Agilon Health Stock Down 12% in July – Time to Buy AGL stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

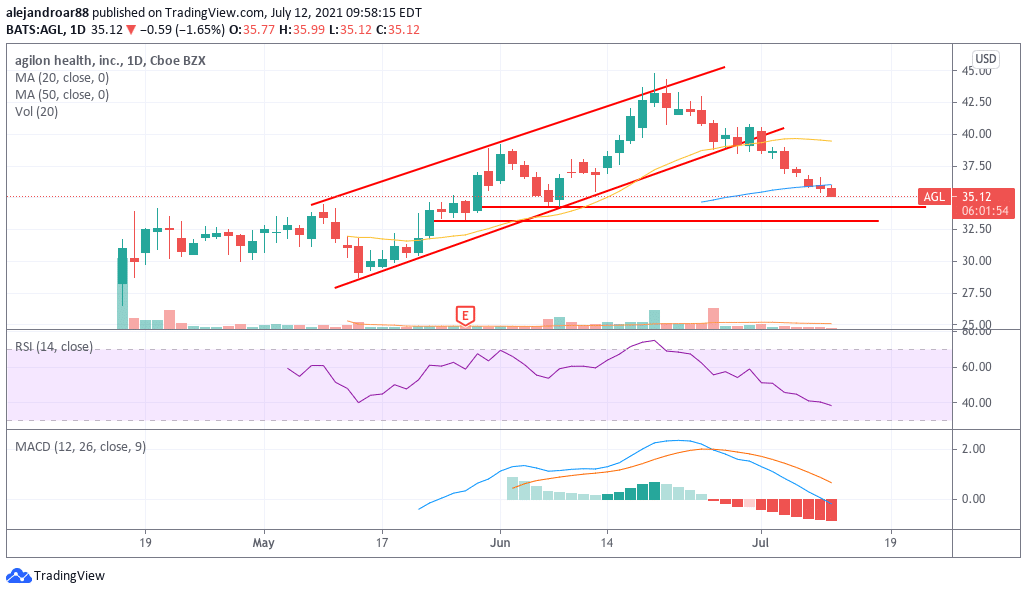

The price of Agilon Health stock has come down 12% so far in July despite the absence of any material events that could affect the financial performance of the company. Meanwhile, the stock is down 1.7% so far this morning at $35.12 while it is posting its fifth consecutive down day.

Could this be a time to buy Agilon Health stock at a point when the market seems to be being overly pessimistic about this healthcare stock? The following article takes a closer look at the fundamentals of the business to possibly answer that question.

Agilon Health – technical analysis

With a little less than three months trading since the company went public, the price action for Agilon Health stock seems lengthy enough to provide indications of where the stock might be heading in the near future.

In this regard, the chart shows that the stock has broken below a rising price channel that started to form a couple of weeks after Agilon’s initial public offering (IPO). Interestingly, the downtrend appears to have started only a few days after the company participated in Goldman Sachs’ Annual Global Health Conference.

The price seems to be temporarily bouncing off the $35.5 support area but this threshold is not particularly strong as it has only been tagged one time in the past. If the downtrend continues in the following sessions, the next area of support to watch would be found around the $34 level 3% downside risk still on the horizon.

Due to the stock’s limited price action, fundamentals are likely playing a more important role in determining the price than technical patterns.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Agilon Health – fundamental analysis

Agilon Health is a California-based company that seeks to optimize the way health care is administered in the United States. Despite the company showing an impressive CAGR in its sales in the past few years, the numbers show that both sales and memberships have actually been slowing down.

For Agilon, enrolling more doctors for its network is crucial as that is how they attract more revenue toward the business. According to the firm’s historical performance, membership growth has grown at a slower lately, moving from a 97% jump in 2018 to a 46% advance last year.

Meanwhile, during the first quarter of 2021, total memberships expanded by only 35%, ending the three months with a total of 165,300 physicians currently enrolled.

Moreover, the company is forecasting total memberships of 184,000 for its 2021 fiscal year along with revenues of $1.78 billion. If those targets are met, memberships would be reporting their third consecutive year of slower growth and the same thing can be said for Agilon’s sales.

During the first quarter of 2021, gross margins stood at 7%. Agilon’s top-line margins are particularly important as the firm’s bottom-line profitability depends on the company’s ability to raise those margins as much as possible.

Compared to its historical performance, first-quarter margins came in at the high end of the market’s expectations. Moreover, platform supporting costs and administrative costs as a percentage of sales dropped slightly, which was also positive.

As for its solvency, by the end of the first quarter, Agilon had long-term debt of approximately $180 million on assets of $574 million that included $105 million in cash. During this period, the firm raised $100 million and repaid around $70 million in long-term debt. Meanwhile, its cash burn during these three months was almost $50 million, which is quite elevated.

The rate at which Agilon is burning cash is a bit concerning and it is highly likely that the company will have to raise more money soon to increase its reserves.

Meanwhile, at its current market capitalization of $14 billion, the firm seems to be being valued at almost 8 times its forecasted sales for 2021 as per the management’s guidance. This number seems particularly stretched based on the company’s declining revenue and membership growth.

To date, Agilon hasn’t been able to prove that its business model can deliver the kind of growth and top-line profitability that would allow it to deliver positive returns for shareholders in the long run.

Administrative and platform supporting costs remain above the firm’s gross margins and there have been no signs about the possibility of that situation turning around for the benefit of shareholders.

Buy Stocks at eToro, the World’s #1 trading platform!