5 Best Healthcare Stocks to Buy in July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The pandemic has provided what could be a long-term tailwind for companies in the healthcare sector and especially to those that develop systems, technologies, and treatments that are somehow connected to the COVID-19 virus.

To help you in navigating the vast universe of stocks that you can pick from in this large sector, the following article shares a selection of the 5 best healthcare stocks to invest in July 2021 based on an analysis of their fundamentals, growth prospects, and technical setups.

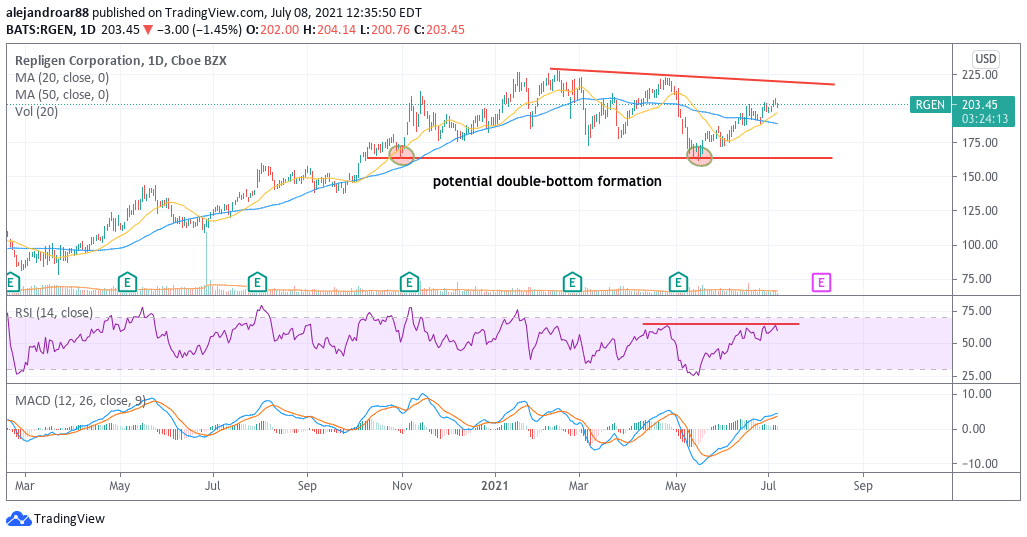

1. Repligen Corporation (RGEN)

Repligen is a Massachusetts-based company that develops systems that enable drugmakers to improve their manufacturing processes. The firm divides its revenue segments into four: filtration, chromatography, process analytics, and proteins, with most of its revenues coming from North American and European customers.

Filtration products account for roughly half of the firm’s revenues and top-line results for this segment have doubled since 2018, with sales landing at $175 million last year. Meanwhile, the firm’s process analysis segment has also doubled from 2019 to 2020 and it now accounts for 9% of Repligen’s total revenues.

Since 2018, revenues for Repligen have nearly doubled from $193.9 million to $367 million while net income during the same period rose from $16.6 million to $59.9 million.

By the end of the first quarter of 2021, the firm had $30 million in long-term debt while it held $711 million in cash and equivalents.

Sales for 2021 based on the management’s forecasts are expected to land at $590 million while net income is expected to come in at around $100 million. At a market capitalization of $10.5 billion excluding cash, this would result in a forward P/E ratio of 105.

Even though this ratio seems high, it is important to note that if the management hits that $100 million net income target, the firm’s earnings growth rate will land at around 66% while last year’s net income rose by as much as 180%.

Based on these forecasts, the current valuation for Repligen seems attractive for a company that is experiencing what could be a long-lasting tailwind resulting from the pandemic as more providers are now aware of the company’s products and solutions to ramp up their manufacturing capabilities.

67% of all retail investor accounts lose money when trading CFDs with this provider.

2. Seagen (SGEN)

Seagen swung to profits last year amid a significant surge in the firm’s collaboration revenues. This uptick came primarily from a licensing agreement the firm signed with Merck that produced approximately $975 million for the company.

As a result, the Washington-based biotech company saw its total revenues jump to $2.18 billion – more than doubling its top-line results compared to the previous year while its net income landed at $614 million.

However, Seagen expects that revenues coming from collaborations with other companies should decrease this year, with top-line results possibly landing at around $1.50 billion according to analysts’ estimates compiled by Koyfin.

