PayPal Stock Price Forecast January 2022 – Time to Buy PYPL Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

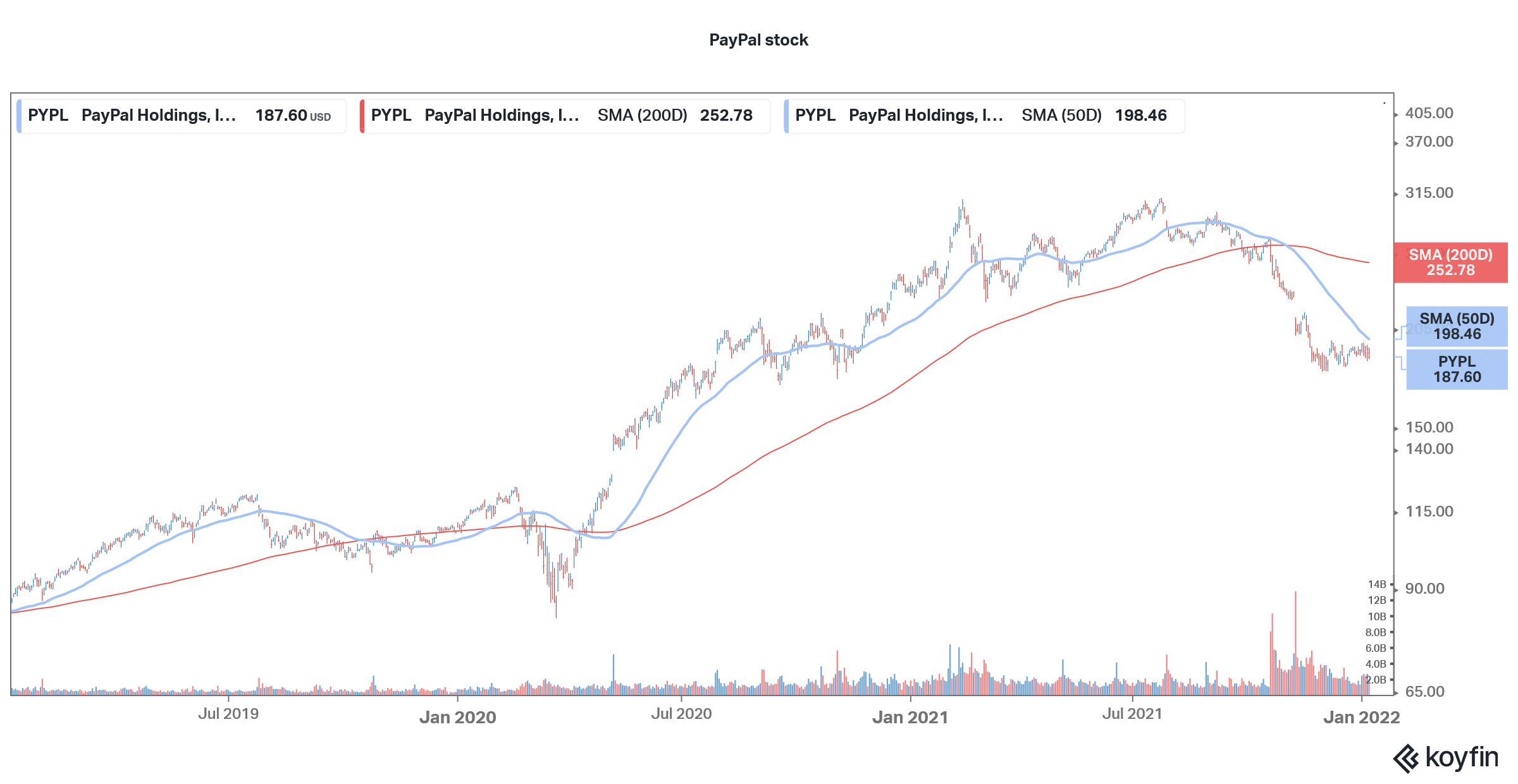

PayPal (NYSE: PYPL) stock has lost 17.3% over the last year and is underperforming the markets by a wide margin. PYPL is not alone and other fintech stocks have also whipsawed over the last year and went through a boom-bust cycle.

Other fintech names have also been quite volatile and have come off their 2021 highs. This includes famous names like SoFi, Affirm, and Square. 2022 hasn’t been any better for fintech stocks and they have come under pressure. What’s the forecast for PYPL stock and is it a good buy for 2022?

Why has PayPal stock been falling?

There has been a sell-off in growth names and fintech stocks have especially come under pressure. In November, PYPL stock had its worst day since March 2020, as investors gave a thumbs down to its third-quarter earnings release. PayPal provided lower-than-expected guidance for the fiscal year 2022 and said that it expects revenues to be $30 billion, which was below the $31.6 billion that analysts were than expected. Several growth stocks tumbled in 2021 as their topline growth fell short of expectations.

