Opendoor Stock Price Forecast August 2021 – Time to Buy OPEN?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Opendoor (OPEN) stock was trading sharply higher in US premarket price action today after reporting spectacular earnings for the second quarter. What’s the forecast for OPEN stock and is it a good buy in August 2021?

Opendoor went public last year through a reverse merger with a SPAC (special purpose acquisition company) sponsored by Chamath Palihapitiya. The stock has had a turbulent ride and is down 63% from its 52-week highs.

Opendoor earnings

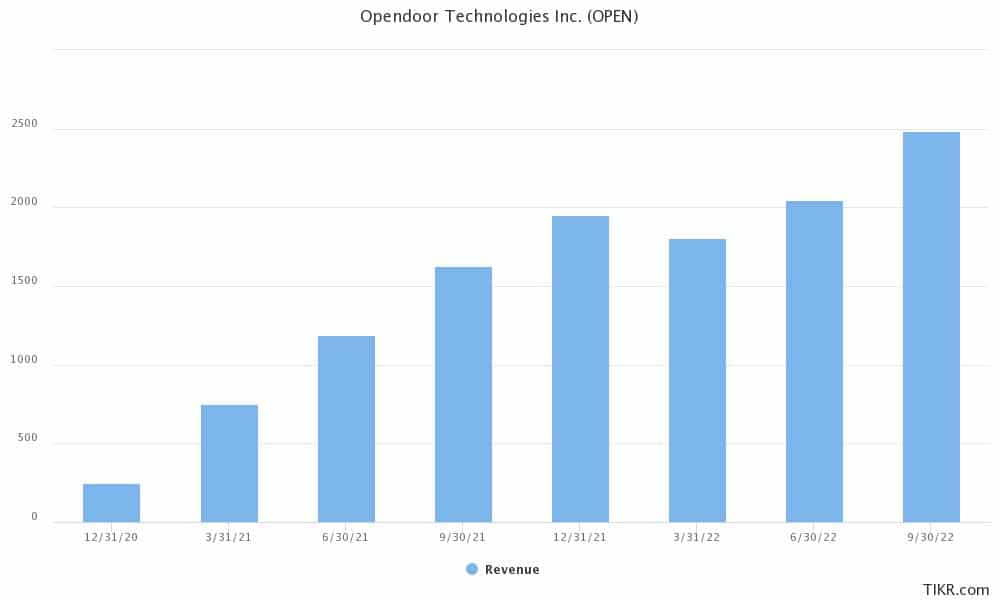

Opendoor reported revenues of $1.2 billion in the second quarter which were 59% higher than what it generated in the first quarter. The home flipping platform sold 3,481 homes in the quarter which was 41% higher than the previous quarter. The company’s gross margin expanded 40 basis points in the quarter to 13.4%. Opendoor posted a gross profit of $159 million in the quarter which was 64% higher than the previous quarter.

OPEN posted an adjusted EBITDA of $26 million in the quarter as compared to an EBITDA loss of $2 million in the previous quarter. The company’s net loss also narrowed to $144 million in the quarter, as compared to $270 million in the previous quarter.

67% of all retail investor accounts lose money when trading CFDs with this provider

OPEN expands to new markets

Opendoor expanded to 12 new markets in the quarter and was present in 39 markets at the end of the second quarter. The company purchased 8,494 homes in the quarter which was 136% higher than the previous quarter. Its inventory of homes rose to $2.7 billion at the end of the quarter which was 224% higher than what it had at the end of the first quarter. Opendoor ended the quarter with cash and cash equivalents of $1.8 billion.

Eric Wu, Co-Founder, and CEO of Opendoor sounded upbeat after the results. “This strong outperformance is further evidence of the seismic shift in consumer demand towards the modern real estate experience we are pioneering. Based on our current momentum, we are operating today at a second half revenue run rate that is on track to meet the 2023 target we provided at the time of our December listing,” he said in the release.

Opendoor’s topline, as well as bottomline, were better than expected. Also, the company’s guidance was ahead of what analysts were expecting. OPEN expects to post revenues between $1.8-$1.9 billion in the third quarter. It expects to post adjusted EBITDA between $15-$25 million in the third quarter.

