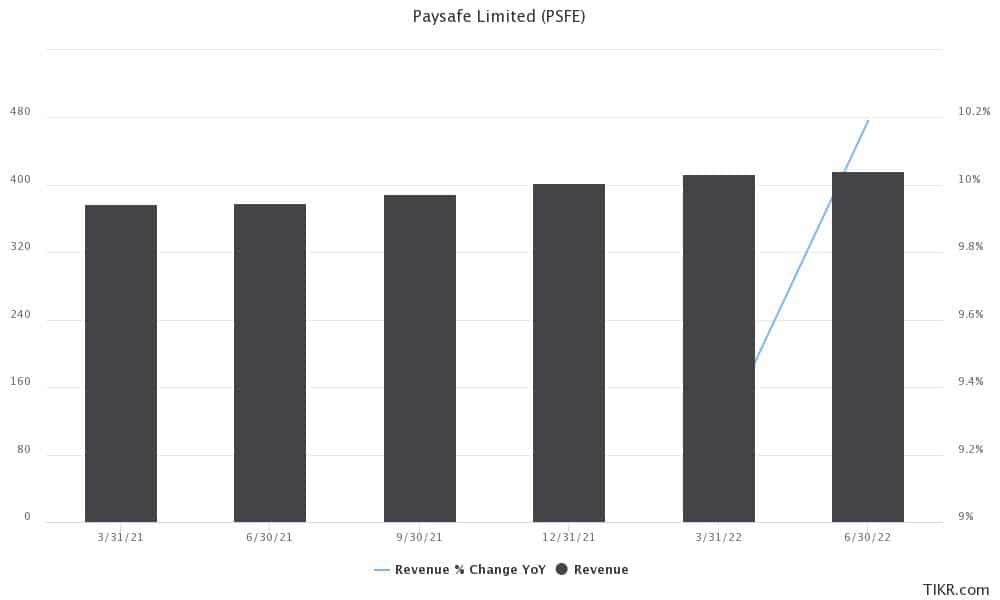

Paysafe released its second-quarter earnings today. This is the company’s second earnings release as a publicly-traded company. However, just like the first-quarter results, where the stock had tumbled after the earnings release, it is falling sharply after the second-quarter release also.

PSFE reported total payment volumes of $32.3 billion in the quarter which were 41% higher than the corresponding period in 2020. Notably, Paysafe processes over $100 billion in payment volumes annually. The company reported revenues of $384.3 million in the quarter which were 13% higher than the second quarter of 2020. PSFE’s adjusted EBITDA increased 8% YoY to $118.8 million. The company also turned profitable on the net profit level and posted a net profit of $6.6 million in the quarter as compared to a loss of $15.9 million in the corresponding quarter in 2020.

“We are pleased with the continued momentum Paysafe exhibited over the second quarter with impressive growth and several key wins across iGaming and other attractive digital commerce verticals, including crypto,” said Paysafe CEO Philip McHugh.

67% of all retail investor accounts lose money when trading CFDs with this provider

PSFE maintains guidance

Paysafe maintained its 2021 revenue guidance of $1.53-$1.55 billion for the full year 2021 while it expects to post an adjusted EBITDA of $480-$495 million during the year. For the third quarter, it gave revenue guidance of $360-$375 million and an adjusted EBITDA guidance of $95-$110 million.

PSFE announced acquisition

PSFE’s free cash flows fell to $54.6 million in the quarter as compared to $96.2 million in the second quarter of 2020. While announcing the SPAC merger, Paysafe had touted its asset-light business model and high EBITDA margins. The company has been making acquisitions to spur growth. Today only, it announced the acquisition of SafetyPay for $441 million. Founded in 2007, SafetyPay enables e-commerce transactions and is primarily present in Latin America. Earlier this month only, PSFE had announced the acquisition of PagoEfectivo which gave it a foothold in Latin America.