Commenting on the slowdown PayPal’s CEO Dan Shulman said “We are seeing the impact of global supply chain shortages in our merchant base, consumer confidence is weakened with the absence of stimulus payments, and with the economy reopening, more people may be likely to do their holiday shopping in-store.”

68% of all retail investor accounts lose money when trading CFDs with this provider.

PayPal stock forecast

While some of the Wall Street analysts have lowered PayPal’s target price, the consensus view is quite bullish on the stock. Of the 49 analysts covering the stock, 42 have a buy rating. Four analysts have a hold rating while the remaining three analysts have a sell rating. The stock’s median target price of $268 is a premium of almost 42%. The street low target price of $172 is an 8.3% discount while the street high target price of $345 is a premium of 84% from these price levels.

There has been a massive sell-off in payments companies. While PayPal is trading close to its 52-week lows, Paysafe that went public through a SPAC merger is trading at a fraction of its 52-week highs.

BMO finds PYPL stock attractive

Meanwhile, BMO believes that the sell-off in PayPal stock is overdone and the stock looks set for a rebound. “We believe PYPL faces uncertainty regarding the impact of competition, macroeconomic trends, and business mix on growth and margins; however, our growth-margin sensitivity analysis implies valuation risks are now skewed to the upside,” said BMO in its note.

While the brokerage lowered its target price from $278 to $224, it upgraded it to outperform. “PYPL is the preferred digital wallet option for online merchants [excluding Amazon], offering a seamless and secure check-out experience for consumers. We expect PYPL will continue to grow its volumes above the industry rate (global e-commerce ex-AMZN), with potential upside risk from Venmo, [buy now, pay later], Super-App, [point of sale], and partnership monetization efforts,” said BMO in its note.

Wall Street analysts lower PayPal’s target price

BMO is not the only brokerage that has slashed PayPal’s target price. This month only, RBC lowered its target price from $298 to $230 while maintaining the outperform rating. The brokerage believes that PYPL is an “under monetized” business. However, it still lowered the target price citing the multiple contraction of peer companies as well as the rising interest rates.

Higher interest rates are particularly negative for growth companies as their earnings are skewed towards the future. A lot of growth companies have seen a severe contraction in their trading multiples amid the feared rate hikes from the US Federal Reserve.

DA Davidson had also lowered PayPal’s target price following the third-quarter earnings and said “PYPL was one of the pandemic’s biggest beneficiaries, but the uneven global macro recovery amid supply chain issues as well as tough comps are challenging growth prospects.”

PayPal stock long term forecast

While PayPal’s growth has come down in the short term, like many other pandemic winners, the company’s long-term growth outlook looks strong. It has been expanding its offerings and last year announced a partnership with Amazon which would allow US users on the platform to pay with Venmo.

“Over the last year, we have focused on giving our Venmo community more ways to use Venmo in their daily lives, including the ability to pay with QR Codes and providing more shopping features like purchase protections,” said Darrell Esch, Senior Vice President, and GM, Venmo.

Last year only, Amazon partnered with BNPL (buy-now-pay-later) company Affirm wherein select users on the platform got the option to pay using Affirm’s BNPL solutions.