OPEN stock technical analysis

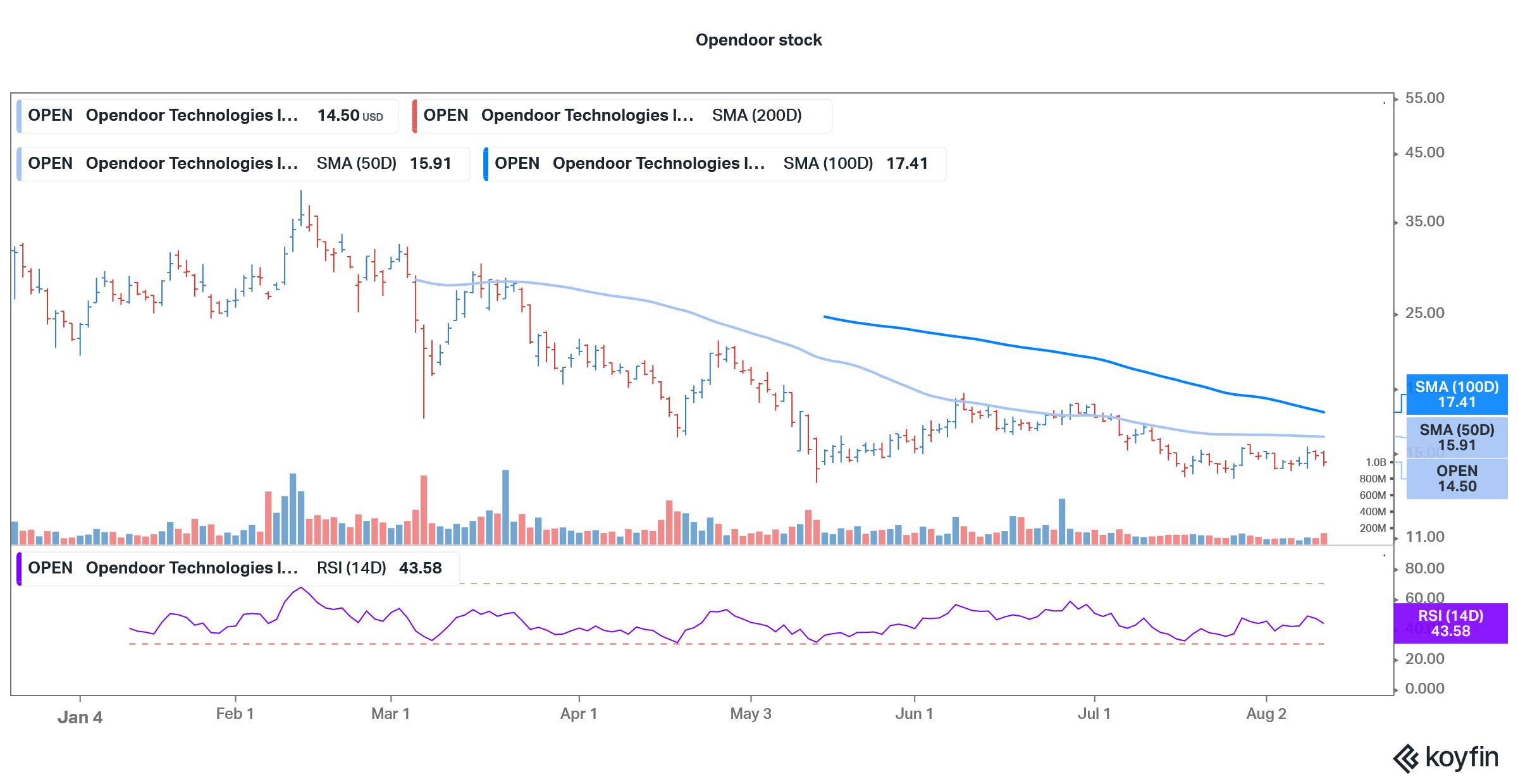

Opendoor looks set to cross above the 50-day SMA (simple moving average) in today’s price action. The 50-day SMA has been strong resistance for the stock and the surge today would take it past the level. The next key level to watch would be the 100-day SMA which is currently at $17.41. If the stock rises above the 100-day SMA also, it would signal a strong uptrend.

