Match Group Stock Down 5% – Time to Buy MTCH Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Shares of the online dating giant Match Group slid 1.8% yesterday and they are down more than 5% this morning after the company reported its financial results covering the second quarter of its 2021 fiscal year.

The parent company of the popular Tinder app reported revenues of $707.8 million during the three months ended on June 2021, up from $555.5 million it brought during the same period a year ago while surpassing analysts’ estimates of $694 million for the quarter.

Meanwhile, the company’s payers – a recently incorporated metric that tracks the number of users that contributed to the firm’s revenues – moved from 13 million last year to 15 million by the end of the second quarter of 2021 for a 15% year-on-year uptick.

Tinder direct revenues accounted for 56.4% of the firm’s total top-line results at $399 million – in line with last year’s trends – while the company reported total revenues per payer of $15.5 – up 10% from the previous year.

As per its profitability, Match reported a 7.3% jump in its operating income, which landed at $209.9 million but this still resulted in a sharp drop in its operating margin as it ended the period at 29.7%, down from 35.2% the company reported a year ago.

Diluted earnings per share went down 27.8% to $0.46 amid this deterioration in the company’s bottom-line profit margins while fully diluted shares leaped from 207.8 million to 311 million.

Analysts were expecting to see basic earnings per share landing at $0.55, meaning that the company beat estimates by one cent.

Moving forward, the management is expecting to see sales landing at around $790 and $805 million for the third quarter along with an EBITDA of around $280 million for Q3· and $1.06 billion for the entire 2021 fiscal year.

Could today’s single-day downtick be providing an opportunity to buy Match shares at an attractive price? The following article takes a closer look at the price action along with analyzing the firm’s fundamentals to see if this could be an opportunity to enter a long position on the online dating giant.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Match Group Stock – Technical Analysis

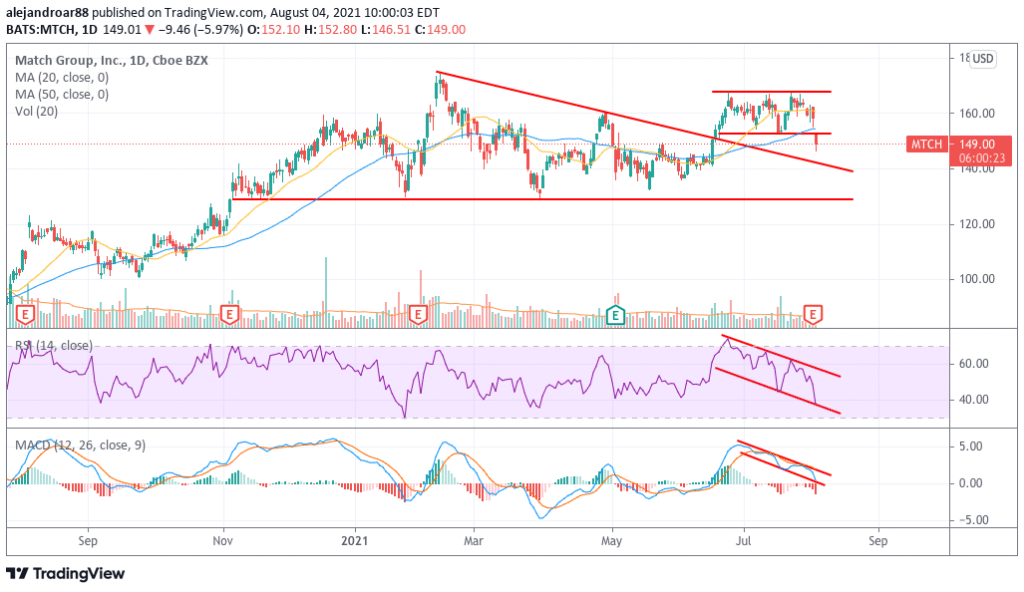

The latest consolidation experienced by Match’s stock seems to have resolved to the downside as a result of today’s sharp drop, with the price breaking below the issue’s latest intraday low.

Momentum readings were already bearish before the release of this earnings report as shown by a downtrend in both the Relative Strength Index (RSI) and the MACD even though the stock traded range-bound.

Trading volumes were already fairly elevated yesterday as they surpassed the 10-day average while today’s volumes will probably exceed that threshold as well as sellers seem to be dumping their Match shares in expectation of a deceleration of the firm’s latest growth on the back of a fading pandemic tailwind.

In this regard, the company’s revenues could suffer moving forward as a result of more people going out on regular dates instead of relying on Match’s apps to interact. If that is the case, chances are that the stock’s latest negative momentum could accelerate.

For now, the outlook for Match seems bearish based on technical readings but the total downside risk is fairly small as the trend line resistance – which should act now as support – is at a close distance.

However, if the stock drops below that level, losses could accelerate as the price action could retest the $130 level shortly afterwards.

Match Group Stock – Fundamental Analysis

Revenues for Match had been growing steadily in the past two years, moving from $1.73 billion back in 2018 to $2.39 billion by the end of 2020 at an average rate of 17%. Meanwhile, during the first semester of 2021 have already advanced 25% at $1.38 billion while they are expected to land at $2.89 billion for a 21% jump.

Meanwhile, the company recently acquired Hyperconnect, a live video and audio chat app from South Korea whose services might be integrated with Match’s multiple dating apps to further enrich the range of interactions that users can have through the platform.

As a result of this acquisition, Match’s annual sales should now accelerate to $3 billion as a result of a $135 million expected contribution of Hyperconnect to the firm’s top-line results this year.

The firm’s top-line margins have been deteriorating in the past years, with gross margins moving from 76.3% to 73.6% from 2018 to 2020 while EBITDA margins have stood fairly flat at 33%.

Meanwhile, net margins are showing a worrying downtrend as they have moved from 36% in 2018 to 5.4% in 2020 as a result of losses coming from discontinued operations of Former IAC.

Moving forward, analysts are expecting to see earnings per share picking up their pace as non-GAAP EPS is forecasted to land at $2.85 in 2022 for a 20% jump compared to this year’s forecasted figure and $3.6 by the end of 2023 for a 25% YoY advance.

Based on the management’s forecasts, at a market capitalization of $43.7 billion, Match would be trading at around 14.5 times its forecasted sales for 2021 and at 43 times its forecasted EBITDA for the period.

Historically, the firm has managed to increase its EBITDA at a rate of around 16.5% which makes the current trading multiple a bit lofty, particularly if the firm is expected to experience a deceleration in its growth rates moving forward.

Based on the bearish readings identified on the technical front and this seemingly stretched valuation, Match shares seem to be poised to experience further downward momentum.

Buy Stocks at Cedar FX, the World’s #1 trading platform!