Crocs Stock Down 25% In December – Time to Buy CROX Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Crocs stock has gone down nearly 25% so far in December as the rally that followed the release of the firm’s latest earnings report and Investor Day presentation has lost most of its steam.

Meanwhile, the company’s announcement of a $2.5 billion acquisition of the casual footwear company HEYDUDE contributed significantly to this decline as CROX stock dived more than 11% in last Friday’s stock trading activity amid the potentially dilutive effect of the deal.

According to the press release, Crocs will pay $2.05 billion of the transaction in cash while the remaining $450 million will be paid in equity directly to HEYDUDE’s Chief Executive Alessandro Rosano.

The cash used to complete the acquisition will be obtained from a $2 billion term loan and the remaining $50 million from a revolving credit facility. The company expects to settle the deal in the first quarter of 2022.

The valuation given to HEYDUDE represents nearly a third of Crocs’s market capitalization before the announcement was made and the market seems concerned about the fact that the deal will increase the company’s financial leverage significantly.

What can be expected from the manufacturer of one of the world’s most popular flip flops in light of this development? In this article, I’ll be assessing the price action and fundamentals of Crocs stock to outline plausible scenarios for the future.

67% of all retail investor accounts lose money when trading CFDs with this provider.

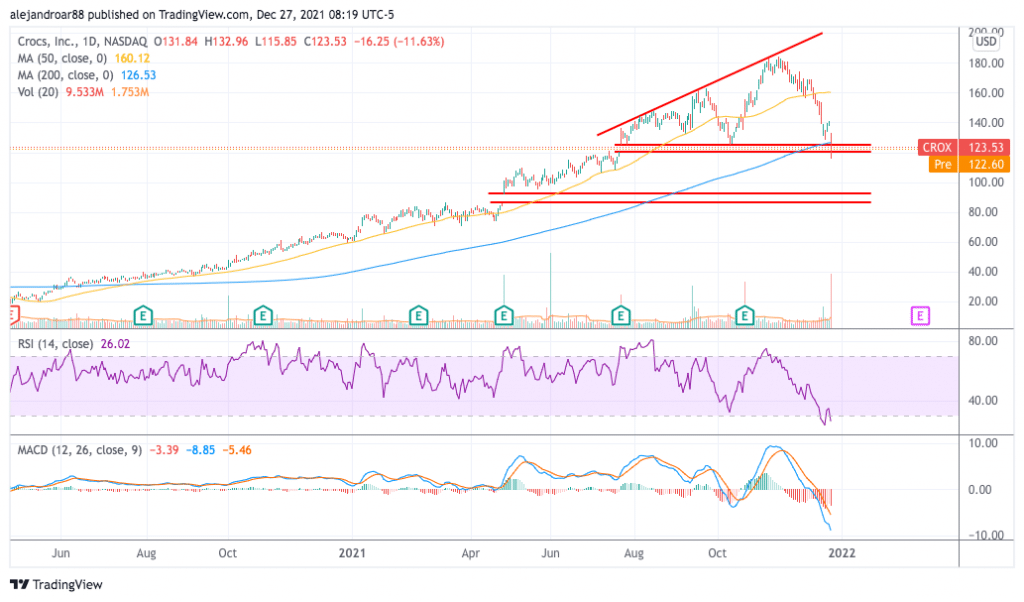

Crocs Stock – Technical Analysis

Back in October when I last wrote about Crocs, I emphasized that there was a possibility that the stock could climb to fresh all-time highs following the release of its quarterly earnings report as positive momentum was picking up.

That prediction turned out to be true as the stock climbed to $180 and it tagged the upper trend line highlighted in the chart. After that, the valuation started to decline as growth stocks as a whole performed negatively both in November and December.

Last Friday’s strong drop led to the closing of the price gap left behind on 22 July and this creates room for further declines if bulls fail to keep the price above the $125 level – another relevant horizontal support.

Meanwhile, the decline also led to a break below the 200-day simple moving average. Such a break had not happened since the pandemic crash of February-March 2020 and it increases the risk of a sustained drop for CROX stock.

Trading volumes were quite high last Friday as more than 9.5 million shares exchanged hands – a figure that exceeded the 10-day average by more than 5 times.

On the other hand, momentum indicators have declined to their lowest levels in months and this typically signals the beginning of a full-blown trend reversal.

All things considered, the outlook for Crocs stock is bearish. Moving forward, the price could continue to drop to the low 100s or even to the low 90s if negative momentum accelerates following the HEYDUDE deal.

Crocs Stock – Fundamental Analysis

The outlook for Crocs would have been positive if it had not been for this HEYDUDE transaction as the company’s fundamentals and prospects were fairly robust.

According to Crocs, HEYDUDE will contribute around $750 million to the firm’s top-line results next year. The strategic reasoning behind the deal is that the company will become a multi-brand platform. This should, in theory, increase Crocs’s total addressable market and multiple synergies may result from the combination of the two companies.

Crocs will take advantage of its well-positioned digital platform and strong network of distributors to promote and sell HEYDUDE footwear from now while the deal is expected to be accretive to the firm’s earnings per share immediately.

According to the management, Crocs is paying a 15 EV/EBITDA multiple on HEYDUDE and the company will, from now on, pause its share repurchases in 2022 to repay a portion of the $2.05 billion in debt it is taking to settle the transaction by using its free cash flows.

Crocs long-term borrowings will climb to $2.69 billion at least after the transaction is settled while assets will stand at around $4.3 billion resulting in an LT-debt-to-assets ratio of at least 60%.

This significant increase in the firm’s leverage ratio is one compelling reason to revaluate the company’s trading multiples moving forward as this increases the firm’s solvency risks in case the business unexpectedly faces a downturn in both its sales and cash-flow generation capacity.

Meanwhile, the $450 million that will be paid in stock to settle the acquisition will dilute existing shareholders by around 6% and that partially explains the decline in the firm’s valuation after the announcement.

Despite the acquisition being accretive to Crocs’s earnings right away, the elevated trading multiple paid for the firm and the strong increase in the company’s financial leverage make this deal bearish in the short to mid-term and until the company proves that the acquisition has been a positive move from a strategic and financial standpoint.

Buy CROX Stock at eToro with 0% Commission Now!