McHugh sounded optimistic on SafetyPay transaction and said that “by combining the capabilities and open banking network of both SafetyPay and PagoEfectivo with our existing solutions in processing, digital wallets and eCash, along with our deep expertise in specialized verticals such as iGaming, travel and digital goods, we can become the true market leader in the region and provide merchants with unique and powerful combinations to grow their business.”

Paysafe stock forecast

Wall Street analysts are very bullish on PSFE stock and all nine analysts polled by MarketBeat rate it as a buy or some equivalent. Its average target price of $16.78 is a premium of 91% over current prices. Earlier this month, Bank of America initiated coverage on Paysafe stock with a buy rating and a $15 target price.

PSFE stock looks well placed in the payments industry. The company is also expanding geographically and is also launching new products.

PSFE stock long term forecast

The long-term forecast for Paysafe stock looks positive. The company has a market-leading position in the US iGaming market. As more states legalize sports betting it would bode well for PSFE’s long-term forecast. The fintech industry has a positive outlook over the long term and companies like Paysafe look well placed to capitalize on the opportunity.

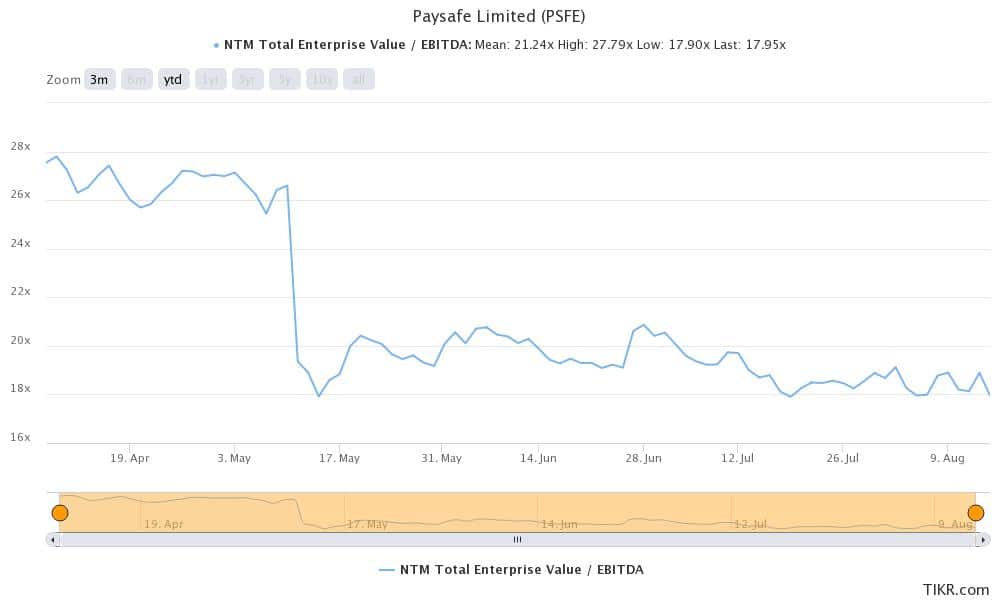

PSFE stock trades at an NTM (next-12 months) EV-to-EBITDA multiple of only about 18x which looks attractive. The valuation multiples are way below what other fintech names trade at. While Paysafe’s topline growth is also below that of other fintech names like SoFi and Square, the current valuations look attractive. These are the lowest valuation multiples for Paysafe as a publicly-traded company.

