Lululemon Athletica Stock Price Rises 13% – Time to Buy LULU Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Lululemon Athletica (LULU) stock was trading almost 13% higher in US premarket price action today after markets gave a thumbs up to its earnings and outlook. What’s the forecast for LULU stock and is it a good buy?

Lululemon Athletica released its fiscal second-quarter 2021 earnings after the close of US markets yesterday. The earnings were better than expected on almost all the metrics.

Lululemon Athletica earnings

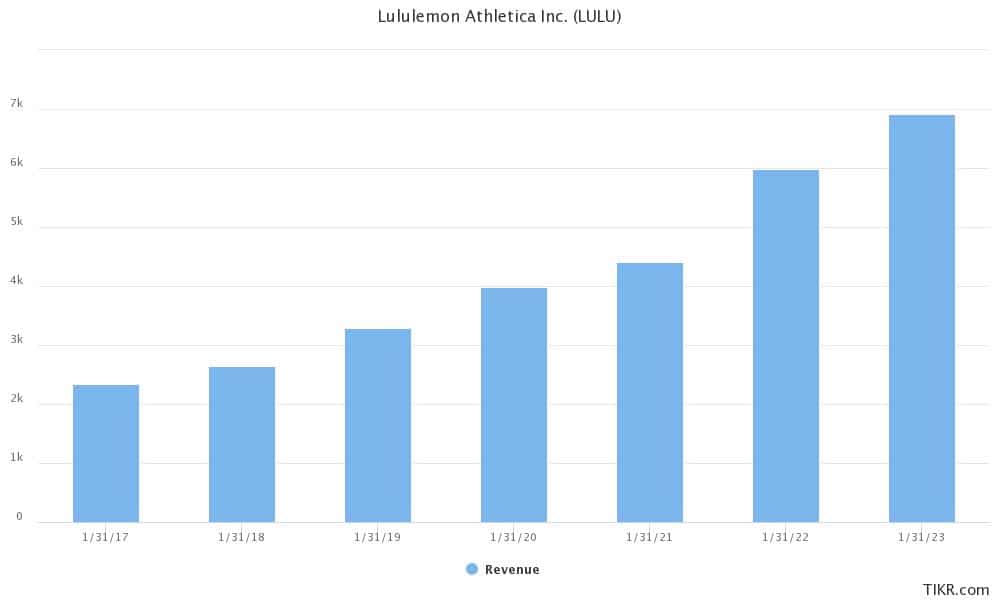

Lululemon Athletica reported revenues of $1.45 billion in the fiscal second quarter that ended in July. The revenues were 61% higher than the corresponding period last year and were 56% higher on a dollar-neutral basis. While the steep rise is coming from a low base, the revenues were significantly higher than the $1.34 billion that analysts were expecting.

LULU reported an EPS of $1.65 in the quarter which was also better than the $1.19 that analysts were expecting. Expressing optimism over the earnings, Calvin McDonald, Lululemon CEO said “Our second quarter results demonstrate the continued momentum across the business, and how we are living into our Power of Three growth plan and Impact Agenda commitments. We launched exciting new products, experienced strength across channels and geographies, and announced new partnerships that will allow us to become a leader in product sustainability.”

67% of all retail investor accounts lose money when trading CFDs with this provider.

Key takeaways from LULU earnings

Lululemon Athletica reported a 390 basis point expansion in its gross margins. Its gross profits increased 72% to $842.7 million during the period and the margin was a healthy 58.1%. During the quarter, it opened 11 new company-owned stores and ended the quarter with 534 stores. Notably, the company’s revenues were significantly higher than what it had reported in 2019. Over the last two years, its revenues have increased at a CAGR of 28% while gross margin has expanded 310 basis points over the period.

Lululemon Athletica raises guidance

With Lululemon Athletica’s earnings were better than expected, its guidance looked even better. It expects to post revenues between $1.40-$1.43 billion in the fiscal third quarter and between $6.19-$6.26 billion in the full fiscal year. Both the guidance was better than expected.

“The guidance and outlook forward-looking statements made in this press release are based on management’s expectations as of the date of this press release and does not incorporate future unknown impacts from the spread of COVID-19,” it cautioned in its release. LULU also admitted to supply-side issues which have been highlighted by many other companies as well.