By the end of the first quarter of 2021, Seagen had less than $200 million in long-term debt while it held around $2.5 billion in cash and equivalents.

Analysts are not expecting that the firm will be able to turn another profit this year but they do see Seagen producing around $2.96 per share in earnings by 2023, which results in a forward P/E ratio of 49. Moreover, the firm’s forward P/S ratio based on this year’s estimate sales is currently standing at 17.

Although these valuation metrics seem fairly elevated based on the company’s historical performance, Seagen’s ability to land this latest lucrative deal with Merck shows the underlying potential of the company and investors should keep an eye on further developments that could have a long-term impact on the business’ financials.

Based on those prospects, Seagen would be an attractive biotech stock if the price moves down to the low 100s.

67% of all retail investor accounts lose money when trading CFDs with this provider.

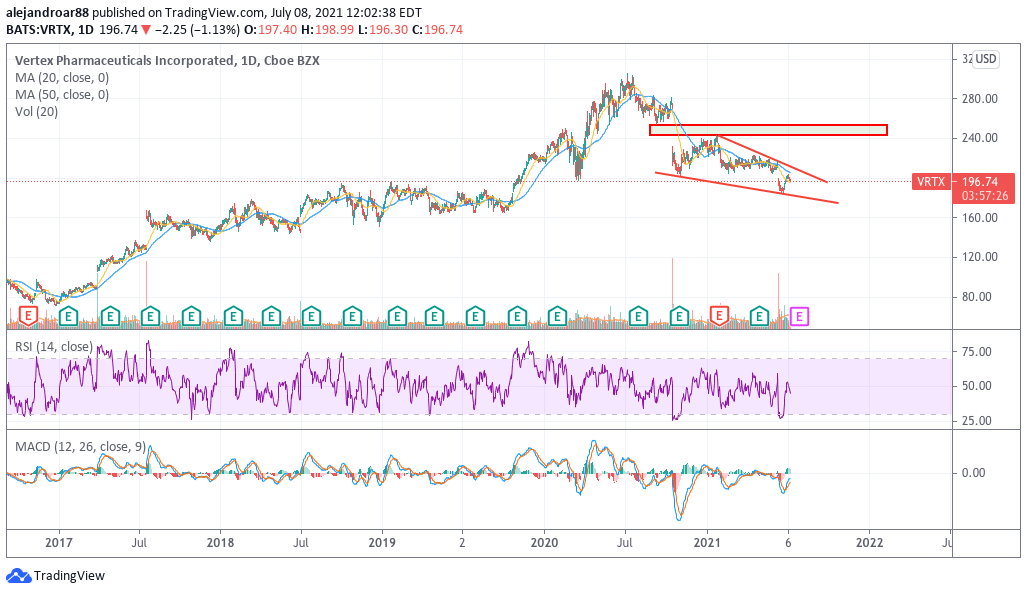

3. Vertex Pharmaceuticals (VRTX)

The price of Vertex stock declined 20% in a single day in mid-October last year after a promising drug in the company’s pipeline was discontinued. This downtick appears to have opened an opportunity to invest in the company at a relatively conservative valuation based on the firm’s historical performance.

Vertex Pharmaceuticals specializes in the development of treatments for cystic fibrosis. In the past three years, the firm has been able to grow its sales from $2.5 billion in 2017 to $6.2 billion by the end of 2020.

Last year, more than 60% of Vertex’s sales came from the commercialization of TRIKAFTA/KAFTRIO, a promising drug that treats cystic fibrosis. The drug was approved for use in children by the US Food and Drug Administration (FDA) in June this year while it had already been approved for use in adults in October 2019.

Analysts are currently estimating that sales for Vertex should land at around $7 billion this year even though TRIKAFTA/KAFTRIO sales landed at $1.7 billion during the first quarter of this year already, which could result in nearly $6.8 billion in annual sales coming from that drug alone using a simple run rate of current results.

Meanwhile, the company has ramped up its net income from $263 million in 2016 to $2.7 billion last year while it doubled its bottom-line results from 2019 to 2020.

Based on the current $51.8 billion market capitalization of Vertex, which includes a total of $6.9 billion in cash reserves, and the market’s overly pessimistic sales estimates for the year, net income for Vertex could land at around $3 billion this year. That would result in an 11% jump this year on a forward P/E ratio of 15.

