Coinbase Stock Price Down 29% in 2022 – Time to Buy COIN Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

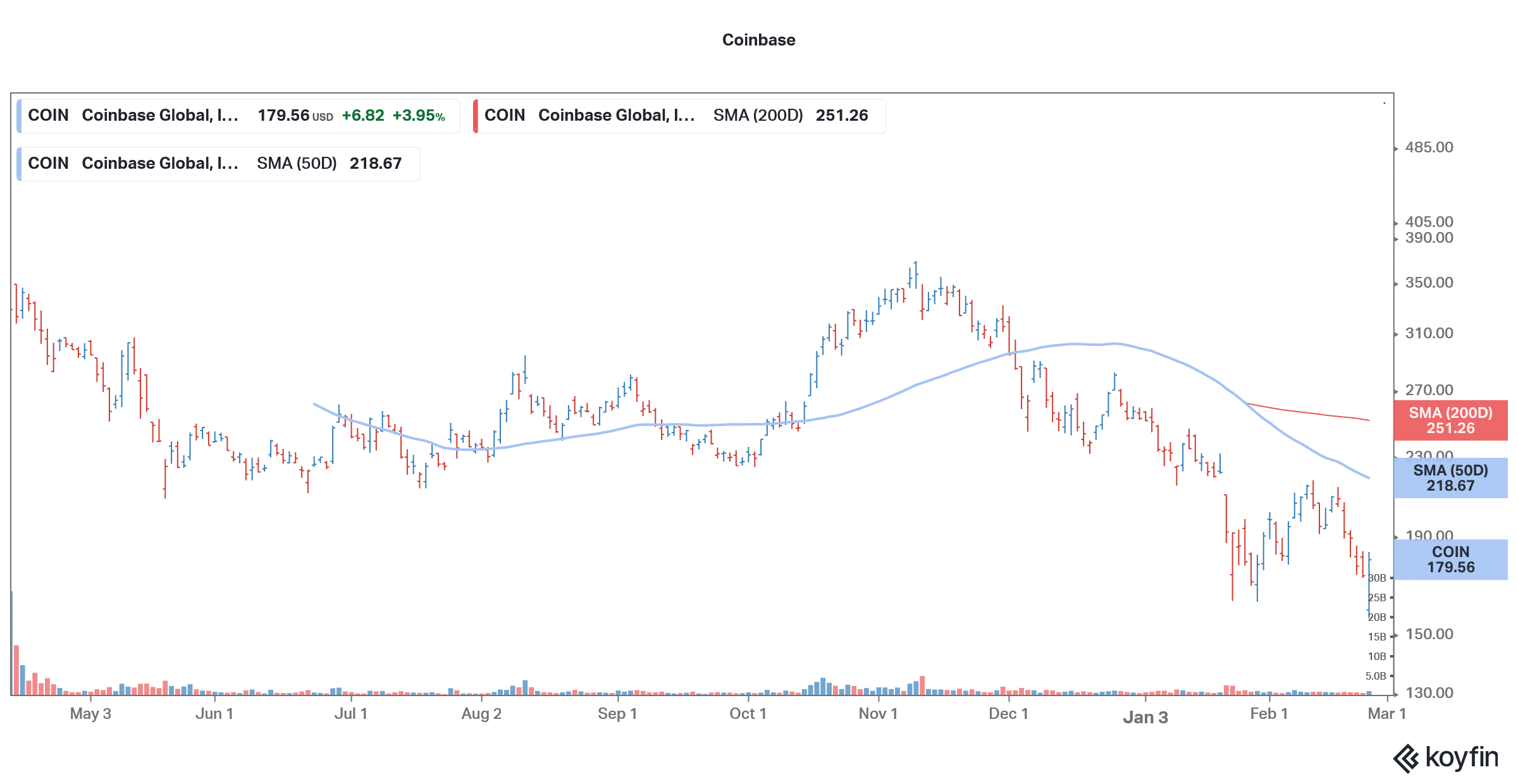

There has been a severe sell-off in fintech stocks and Coinbase (COIN) is down almost 29% in 2022. It hit an all-time low of $155.92 in yesterday’s price action. However, as the broader markets rebounded, COIN stock also reversed the losses and closed the day at $179.56, almost 4% higher than its previous day’s closing.

Other fintech stocks are also having a rough ride and Block, SoFi, and Affirm also hit their 52-week yesterday. Like Coinbase, SoFi and Affirm also went public in 2021 but all these companies choose different ways to go public.

