Peloton Stock Price Down 75% in 2021 – Time to Buy PTON Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

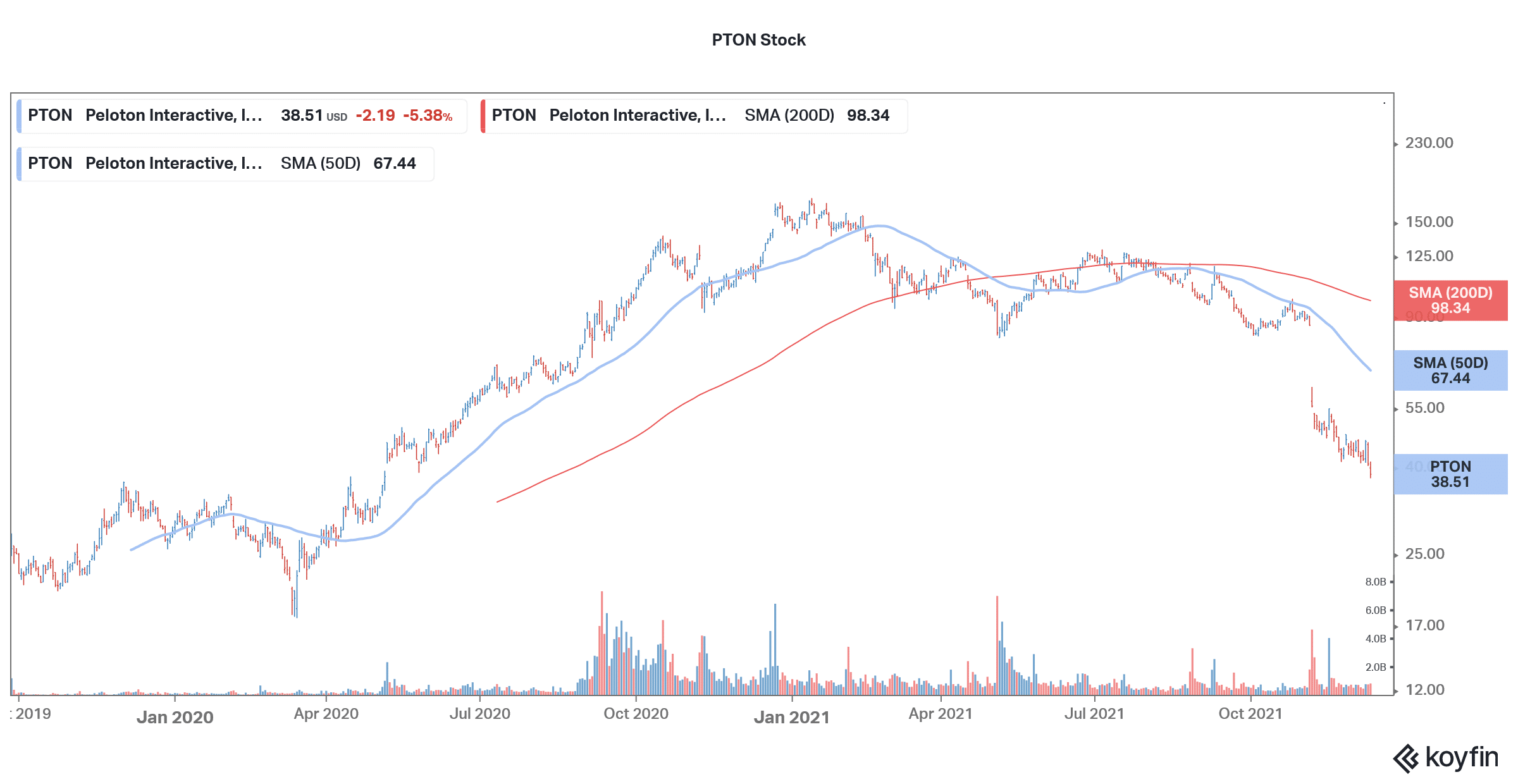

Peloton (PTON) stock fell 5.4% on Friday and hit a new 52-week low of $37.67. While the stock recovered marginally and closed at $38.51, it is still down almost 75% for the year.

While stay-at-home stocks have been weak this year, Peloton is among the worst performers. What’s the forecast for PTON stock and is it a good buy now after the crash?

Peloton stock recent developments

A fictional character in Sex and the City died while using Peloton equipment. There couldn’t be any further negative publicity for the company whose equipment was involved in a fatal accident. While initially, the company’s response to the accidents wasn’t up to the mark, it later went for product recall.

Meanwhile, Peloton hasn’t taken too kindly to the portrayal of its equipment and has hit back with a counter advertisement narrated by Ryan Reynolds. “And just like that… the world is reminded that regular cycling stimulates and improves your heart, lungs and circulation, reducing your risk of cardiovascular diseases. Cycling strengthens your heart muscles, resting pulse and reduces blood-fat levels,” says the advertisement.

68% of all retail investor accounts lose money when trading CFDs with this provider.

PTON has faced multiple issues

Peloton has faced multiple issues this year. It is facing supply chain issues like many other companies. However, soon the supply side scare gave way to demand concerns. Amid the controversy over the safety of its equipment, PTON has also lowered the prices for its original bike. Incidentally, the company lowered the price at a time when companies have had to increase prices amid higher input costs.

Peloton lowered its guidance

Peloton also lowered its guidance for the fiscal year during the earnings call last month. It expects to post revenues between $4.4-$4.8 billion in the full fiscal year with a gross margin of 32%. It expects to have between 3.35-3.45 million connected subscribers by the end of the year. It, however, expects to post an EBITDA loss between $425-$475 million in the year.

