Grab Stock Price Falls 63% – Time to Buy GRAB Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

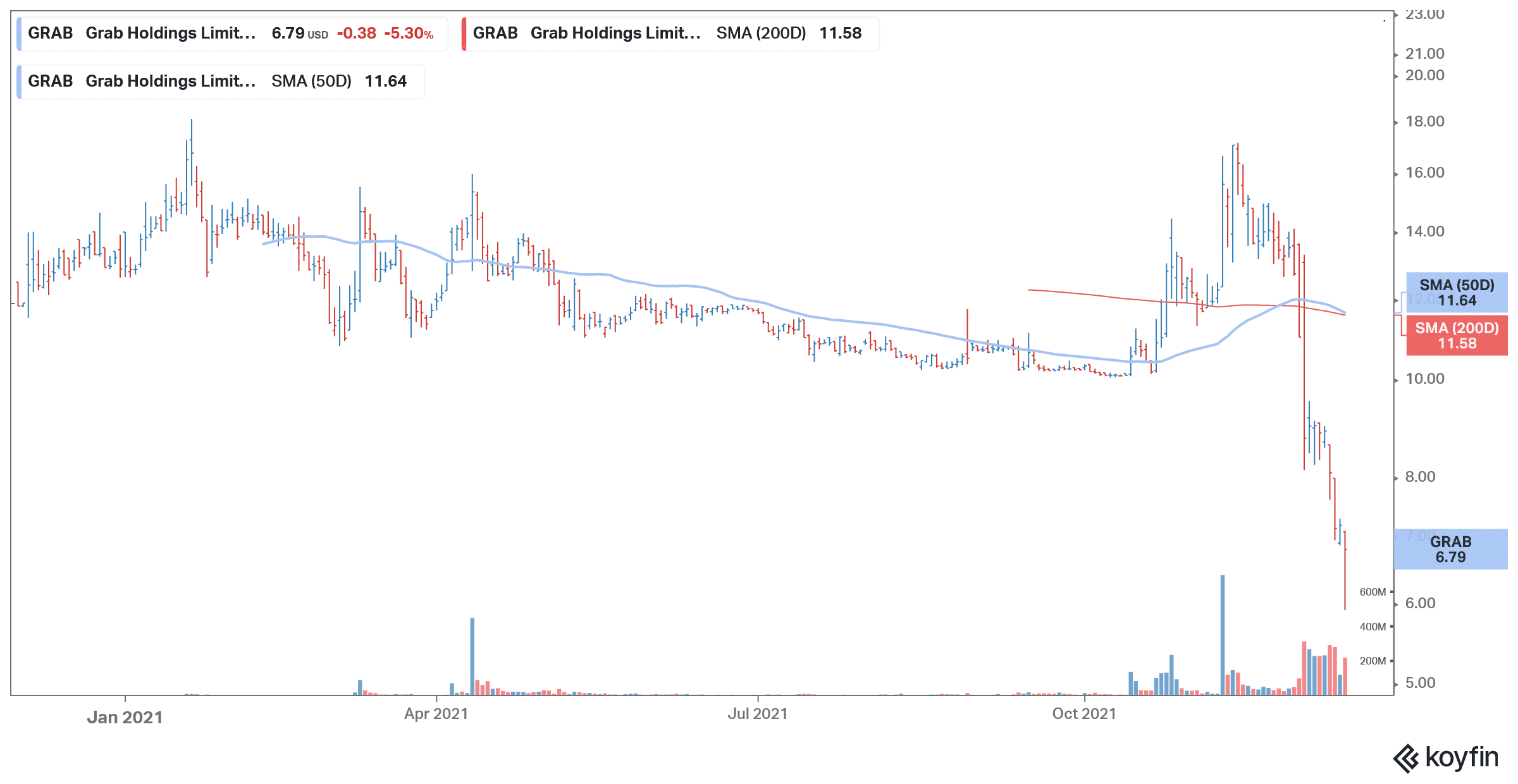

Grab, the Southeast Asian tech company that recently went public through a SPAC reverse merger, fell 5.3% yesterday but was trading higher in premarket price action today. The stock now trades well below the SPAC IPO price of $10 and joins the ranks of many other companies that have fallen below the IPO price.