Notably, looking at the company’s guidance, it looks set to surpass its 2023 guidance this year only. Markets look quite impressed with the performance and the stock looks headed for a record rally.

LULU stock forecast

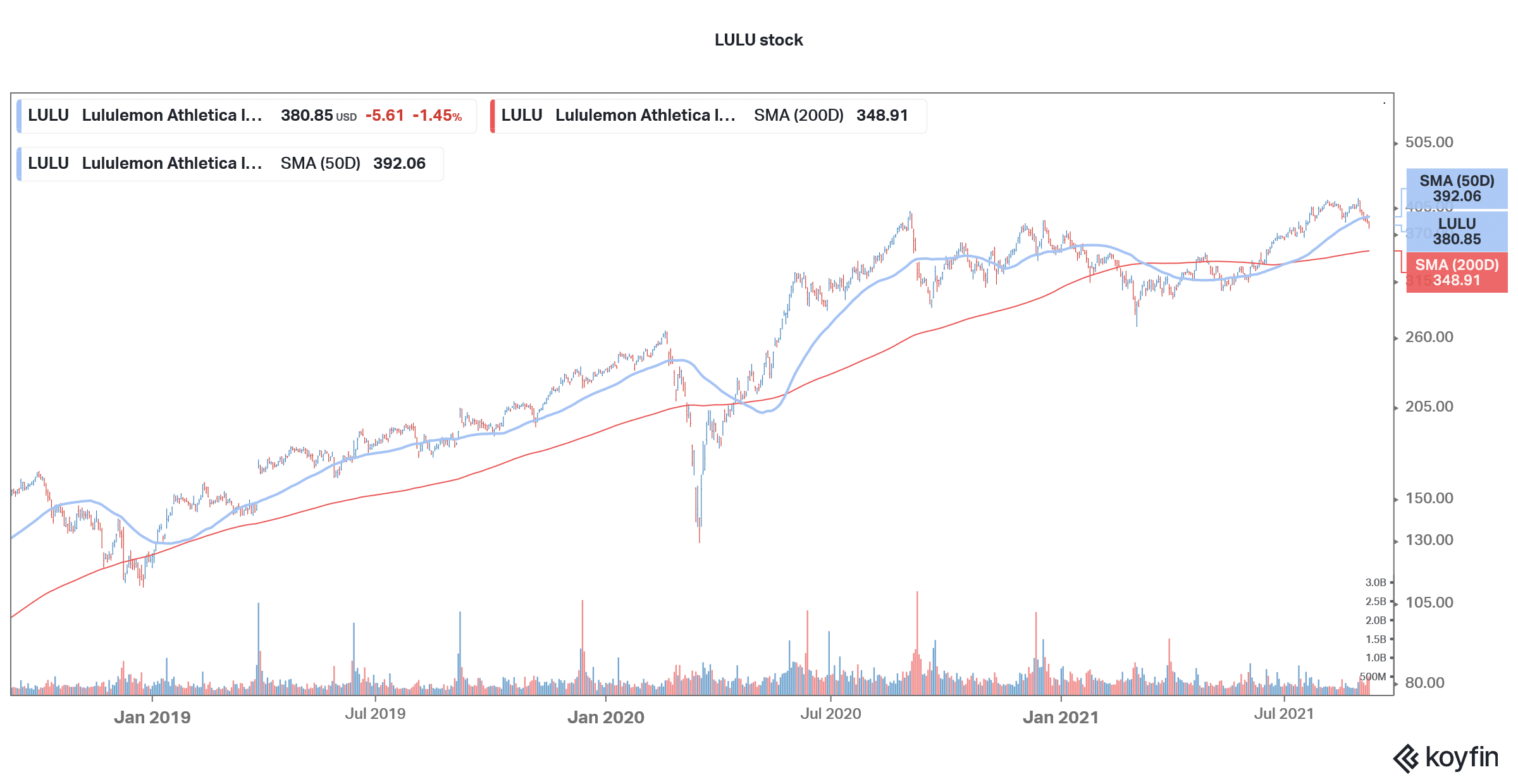

Prior to the rise today, Lululemon Athletica stock has been having a dismal year. The stock is up only about 7% for the year which is only about a third of what the S&P 500 has returned during the period. Forecast estimates call for an 11.5% upside from these levels. The stock’s street-high target price of $481 is a premium of 26.3% over the next 12 months.