During the previous earnings call, PTON had guided for revenues of $5.4 billion in the fiscal year. At the midpoint of the guidance, the company has dialed back its revenue forecast by $800 million. At the same time, it has increased the projected EBITDA loss by $125 million.

The stock tumbled after the earnings release. While it saw some upwards price action after the emergence of the omicron variant, the gains could not sustain and the stock drifted even lower.

Pandemic winner

Peloton was among those pandemic winners that that benefited from the changed consumer behavior. As gyms were closed, many people pivoted towards home fitness equipment which helped propel Peloton’s sales as well as shares higher. However, as is the case with other pandemic winners including Teladoc and Zoom Video Communication, the sales growth has come down significantly. Even the mighty Amazon hasn’t been able to skip the slump and has missed topline estimates for two straight quarters.

Here it is worth noting that Peloton has had to increase its sales and marketing budget amid the negative publicity from the recall. In the fiscal first quarter, its sales and marketing expense rose 148% from the previous year and represented 35% of the sales. It not only missed revenue estimates in the fiscal third quarter but its losses were also wider than expected.

PTON stock price forecast

Wall Street analysts have a split rating on PTON stock and 16 of the 31 analysts covering the stock rate it as a buy. 13 analysts have a hold rating while the remaining two rate it as a sell. The stock’s median target price of $75 is a 95% premium over current prices. The street high target price of $110 is a 185% upside while the street low target price of $45 is a 16.8% premium. After the crash, Peloton stock trades even below its street low target price.

Over the last month, several analysts lowered their target price on PTON stock. Its median target price was $130 before the earnings release. However, there was a flurry of analyst downgrades following the company’s fiscal third-quarter earnings miss last month.

Cowen sees Peloton as a top 2022 pick

Meanwhile, Deutsche Bank took a contrarian approach and initiated coverage with a buy rating and a $76 target price. “There are scenarios in which PTON still goes lower from here. But, in our opinion, there are more scenarios that result in greater upside — again based on a fundamental and unemotional analysis of the company’s earnings power in a ‘normalized,’ fully-reopened economic environment,” it said in its note.

The brokerage sees a hybrid model in the fitness industry and expects Peloton to flourish even as the gyms reopen.

PTON stock long-term forecast

The long-term outlook for home fitness equipment companies like Peloton looks positive. While the growth rates of 2020 might not be sustainable, the industry should see secular growth over the long term. PTON is also building a factory in the US to support the demand.

From the home fitness market, Peloton is now also diversifying into the commercial market. Earlier this year, it had acquired Precor and is now integrating the two businesses to target the hospitality sector.

Peloton tried to portray a rosy long-term forecast during the earnings release. It said, “While we are reducing our near-term forecast, our confidence in and commitment to our strategy is unchanged. Software and streaming media have redefined at-home fitness and are driving a migration of workouts into the home, a consumer behavioral shift that we believe is still in its early stages.”

Sounding optimistic on the long-term growth potential, PTON said We remain convinced that the growth opportunity for Peloton is substantial and this informs our decision to prioritize accessibility and household acquisition over near-term profitability, particularly as our industry-leading net promoter scores (“NPS”) and retention rates support a very strong consumer LTV (lifetime value) and unit economics.”

Should you buy Peloton stock?

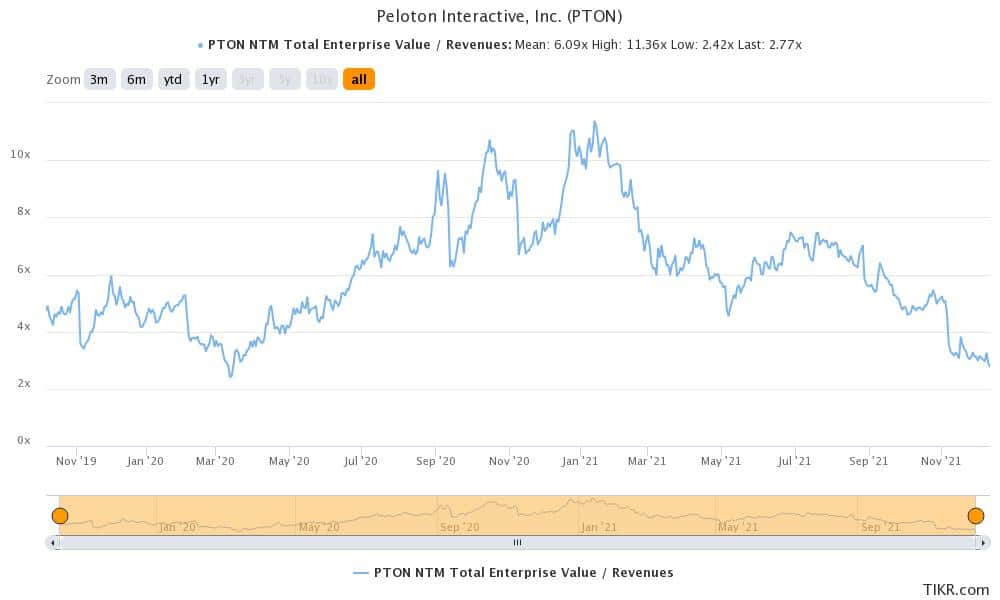

Peloton stock is looking bearish on the charts and has been hitting new lows. It also trades below all key moving averages after having fallen to a new 52-week low. Meanwhile, the stock looks quite attractive based on the fundamentals and its NTM (next-12 months) EV-to-sales multiple of 2.7x is almost the lowest since it was listed in 2019.

All said, PTON stock looks a good buy at these prices and the recent weakness looks like a good buying opportunity. The stock should recover from these levels and 2022 might turn out to be a far better year for the company.

Buy PTON Stock at eToro from just $50 Now!