Paysafe stock technical analysis

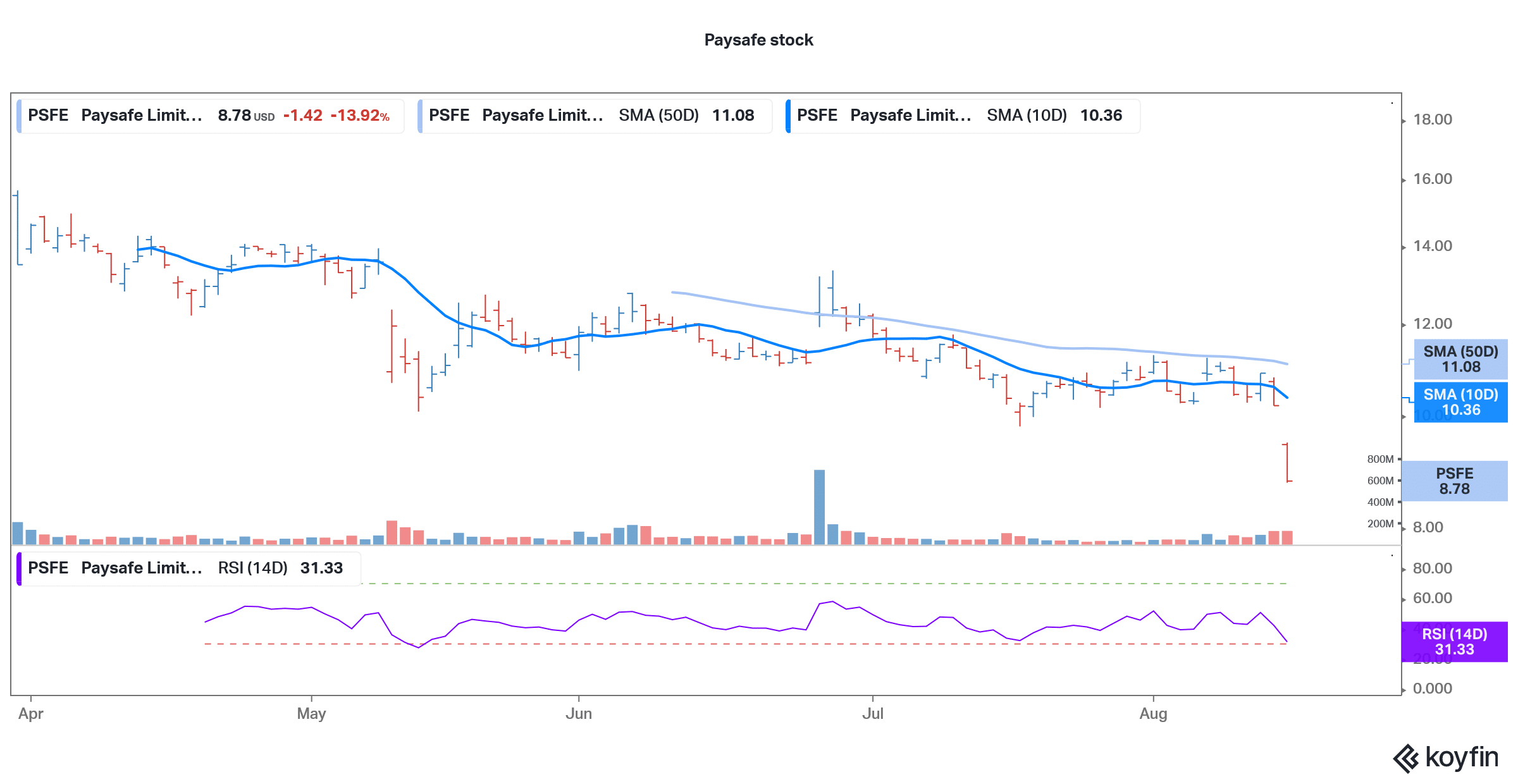

PSFE is looking weak on the charts after having fallen to a new 52-week low. The stock now trades below all the key moving averages. However, it has a 14-day RSI (relative strength index) of 31 which indicates that it is now getting near the oversold territory. RSI values below 30 signal oversold positions.

Overall, if you are looking at a reasonably valued fintech name with a positive long-term outlook, the recent crash in PSFE stock looks like a good buying opportunity. The company has a strong management team also and Foley also brings with him decades of experience in the financial services industry.

67% of all retail investor accounts lose money when trading CFDs with this provider