Peloton Stock Price Forecast November 2021 – Time to Buy PTON Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

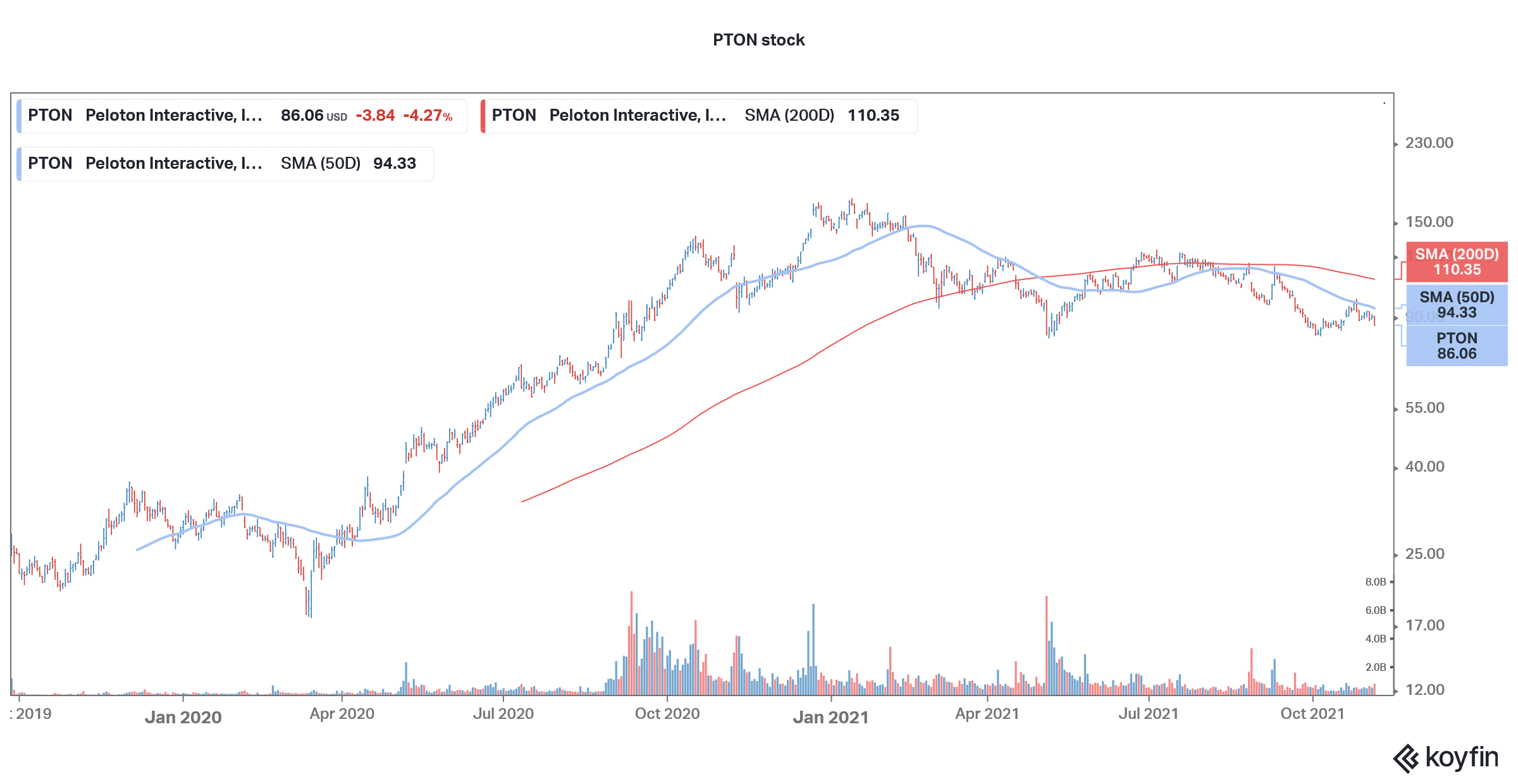

Peloton (PTON), whose stock price soared last year as sales boomed during the pandemic, has looked weak in 2021. The stock is down over 43% in 2021 and trades near its 52-week lows.

PTON’s dismal run looks far from over and it is down over 30% in US premarket price action today. What’s the forecast for Peloton stock and should you buy the dip in the home fitness company?