PYPL stock technical analysis

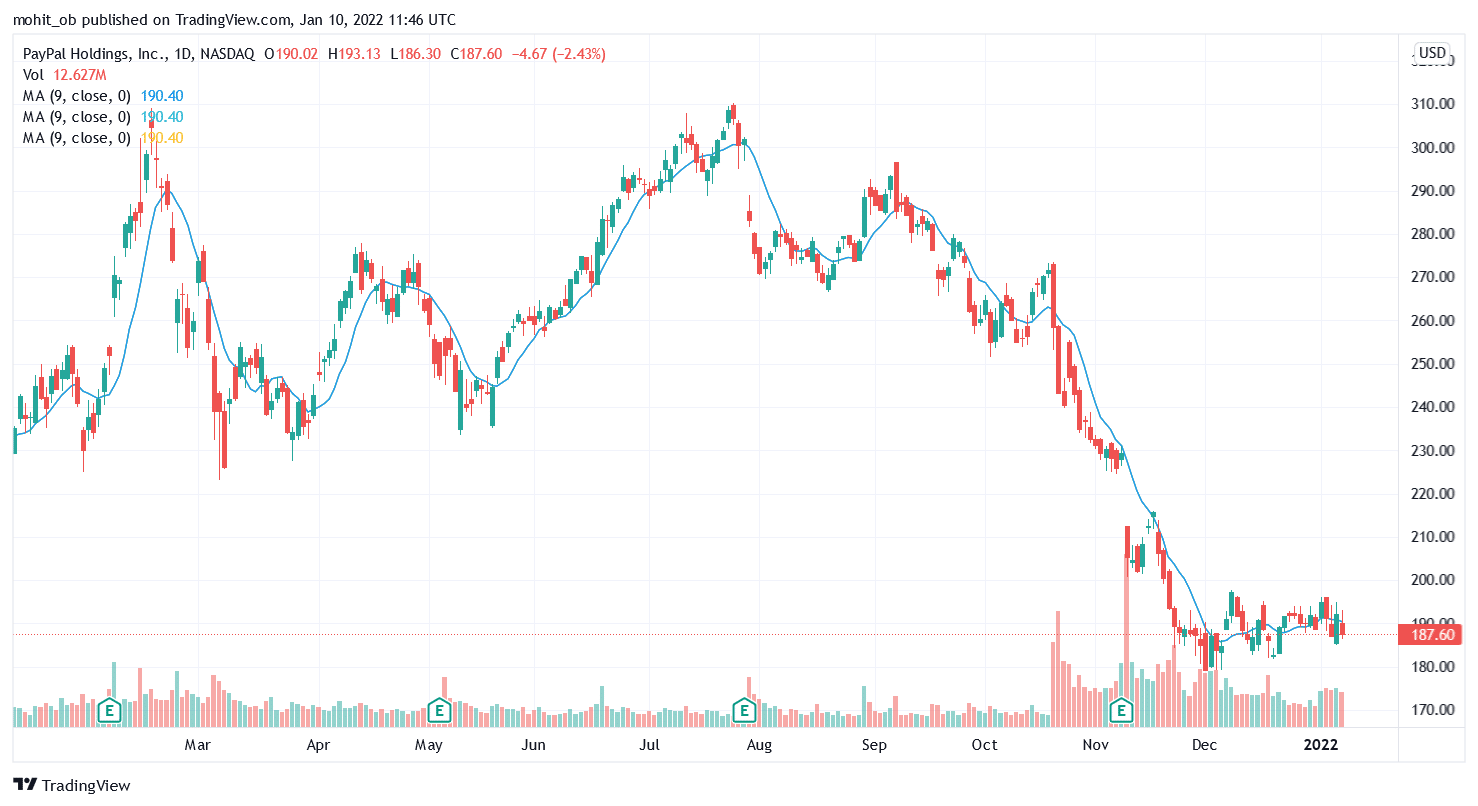

PayPal stock is looking very bearish on the charts and trades below all the key moving averages including the 50-day, 100-day, and 200-day SMA. The 50-day SMA has especially been strong resistance for the stock. It has been in a downwards price channel but has been consolidating at current price levels. The stock could break out of the narrow price channel if it can cross above the 50-day SMA.

Should you buy PayPal stock?

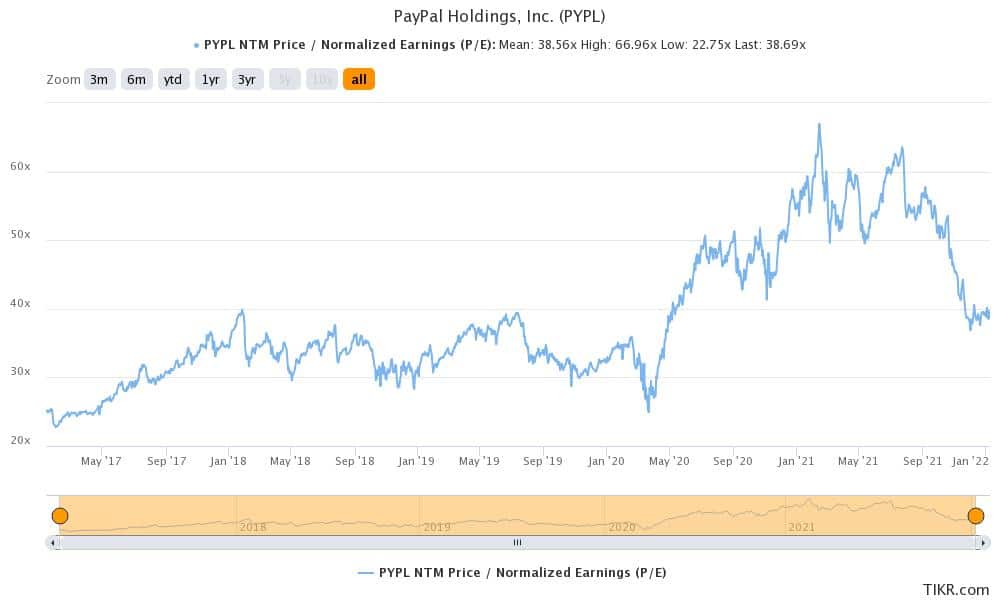

PayPal stock trades at an NTM (next-12 months) PE multiple of 38.7x. The multiples are much lower than the average multiples over the last year but are still slightly higher than the pre-pandemic levels. A similar story is playing out in other companies whose earnings had spiked during the lockdowns in 2020 but the growth has since tapered down.

Overall, PYPL looks like a good fintech stock to buy after the recent underperformance. The fintech industry holds long-term promise and PayPal is one fintech name that offers a mix of growth and stability.

Buy PYPL Stock at eToro from just $50 Now!