Match Group Stock Up 17% in September – Time to Buy MTCH Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Match Group stock is up 17% so far in September following the release of the company’s Q2 2021 earnings report in which the owner of the Tinder app reported better-than-expected top-line results and forward guidance.

For the three months ended on 30 June, Match saw its total revenues rise to $708 million or more than 27% higher than the same period a year ago while also exceeding the consensus forecast of $694 million for the period as per data from Capital IQ.

Meanwhile, even though adjusted net earnings per share came in significantly lower than expected at $0.46 – 9 cents lower than the consensus – the management’s revenue guidance for both Q3 and the full 2021 fiscal year exceeded Wall Street’s estimates and that may have helped the stock in recovering from the downtrend it experienced after the report came out.

Moreover, on 7 September, the stock experienced a pronounced 7.5% single-day uptick after it was announced that MTCH stock will join the popular S&P 500 index in substitution of Perrigo (PRGO).

Has this addition to one of the world’s most popular stock market benchmarks be a game-changer for Match Group stock? In the following article, I’ll assess the stock’s current technical setup and fundamentals to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Match Group – Technical Analysis

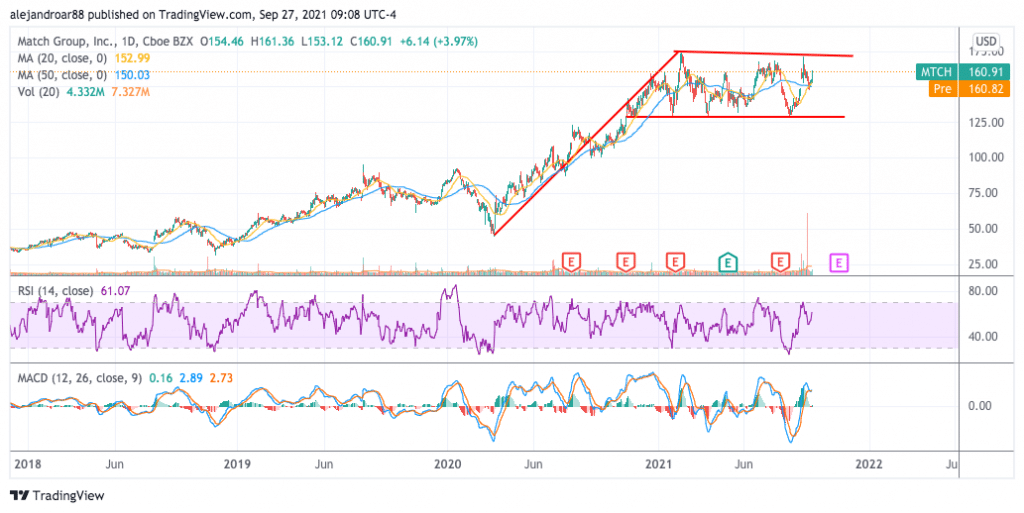

In a previous article, we anticipated that the decline the stock suffered upon missing Wall Street’s estimates for its Q2 earnings will lead to a pronounced downtrend and that is exactly what happened as the price of Match stock dropped 7% over the next 10 sessions.

However, the stock appears to have bottomed upon tagging a long-dated horizontal support at $130 and has steadily risen since then even though the bullish gap left behind after news of its addition to the S&P 500 has been filled in the past few days.

Notably, trading volumes surged more than 7 times above the 10-day average on 17 September only a few days before the company announced the pricing of a senior notes offering along with a direct offering of shares that was set to start on 24 September.

Somehow counterintuitively, this announcement – which is typically bearish – resulted in a 4% jump in the price of MTCH stock on the day that the direct offering commenced.

At the moment, the outlook for the stock is not directionally biased unless its short-term moving averages are broken. In that case, the outlook would turn to the bearish side as the price action rejected a climb above the trend line resistance on 10 September and that may trigger a decline in the short term.

To possibly define the direction that the stock will take in the future, it would be important to keep an eye on the Relative Strength Index (RSI) to see if it makes a lower high even if the price keeps climbing. That would result in the formation of a bearish divergence in this momentum oscillator – which would further favor a bearish outlook.

For now, unless the price makes a move either below the short-term simple moving averages or above the upper trend line support highlighted in the chart, the outlook is neutral.

On the other hand, a flag pattern seems to be in play and, if the price breaks above the $172 level, chances are that the uptrend that the stock experienced since the pandemic crash might be resumed.

Match Group – Fundamental Analysis

Match is the parent company of the popular dating app Tinder, which accounts for more than 55% of its revenues as per data from its latest quarterly report. The company was spun off by its former parent IAC back in 2018 and since then it has reported positive top-line growth of around 17% per year while sales are expected to accelerate this year to jump 25% compared to a year ago based on the management’s latest guidance.

Gross margins during that period have been steadily declining from 76% to 73% but operating margins have remained stable at around 31%.

Meanwhile, during that same period, normalized diluted earnings per share progressively expanded from $0.89 to $1.34 at a compounded annual growth rate of 23%. Moreover, a simple run rate of the firm’s adjusted diluted earnings per share for the first semester of 2021 would point to bottom-line results of $2.08 per share for the year – a 55% year-on-year climb.

However, Match’s debt is quite high as the company has $3.85 billion in long-term debt, most of which carries a 4% to 5% interest rate. By the end of the second quarter, total assets landed at $4.4 billion including $236 million in cash and equivalents and around $3.2 billion in goodwill and intangibles.

Even though most of its debt is due in 2026 and forward (except from one senior note due in October 2022), this elevated level of borrowings will probably weigh on the company’s valuation for a while as interest expenditures are eating nearly a quarter of its GAAP operating income.

That said, the company’s recently issued $500 million in senior notes due in 2031 will be used to pay off the upcoming 2022 commitment and market participants seem to have greeted the placement of these notes as positive news as Match’s solvency is not a concern at the moment.

At its current price of $160.9 per share, the company is being valued at 63 times its forecasted adjusted earnings per share for the next 12 months. This valuation seems stretched based on the firm’s past bottom-line growth.

However, if the tailwind provided by the pandemic has a long-lasting effect on the business, chances are that Match’s profitability may grow at an accelerated pace moving forward and that would justify, to some extent, its current market cap.

Nonetheless, based on the firm’s elevated level of debt and possibly stretched valuation, the outlook, from a fundamental perspective, is neutral as well.

Buy MTCH Stock at eToro with 0% Commission Now!