Fintech stocks

Affirm opted for a traditional IPO which it had originally planned for December 2020. However, after the surge in DoorDash and Airbnb stocks on their listing, the company delayed its IPO plans. SoFi opted for a SPAC merger and went public by merging through a SPAC sponsored by Chamath Palihapitiya.

Coinbase went public through a direct listing and kept the reference price at $250. The stock had a bumper listing and went on to hit a 52-week high of $429.54. However, the sell-off in cryptocurrencies took a toll on COIN stock as well, and soon it tumbled below $200. While it eventually recovered the recent sell-off in tech stocks has pushed the stock way below its direct listing prices. What’s the forecast for COIN stock and should you buy it now?

68% of all retail investor accounts lose money when trading CFDs with this provider.

Coinbase reported fourth-quarter earnings

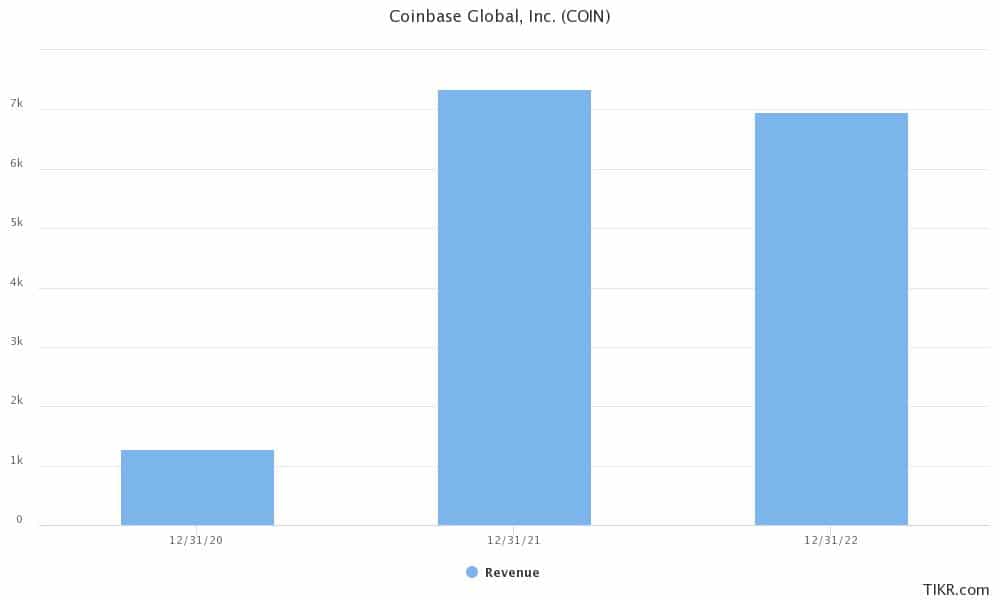

Coinbase reported its fourth-quarter 2021 earnings yesterday after the US markets closed. It reported revenues of $2.49 billion in the quarter. To put that in perspective, it reported net revenues of $1.23 billion in the third quarter and $497 million in the fourth quarter of 2020. The company’s sales were way ahead of the $1.94 billion that analysts were expecting.

Its net income also more than doubled over the third quarter to $840 million. Coinbase reported an adjusted EPS of $3.32 which was again way above the $1.85 that analysts were expecting.

COIN reported stellar numbers in the fourth quarter

Coinbase reported stellar operating results in the quarter. It had 11.4 million MTUs (monthly transacting users) in the quarter while the total traded volume was $547 billion in the quarter. In 2021, its total traded volume jumped to $1.67 trillion which was way above the $193 billion that it reported in 2020. The company had $278 billion worth of assets on the platform at the end of 2021, as compared to $255 billion at the end of the third quarter.

The company’s performance in 2021 was better than what it had guided. For instance, its average annual retail MTUs were 8.4 million in 2021 which was towards the upper end of its range of 8-8.5 million. Similarly, its average transaction revenue per user was $64 while the company had guided for the metric to be in the high $50s.

To sum it up, Coinbase delivered strong earnings in the fourth quarter of 2021. However, the stock was trading lower in US premarket price action. The devil lies in the company’s guidance, which spooked investors.

Coinbase expects results to be lower in the first quarter

Coinbase said that it expects its retail trading volumes and retail MTUs to fall on a sequential basis in the first quarter. It blamed the fall in crypto prices and volatility in the quarter for the expected decline in volumes. However, it said, “This is not unusual, as we have seen historical crypto market patterns where all-time high periods have been followed by softer periods.”

For the full year, 2022, Coinbase provided very wide guidance. It expects annual average retail MTUs to be between 5-15 million. Commenting on the wide range, it said, “This wider than normal set of factors results in a wider range of potential outcomes for 2022. Simply put, we have less near-term visibility, and it is currently too early to provide a more precise range.”

