Gap Stock Down 20% Today – Time to Buy GPS Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Gap stock is down 20% this morning in pre-market stock trading action following the release of the firm’s financial results covering the third quarter of 2021 after the company missed analysts’ estimates for both revenues and earnings amid acute supply chain woes.

For the three months ended on 30 October, the San Francisco-based retailer reported net sales of $3.9 billion resulting in a 1.3% drop compared to the same period a year ago while it missed analysts’ estimates of $4.43 billion for the quarter by a long shot.

Banana Republic sales were the most affected as they declined 18% compared to 2019’s figures – the year before the pandemic – followed by sales of Gap stores, which declined 10% compared to 2019 sales as well.

“Global supply chain disruption, including COVID-related factory closures and continued port congestion, caused significant product delays in the third quarter. Meaningfully reduced inventory positions throughout the quarter negatively impacted sales as brands were unable to fully meet strong consumer demand”, the management stated to explain these disappointing results.

The company estimates that around $300 million in sales were lost as a result of a constrained inventory while air freight costs added around $100 million to its top-line costs during this quarter. As a result, adjusted operating margins suffered during Q3, dropping by 320 basis points compared to the same period in 2019.

Finally, adjusted earnings per share landed at $0.27 compared to $0.53 per share Gap reported in 2019. This figure was significantly lower than Wall Street’s consensus forecast of $0.51 for the period.

For the entire 2021 fiscal year, Gap expects to report a 20% increase in its sales compared to a year ago along with adjusted earnings per share of around $1.25 and $1.40. The firm estimates between $550 to $650 million in lost sales amid the current supply chain woes. These figures indicate a downward revision from Gap’s previous EPS guidance of $2.10 and $2.25 for the period.

This disappointing quarterly report is the reason why Gap stock is dropping this morning. Can today’s decline accelerate the negative momentum that the stock has been experiencing lately? Let’s have a look at the price action and fundamentals of GPS to outline plausible scenarios for the future for this retail stock.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Gap Stock – Technical Analysis

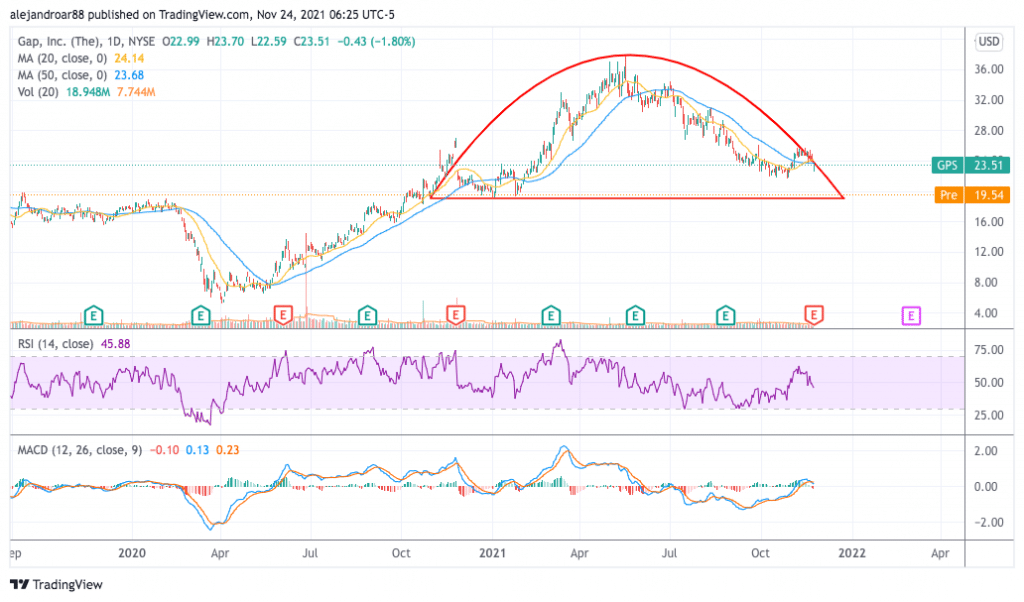

The price of Gap stock was already embarked on a downtrend before today’s downtick as it closed yesterday’s session 38% below its 52-week high of $37.6 per share. On 27 August, the price decisively declined below the 200-day simple moving average following the release of the firm’s Q2 2021 earnings report as Gap started to inform about the impact of these supply chain bottlenecks.

Now, if this morning’s pre-market action spills over to the opening, the price will approach a crucial support area found at the $19 level and would complete a rounding top pattern. This formation is typically considered bearish as it points to a full-blown trend reversal in GPS stock.

Momentum oscillators are also favoring a bearish outlook as the Relative Strength Index (RSI) is standing at 46 – bearish – while the MACD has just crossed below the signal line on the back of the stock’s first negative histogram readings in at least two months.

Overall, the outlook for Gap stock is bearish, especially if the price breaks below the $19 support. However, if that happens, the stock has many horizontal support areas to fall back on and it is highly likely that the extent to which these supply chain woes affect its bottom-line profitability will determine how painful the decline will be in the future.

Gap Stock – Fundamental Analysis

This year was supposed to be a good one for this brick-and-mortar apparel retailer as the pandemic prompted the firm to strengthen its online offering, with digital sales now accounting for over a third of its top-line results.

However, these supply chain woes are depressing the outlook for Gap and its forecasted earnings per share for this year would result in a 29% drop compared to the figure reported during the 2019 fiscal year.

At today’s indicated opening price of $18.7 per share, Gap is being valued at 13 times the upper bound of its forecasted adjusted earnings per share for this year. Meanwhile, if we use the free cash flow figure reported for the nine months ended on 30 October to forecast its annual FCF, the firm would be trading at around 27 times that figure using an estimated post-earnings market cap of $7 billion.

Overall, the valuation for Gap now seems fair considering the challenging environment that the firm is navigating. That said, Gap has some strong brands and the capacity to outperform the market in future years once this supply chain situation becomes an item in the rearview mirror.

Therefore, for patient investors, the current valuation could be considered an opportunity to buy GPS stock at a low price with the expectation that it can deliver decent gains in the next two to three years once these issues are no longer affecting the firm’s performance.

Buy GPS Stock at eToro with 0% Commission Now!