This includes the hyped mergers like Clover Health, Paysafe, and more recently Planet Lab. Incidentally, the majority of SPACs are trading below the $10 price level after the merger, and almost all of them are well below the 52-week high prices even as the broader markets are near all-time highs. Grab is now trading almost 63% below its 52-week highs. What’s the forecast for the stock and is the fall a good buying opportunity?

Ride-hailing companies have been a wealth destructor

Ride-hailing companies have been a wealth destructor for investors. Uber, Lyft, and most recently Didi trade below the IPO price. One can discount Didi because of the crackdown in China and the eventual delisting from the US markets. However, in general, ride-hailing and food delivery companies haven’t done well. DoorDash has been an exception in the food delivery business but UK-based Deliveroo had tumbled after its IPO earlier this year.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Grab stock recent developments

Grab has announced the acquisition of Jaya Grocer Holdings Sdn, Malaysia’s top premium grocery chain. Earlier this year, the company has also acquired Ovo, the Indonesia-based wallet company. Grab has been betting on fintech space along with the core ride-hailing and delivery business.

The company had also acquired Uber’s ride-hailing business in the region. Notably, Uber’s track record outside of US, especially in Asia has been quite mixed. It also exited the business in China and sold it to Didi, taking a significant stake in the Chinese company in the bargain. While Didi’s IPO was expected to lead to value unlocking for Uber, things did not go as planned and the company’s valuation is now even below the private market valuation.

Grab stock forecast

Since Grab was listed only recently, not many analysts are covering the stock. Earlier this month, JPMorgan initiated coverage on the stock with an overweight rating and a $12.5 target price. “We initiate coverage of Grab with an OW rating and SOTP-derived Dec-22 PT of $12.5. Grab’s superior regional superapp platform is best geared to rising online consumption in ASEAN (Association of Southeast Asian Nations), in our view,” it said in its note.

Southeast Asia has a total population of 670 million and Grab sees its total addressable market rising to $180 billion by 2025. The company expects to post revenues of $4.5 billion and an adjusted EBITDA of $0.5 billion by 2025.

After the recent fall, Grab’s market cap has fallen to $25 billion which gives a 2025 price to sales multiple of 5.5x. The valuations now look a lot more reasonable than they did during the merger.

Long-term forecast

Grab is a play on the long-term growth story in the ASEAN region. The company has a strong moat in the region and is transforming into a superapp. The long-term forecast for the company looks positive. Notably, with Chinese stocks looking risky amid the continued crackdown in the communist country, some investors might find Southeast Asia as a good bet.

Should you buy Grab stock?

Grab was the biggest SPAC merger of all time. However, it also became the worst listing by a Southeast Asian company in the US. As part of the merger, the company received a $4 billion PIPE (private investment in public equity) which again was a record. The company would use these funds to expand its business and also look for inorganic growth as it did with Jaya.

Accounts managed by Morgan Stanley also participated in the PIPE. Dennis Lynch, Head of Counterpoint Global (Morgan Stanley) said “Grab represents a unique growth investment in the dynamic and growing Southeast Asian market. We’re incredibly excited to help fuel the emergence of innovative technology platforms in Southeast Asia.”

The company’s GMV (Gross Merchandise Value) was $11.5 billion in the third quarter which was the third consecutive quarter of record GMV for the company. It completed a billion transactions in the first half of 2021. The average spend per user has also been rising and in the third quarter, it increased 43% YoY.

Good play on Southeast Asia

The company’s diversified business would also be a key long-term driver and over 55% of the customers on the platform have used more than one service as compared to 33% at the end of 2018. The company is now present in 465 cities across eight countries in the region.

Cross-selling and upselling are two key opportunities for Grab. The company continues to add more services on the platform which would help it increase the target market as well as revenues and moves towards the goal of an “everyday everything app. Overall, after the massive crash, Grab looks like a good buying opportunity and play the growing market in Southeast Asia.

Buy GRAB Stock at eToro from just $50 Now!