Stay-at-home stocks have looked weak

Peloton was among the so-called “stay-at-home” stocks that benefited from the changed consumer behavior. As gyms were closed, many people pivoted towards home fitness equipment which helped propel Peloton’s sales as well as shares higher. However, as is the case with other pandemic winners including Teladoc and Zoom Video Communication, the sales growth has come down significantly. Even the mighty Amazon hasn’t been able to skip the slump and has missed topline estimates for two straight quarters. The company’s fourth-quarter guidance was also bleak and another reminder that the high growth rates of 2020 are not sustainable.

68% of all retail investor accounts lose money when trading CFDs with this provider

Peloton earnings

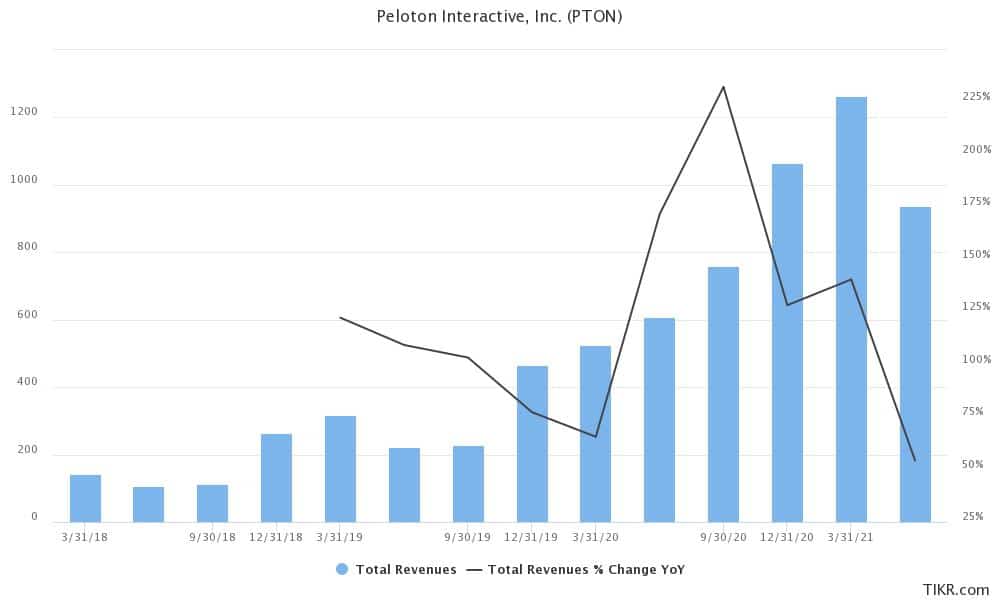

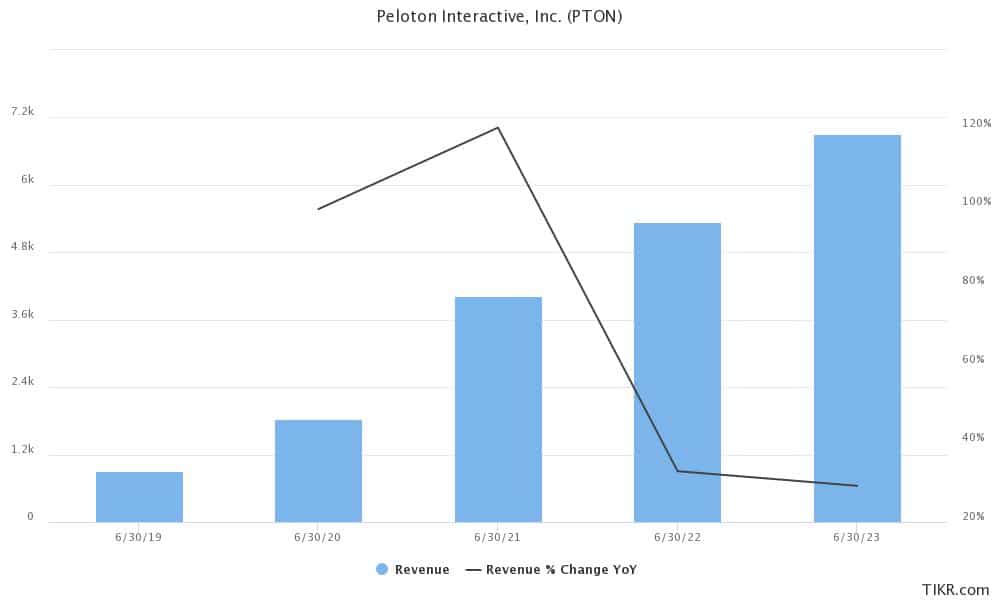

Peloton reported revenues of $805.2 million in the fiscal first quarter of 2022 that ended in September. The revenues increased only about 6% year-over-year and were below the $810.7 million that analysts polled by Refinitiv were expecting. This is the slowest revenue growth for the home fitness company since it went public in 2019.

While PTON’s topline missed estimates, its losses were also wider than expected. The company’s adjusted loss per share was $1.25 in the quarter which was ahead of the $1.07 per share loss that analysts were expecting.

While Peloton’s Subscription revenues increased 94% to $304.1 million in the quarter, it was more than offset by the 17% fall in sales of fitness products. Meanwhile, the company’s connected fitness subscribers increased 87% to 2.49 million at the end of the quarter. However, on the flip side, these subscribers completed 16.6 workouts every month which was below the 20.7 million workouts in the corresponding period last year.

PTON lowered guidance

If the earnings miss wasn’t enough, Peloton also lowered its guidance for the year. The company now expects to post revenues between $4.4-$4.8 billion in the full fiscal year with a gross margin of 32%. It expects to have between 3.35-3.45 million connected subscribers by the end of the year. It, however, expects to post an EBITDA loss between $425-$475 million in the year.

During the previous earnings call, PTON had guided for revenue of $5.4 billion in the fiscal year. At the midpoint of the guidance, the company has dialed back its revenue forecast by $800 million. At the same time, it has increased the projected EBITDA loss by $125 million.