Here it is worth noting that these forecasts were provided before the earnings release. More analysts are expected to upwardly revise their target prices on LULU stock after the spectacular earnings and guidance.

Ahead of the earnings release, MKM Partners had raised its target price from $390 to $419 while Telsey Advisory Group had raised its from $440 to $460. Overall, of the 30 analysts covering Lululemon Athletica stock, 20 have a buy rating while nine have a hold rating. One analyst has a sell rating on LULU stock.

Goldman Sachs

In July, Goldman Sachs had advised buying LULU stock. “We see best in class premium brand positioning and believe new category momentum (men’s / international / inclusive sizing / footwear) will propel sales and margins, supported by upside from membership initiatives driving consumer engagement,” said analyst Brooke Roach while initiating coverage with a target price of $447.

Lululemon Athletica stock valuation and technical analysis

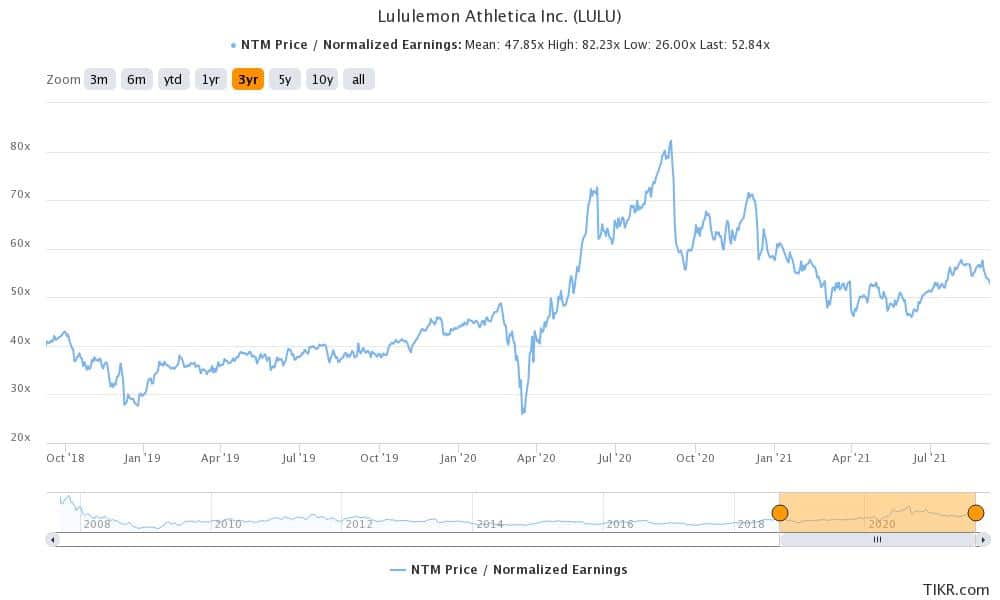

Meanwhile, Lululemon Athletica is among the most expensive retail brands. The stock currently trades at an NTM (next-12 months) EV (enterprise value)-to-sales multiple of almost 8x. Its NTM PE is 52.8x. The metric has averaged 47.9x over the last three years.

There is a section of the market that is apprehensive of Lululemon Athletica’s valuations. Citi, for instance, downgraded the stock from a buy to neutral earlier this month saying the stock is “priced for perfection.”

“The stock trades at ~9x F21E sales and has an EV of ~$50BN, making LULU the most highly valued specialty retail brand ever, double that of the second highest valued brand in history (Victoria’s Secret, in 2015),” said Citi in its note.

Lululemon Athletica stock looks like a buy

Meanwhile, LULU is a fast-growing specialty brand and the premium valuations don’t look too high considering the growth outlook. Looking at the technicals, Lululemon Athletica stock trades at below the 50-day SMA (simple moving average). However, looking at the pre-market price action, the stock could rise above the 50-day SMA which would indicate technical bullishness in the stock.

That said, despite concerns over the valuations, Lululemon Athletica stock looks like a good buy at these levels. Considering the growth outlook, analysts might also take a more bullish view of the stock in the near term.

Buy LULU Stock at eToro from just $50 Now!