DraftKings Stock Down 22% in February – Time to Buy DKNG Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of DraftKings stock is down nearly 22% so far this month following the release of the company’s earnings report covering the fourth quarter of the 2021 fiscal year as guidance for this year came below Wall Street’s estimates.

For the three months ended on 31 December, the online sports betting company reported total revenues of $473.3 million resulting in a 47% jump compared to the same period a year ago. The consensus estimate for the period stood at $445.7 million.

The number of monthly unique payers (MUP) ended the period 32% higher at 2 million while average revenues per MUP rose 19% compared to the fourth quarter of 2020 at $77.

Meanwhile, the firm’s adjusted EBITDA ended the period at $128 million resulting in a deterioration of the DKNG’s bottom-line profitability compared to the previous year. For the entire 2021 fiscal year, DraftKings’ negative EBITDA rose to $676.1 million compared to $391.9 million the company shed in 2020.

Losses per share for the period ended at $0.35. This figure was markedly lower than the Street’s estimate of $0.63 per share.

DraftKings’ revenue guidance for 2022 came in line with what analysts had forecasted as the company expects to report top-line results ranging from $1.85 to $2 billion compared to the Street’s consensus estimate of $1.9 billion.

However, the firm’s forecasted negative adjusted EBITDA for 2022 was significantly worst than the market anticipated as it is expected to land in a range between $825 and $925 million this year compared to an average forecast of $784.5 million for the period from market participants. DraftKings stated that it expects to report positive adjusted EBITDA for the first time in 2023.

The company’s struggle to swing to profitability is possibly the reason why its shares went down as much as 22% on the day that the earnings report came out. Meanwhile, the stock is diving as much as 14% in pre-market stock trading action this morning.

What could be expected from this gaming stock following the release of this financial report? In this article, I’ll be assessing the price action and fundamentals of DraftKings stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

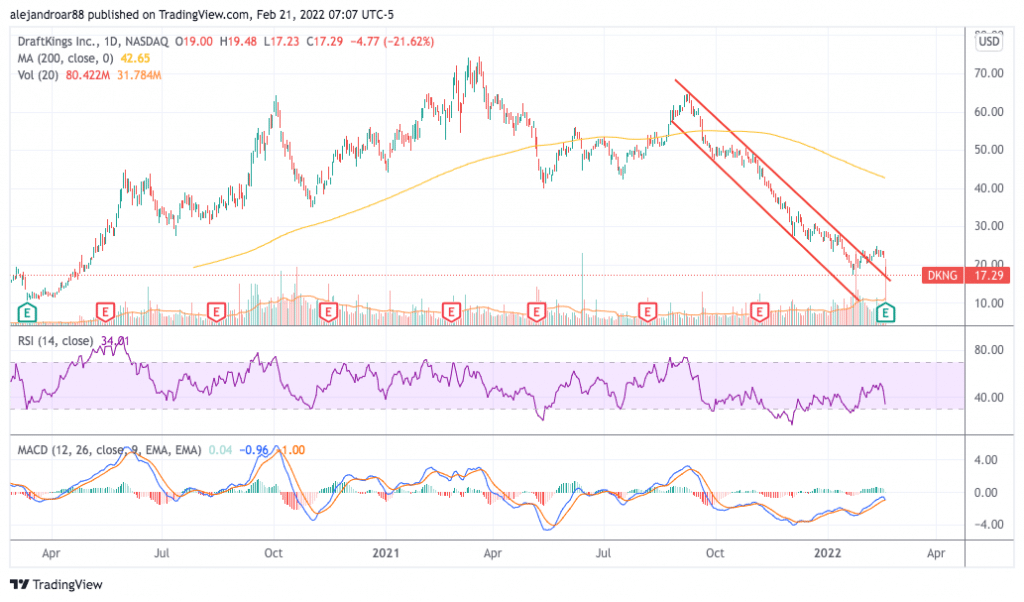

DraftKings Stock – Technical Analysis

In my previous article about DraftKings, I emphasized that the outlook for the stock continued to be bearish since, even though the technical signals were pointing to a deceleration in the negative momentum experienced by the stock recently, those signals were too weak to indicate a change in the direction of the price trend.

Since that article came out, the stock has dived 11% even though the price recovered slightly in the first few days of February.

This recovery led to a break above the descending price channel highlighted in the chart above but last Friday’s downtick pushed DKNG to the upper bound of this formation.

Trading volumes back then exceeded the 10-day average by more than 2 times. This emphasizes the importance of this latest report and its implications on the market’s overall sentiment toward DKNG.

Moving forward, if the price breaks below the upper bound of the price channel chances are that the stock will resume its former downtrend. If that happens, the total downside risk would stand at 38% at least.

DraftKings Stock – Fundamental Analysis

Based on the company’s revenue guidance for 2022, DraftKings will continue to grow its top-line results at a rapid pace, especially if it hits the upper bound of the management’s estimate for the year.

However, profitability remains elusive even on an adjusted basis as the firm’s operating expenses continue to be quite high.

Moreover, stock-based compensation this year nearly doubled. This puts further pressure on the company’s valuation as share count keeps increasing and ends up diluting existing shareholders.

In 2021, DraftKings burned around $520 million in cash or around 40% of its revenues. Considering the overall deterioration of the macro environment that market participants are expecting for this year, it could be difficult for the business to raise more money down the road to remain afloat.

By the end of December, the company had $2.15 billion in cash and equivalents. These reserves should be sufficient to withstand DKNG’s cash burn for at least three years unless the company depletes these reserves faster than expected by acquiring other businesses or making ambitious investments.

Overall, even though DraftKings is growing fast – which is positive – the company’s fundamentals are not as robust as one would like, especially in a potentially tighter macro environment.

As of last Friday, the company’s market capitalization stood at $7 billion resulting in a forward P/S ratio of 3.7x. Even though that multiple seems attractive, the fact that the company is unable to report GAAP profits despite its strong growth increases the risk of further negative volatility in the current scenario.

Buy DKNG Stock at eToro with 0% Commission Now!