Opendoor stock forecast

Wall Street analysts are bullish on OPEN stock. Of the eight analysts polled by CNN Business, five rate the stock as a buy while the remaining three rate it as a hold. None of the analysts have a sell or equivalent rating on the stock.

Its median target price of $33.50 implies an upside of 131% over current prices. Its lowest target price is $17 which is a premium of over 17.3% while the highest target price of $42 is a premium of almost 190% over current prices.

Opendoor stock long term forecast

The long-term forecast for Opendoor stock looks positive. The real estate market in the US is worth $1.6 trillion annually but only 1% of buying and selling in the market happens on digital platforms. Real estate is another frontier that e-commerce is looking to penetrate and companies like Opendoor are at the forefront amid the transformation.

The outlook for the US real estate market is reasonably strong despite lingering concerns of a bubble. Also, while the expected increase in interest rates is a headwind for companies like OPEN, the US Federal Reserve wouldn’t raise rates in a hurry and would be very patient. Overall, OPEN looks like a good way to play the digitization of the US housing market.

OPEN stock valuation

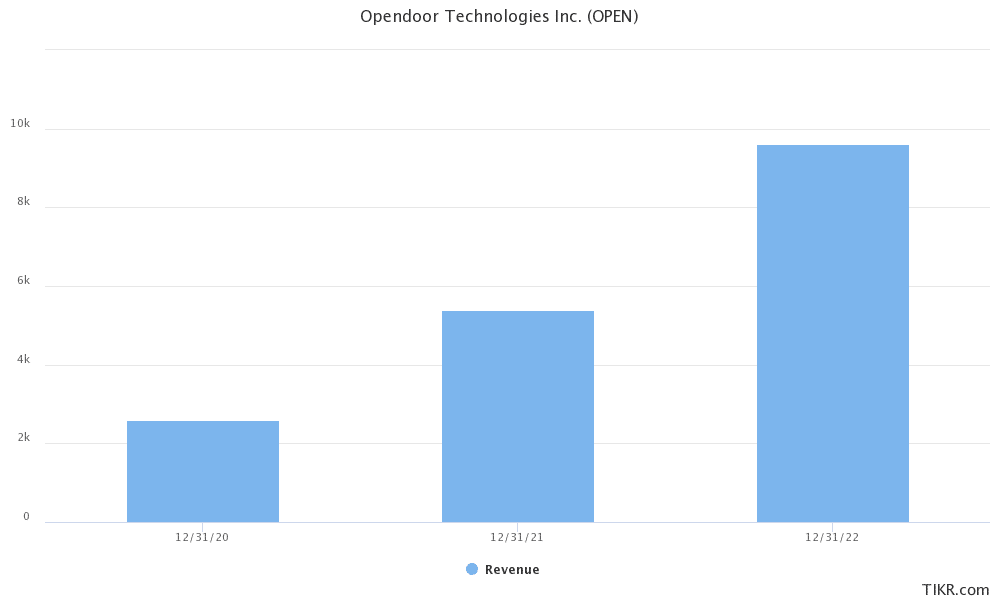

Analysts expect the company’s revenues to rise 108% in 2021 and 79% in 2022. As Opendoor expands to new markets and the momentum in the US housing market continues, it could end up surprising on the upside on the topline. Also, the company turning positive on the EBITDA level is a positive sign.

OPEN stock trades at an NTM (next-12 months) EV-to-sales multiple of only 1x. This is the lowest that the stock has traded since listing. The multiple has averaged 3.5x since the listing while it peaked at 8.4x.

Opendoor is a good stock to buy looking at the strong growth outlook and tepid valuations. Notably, OPEN trades at a big discount to Zillow and might see a valuation rerating. Opendoor could also potentially expand into multiple ancillary services which will add shareholder value in the medium to long term.

67% of all retail investor accounts lose money when trading CFDs with this provider