Carnival Stock Price Forecast July 2021 – Time to Buy CCL?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Cruise stocks like Carnival Corporation (CCL) have whipsawed over the last year. 2020 was probably the worst year that the industry saw in history as revenues dwindled to almost zero amid the COVID-19 lockdowns. However, cruise line stocks have since rebounded as investors pivoted from growth names to beaten-down cyclical names.

Carnival Corporation stock is now trading only marginally in the green for 2021 and is down over 34% from its 52-week highs. Cruise stocks have come off their 52-week highs even as US stock markets surged to their all-time highs. Investors have been apprehensive of the sector amid the increase in coronavirus cases in the US. What’s the forecast for CCL stock and should you buy it in July 2021?

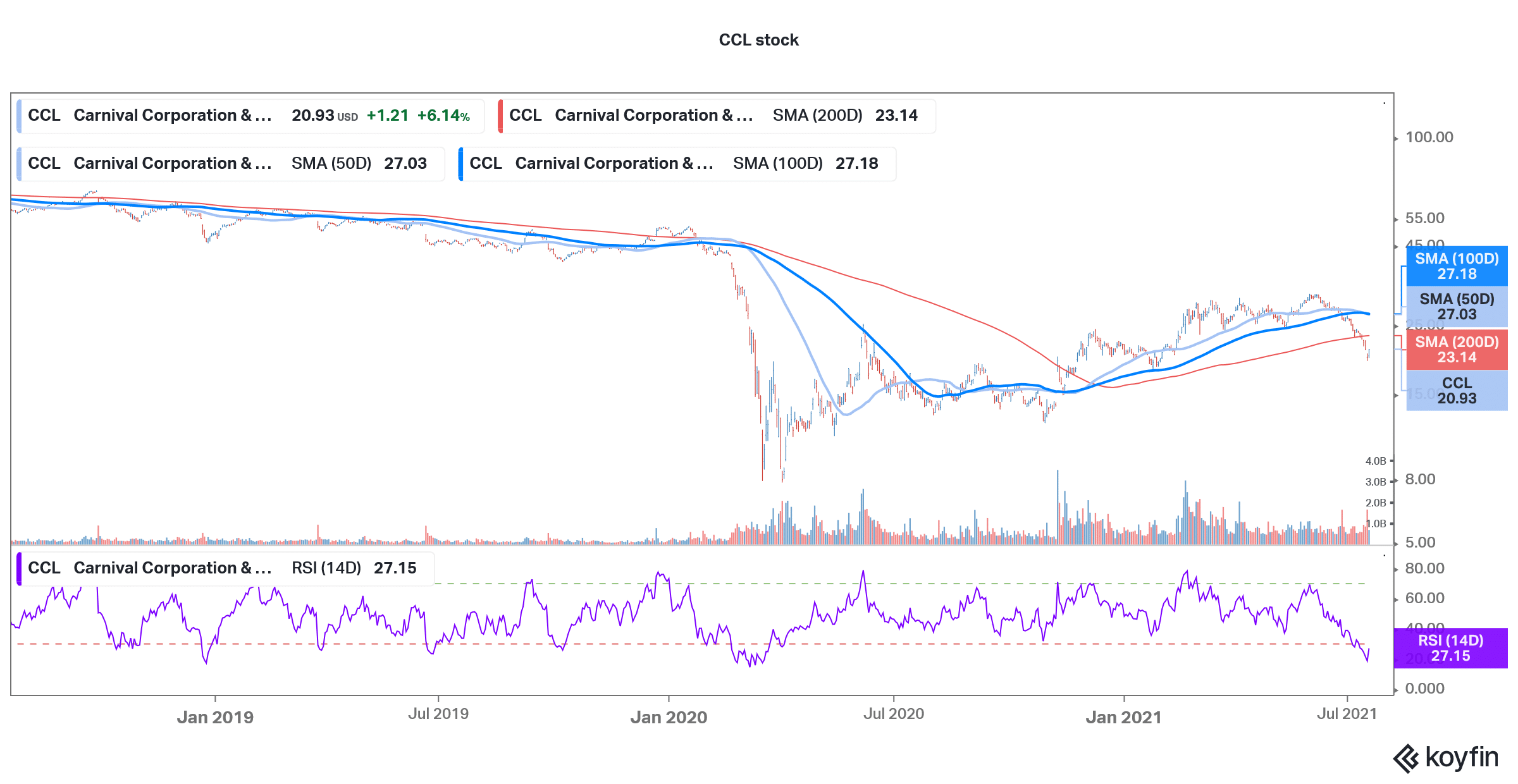

Carnival stock technical analysis

Carnival stock is looking bearish on the charts and it trades below the 50-day, 100-day, and 200-day SMA (simple moving average). The 12,26 MACD (moving average convergence divergence) also gives a sell signal. However, the 14-day RSI of 26.7 shows that the stock is now in an oversold zone.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Recent developments

Carnival stock had tumbled yesterday amid concerns over rising coronavirus cases in the US where the Delta variant has been spreading among the unvaccinated populations. There is still vaccine hesitancy among some sections and the pace of vaccinations in the country has slowed down.

Meanwhile, in a positive development, today CCL announced that it expects to resume operations with 65% of its capacity by the end of this year. “With strong ongoing demand for cruising, we look forward to serving our guests with additional ships announced across eight of our brands and nearly three-quarters of our fleet capacity returning by the end of this year, marking an important milestone for our company and all those who rely on the strong economic impacts generated by the global cruise industry,” said Carnival’s chief communication officer Roger Frizzell.

CCL stock forecast

Meanwhile, Wall Street analysts are divided on Carnival stock and its median target price of $27 implies an upside of 30% over current prices. Its lowest target price is $14.7 which is a discount of over almost 29% while the highest target price of $39 is a premium of 89% over current prices.

Of the 18 analysts polled by CNN Business, five rate CCL stock as a buy while seven rates it as a hold. Six analysts have a sell or equivalent rating on the stock. Earlier this month, Morgan Stanley reiterated its sell rating in carnival stock. “While cruising has recently resumed in the US, our resumption tracker suggests CCL will operate only 18% of its capacity in 3Q21 and 45% in 4Q21, and we model 85% in 1H22 as the company believes it may not be fully operating until spring 2022,” it said in its note. The forecasts are lower than what CCL has now provided.

Wolfe upgraded Carnival stock

Meanwhile, not all brokerages are bearish on cruise line stocks and some see better days ahead. Last month, Wolfe Research upgraded several cruise stocks including Carnival. “Our checks suggest improving booking/pricing trends out of North America over the past month, with stronger trends over the past week. While there is some lingering uncertainty surrounding the U.S. restart (CDC / Florida, etc.), we view those unknowns as largely transitory when viewed against the broader reopening backdrop,” said Wolfe analyst Greg Badishkanian.

Should you buy CCL stock?

CCL stock looks like a good reopening play. There is significant pent-up demand for outdoor entertainment which would help lift the company’s earnings. There are risks like another coronavirus surge taking a toll on the stock. However, the risk-reward dynamics have now started to look favorable for this cruise stock.

67% of all retail investor accounts lose money when trading CFDs with this provider.