While the company expects the growth in services and subscription revenues to be higher than 2021, it is forecasting a fall in ATRPU (average transaction revenue per user.) Coinbase reported an ATRPU of $64 in 2021 as compared to $45 in 2020 and $34 in 2019. In 2022, COIN expects ATPRU to be pre-2021 levels which would mean a big fall from what it reported in 2021.

Coinbase stock fell as the company warned of uncertainties

Coinbase would join the long list of companies that have provided dismal guidance and their stocks plunged following the earnings release. It said, “We enter 2022 with even more unknowns which make our business all the more difficult to forecast. On one hand, in addition to the unpredictability of crypto asset prices and volatility, we also face global macroeconomic headwinds, rising interest rates, inflation, and more recently, geopolitical instability.”

While it talked about rising participants in crypto markets and increasing adoption of cryptocurrencies as tailwinds, it cautioned about short-term volatility in business. In the past also, Coinbase had called upon investors to take a long-term approach. Meanwhile, COIN CEO Brian Armstrong does not expect that we are headed for a “crypto winter” which is a prolonged bear market in cryptocurrencies.

COIN stock forecast

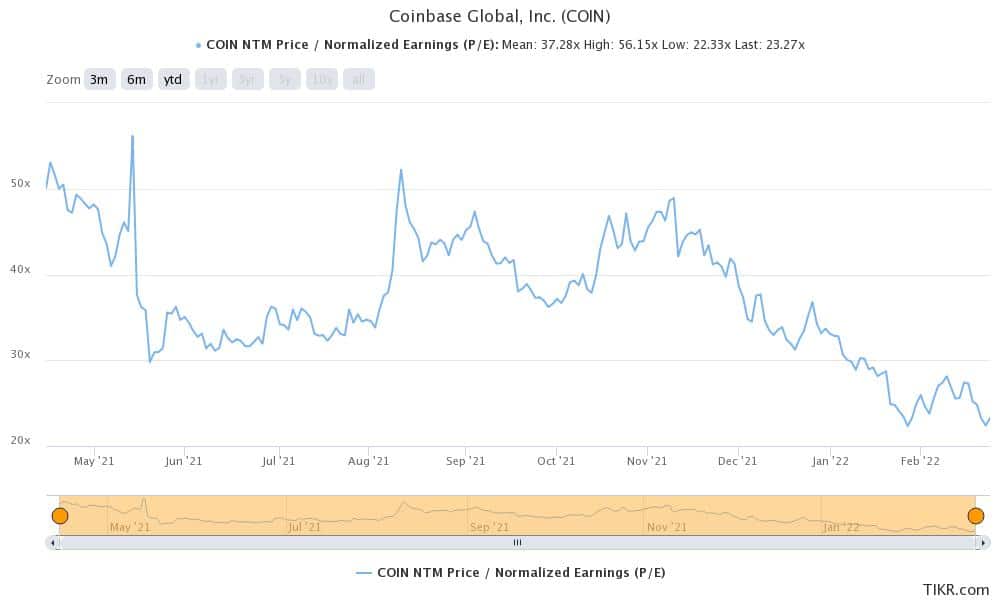

Wall Street analysts have a consensus buy rating on stock. Of the 22 analysts polled by CNN Business, 16 rate the stock as a buy while five rate it as a hold. One analyst has a sell rating in COIN stock.

Its median target price of $322 implies an upside of almost 80% over current prices. Its lowest target price is $220 which is a premium of 22.4% while the highest target price of $600 is a premium of 233% over current prices.

Coinbase stock long term forecast

Over the long term, the higher fees charged by Coinbase are not sustainable. There is bound to be more competition even as the trading volumes are also expected to rise on higher adoption. However, higher engagement on the platform and the addition of new digital assets on the platform will help the company offset some of the revenue loss from lower fees.

Also, revenue diversification measures like NFTs would pay off in the long term. Metaverse could be another long-term revenue driver for Coinbase. The addition of new crypto assets is helping COIN and in the fourth quarter, 68% of its trading volumes were from altcoins.

Should you buy COIN stock?

Coinbase stock has been under pressure amid the broader market crash. The sell-off in cryptocurrencies hasn’t helped matters either for COIN stock. However, if you believe in digital assets and see them as the future, Coinbase is one stock that should find a place in your portfolio.

While there could be heightened volatility in the short term, the stock is a good way to play the expected growth in digital assets.

Buy COIN Stock at eToro from just $50 Now!