Here it is worth noting that Peloton has had to increase its sales and marketing budget amid the negative publicity from the recall. In the fiscal first quarter, its sales and marketing expense rose 148% from the previous year and represented 35% of the sales. The company has also lowered the prices for its original bike. Incidentally, the company lowered the price at a time when companies have had to increase prices amid higher input costs.

Peloton stock price forecast

Before the earnings release, analysts were quite bullish on Peloton stock. It had a buy rating from 22 of the 31 analysts while seven analysts rated it as a hold. The remaining two analysts had a sell rating. Its median target price of $130 is a premium of 51% over yesterday’s closing prices.

However, after the massive guidance cut, we could see more analysts downgrade the stock. Wedbush Securities analyst James Hardiman, who is bearish on the stock, has labeled the earnings as “pretty ugly.”

PTON stock long term forecast

Peloton tried to portray a rosy long-term forecast during the earnings release. It said, “While we are reducing our near-term forecast, our confidence in and commitment to our strategy is unchanged. Software and streaming media have redefined at-home fitness and are driving a migration of workouts into the home, a consumer behavioral shift that we believe is still in its early stages.”

To be sure, there is still a lot of potential for home fitness companies as many people would stick with home gyms even after the pandemic. While the sales growth of last year wasn’t sustainable, the industry should still witness decent growth in the long term.

Sounding optimistic on the long-term growth potential, PTON said “We remain convinced that the growth opportunity for Peloton is substantial and this informs our decision to prioritize accessibility and household acquisition over near-term profitability, particularly as our industry-leading net promoter scores (“NPS”) and retention rates support a very strong consumer LTV (lifetime value) and unit economics”

Should you buy Peloton stock?

Looking at the premarket slump, Peloton’s market cap could fall as low as $18 billion. The company’s midpoint revenue guidance for the year is $4.6 billion which gives us a forward price-to-sales multiple of 3.9x. The valuations don’t seem high considering the positive long-term trajectory for the company.

Meanwhile, Peloton stock wasn’t looking good on the charts previously also and looks set to look even bearish now. The stock has been facing stiff resistance at the 50-day SMA (simple moving average). After the fall today, it would fall below all key moving averages.

However, if you are looking to take a long-term horizon, you can consider PTON stock at this price. Short-term noise withstanding, Peloton looks like a good stock for the long-term.

Buy PTON Stock at eToro from just $50 Now!