This ratio points to Vertex as a possibly undervalued stock based on the growth prospects of its TRIKAFTA/KAFTRIO treatment, which don’t appear to be fully priced into the company’s current valuation.

67% of all retail investor accounts lose money when trading CFDs with this provider.

4. PerkinElmer (PKI)

PerkinElmer is a specialized healthcare company that assists drug developers to enhance their R&D processes while also developing solutions for diagnostics. The firm generates revenues from two segments: Discovery and Analytics and Diagnostics. The two segments account for a similar share of the firm’s top-line results.

By the end of last year, PerkinElmer generated sales of $3.4 billion for a 31.2% jump compared to a year ago as the demand for its services rose during the pandemic. Meanwhile, net income landed at $728 million for a 220% jump compared to a year ago.

Long-term debt by the end of the first quarter of the year landed at $3.4 billion on assets of $8.7 billion that include $5.2 billion in intangibles and goodwill and cash and equivalents of $1 billion.

For 2021, analysts are estimating a 16.4% jump in PKI sales, with top-line results possibly landing at $4.4 billion. This results in a forward P/S ratio of 4. Meanwhile, net earnings should land at around $500 million by the end of the year, which results in a forward P/E ratio of 35.

This P/E ratio is not necessarily unattractive as PKI’s net income is expected to remain at least two to three times above its pre-pandemic earnings for the foreseeable future and the company should be able to justify this valuation by producing a more stable growth rate once the virus crisis is over.

67% of all retail investor accounts lose money when trading CFDs with this provider.

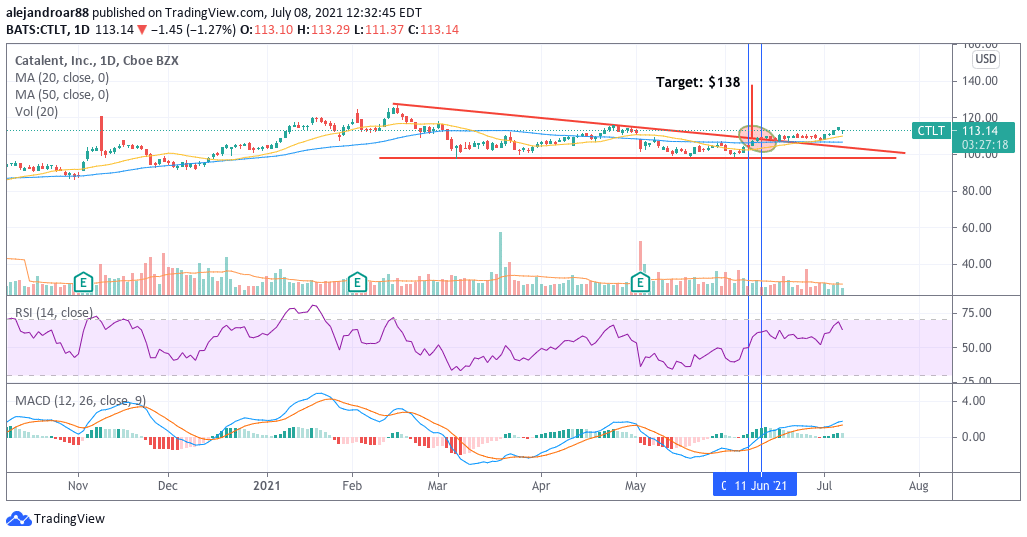

5. Catalent Inc (CTLT) – the technical pick

Catalent has managed to nearly triple its net income from $83.6 million in 2018 to $220.7 million by the end of 2020 while the firm is being valued at 32.5 times its estimated earnings per share for the next twelve months.

The latest price action seen by Catalent shows that the stock has reversed its latest downtrend after breaking above a descending triangle during two consecutive high-volume sessions. This break results in a short-term price target of $138 for CTLT stock for a potential 22% gain based on the triangle’s height.

Reinforcing this outlook, the stock’s short-term moving averages have just posted a golden cross while the RSI has moved near overbought levels for the first time since February this year – further indicating a potential reversal of the stock’s former downtrend.

Buy Stocks at eToro, the World’s #1 trading platform!