Affirm Stock Price Down 42% in 2022 – Time to Buy AFRM Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

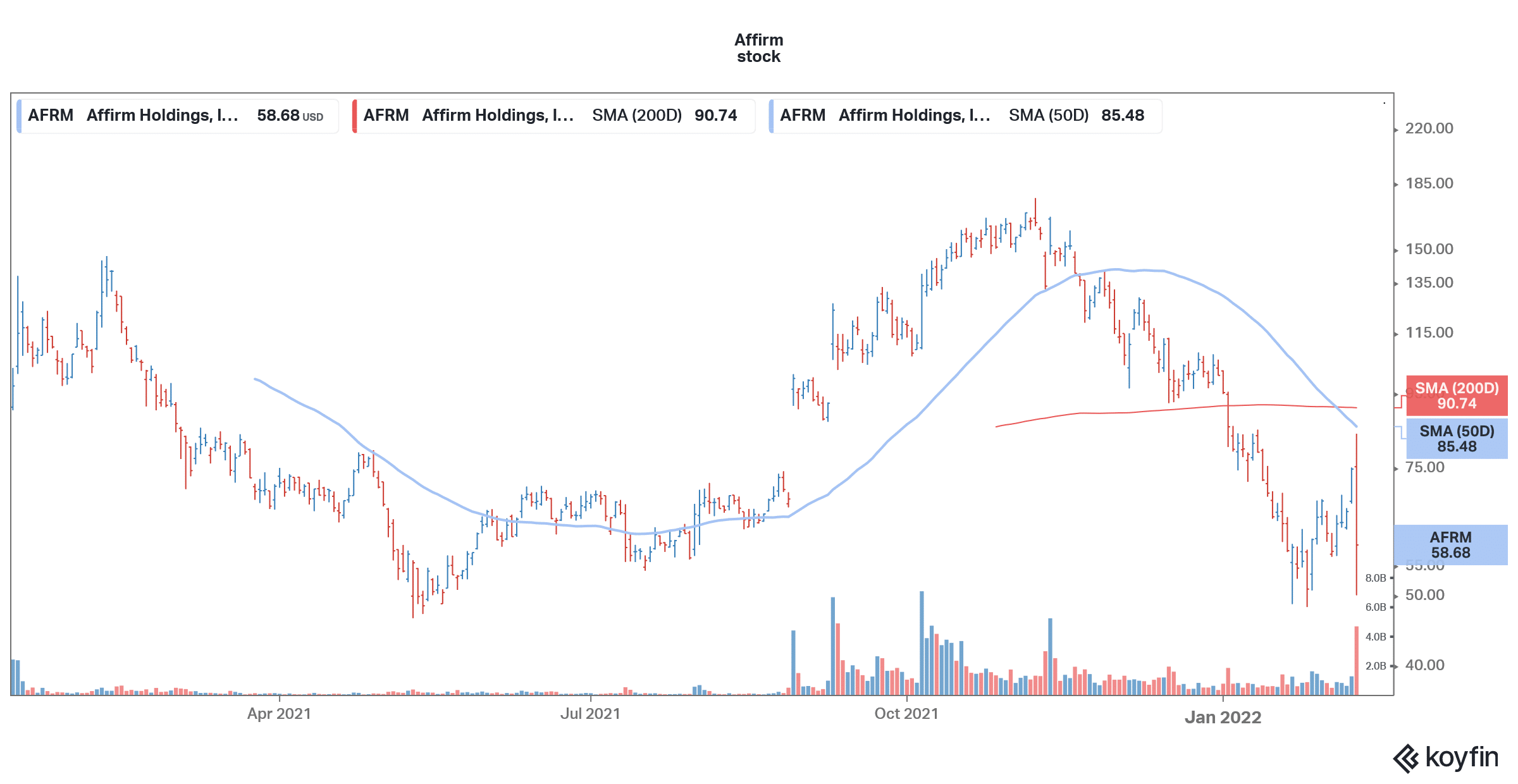

Affirm (AFRM) stock fell 21% yesterday and was down almost 10% in US premarket price action today as well. Till yesterday, the stock is down 42% in 2022 and is among the worst-performing stocks of the year.

While Affirm stock was quite volatile in 2021 it eventually gained almost 105% in the year. What’s the forecast for the stock and should you buy the dip?

Affirm is a BNPL company

Affirm is a BNPL (buy-now-pay-later) company. The industry has been attracting a lot of interest from financial as well as tech companies. Last year, AFRM announced a partnership with Amazon under which buyers on the platform would be able to able to pay using Affirm’s flexible payment options. To begin with, the optionality would be available for a few Amazon customers only but would be eventually Amazon plans to offer the option to a broad range of customers.

The BNPL space saw a lot of action last year. While Apple was rumored to enter the industry, Square, which is now known as Block, went ahead and acquired Australian BNPL company Afterpay. The deal was at a massive premium and signaled the massive appetite for BNPL companies.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Fintech stocks have been under pressure

Meanwhile, fintech stocks have been under pressure amid the fall in growth names. Apart from Affirm, SoFi, Paysafe, and PayPal have also seen a selling spree and continue to trade close to their 52-week lows.

Affirm stock recent developments

Affirm mistakenly released its fiscal second-quarter 2022 earnings yesterday within market hours. It posted revenues of $361 million in the quarter, which were ahead of the $329 million that analysts were expecting. Affirm’s revenues increased 77% YoY in the quarter, which looks encouraging.

The company’s GMV (gross merchandise value) increased 115% and reached $4.5 billion. While the company also benefited from the Amazon partnership, its GMV doubled during the quarter even after excluding the Amazon partnership. Active merchants on the company’s platform increased from 8,000 to 168,000 over the period.

The company’s active consumers increased 150% to 11.2 million over the period. The transactions per active user increased 15% to 2.5 at the end of 2021.

AFRM missed earnings estimates

Affirm posted an adjusted operating loss of $7.9 million in the quarter as compared to an adjusted operating profit of $3.1 million in the corresponding quarter last year. Its adjusted loss per share of $0.57 was also higher than the $0.37 that analysts were expecting.

Along with missing analysts’ estimates for the bottomline, Affirm also gave dismal guidance. It expects to post revenues between $325 to $335 million in the fiscal third quarter, which was below the $335 million that analysts were expecting.

In the full fiscal year, the company expects to post revenues between $1.29-$1.3 billion while it’s forecasting a GMV of $14.58-$14.78 billion. It expects to post an adjusted operating loss margin of 19-21% in the fiscal third quarter while the full-year loss margin is expected between 12-14%.

Management is optimistic after the results

Affirm’s management sounded bullish on the results. The company’s CEO Max Levchin said in his prepared remarks “Affirm’s strong growth accelerated this quarter, reflecting the key advantages of our superior technology, and commitment to putting people first.’ He added, “We more than doubled gross merchandise volume year over year. Over the last 12 months, we have added nearly seven million active consumers to our network, while enabling 168,000 merchant partners to better serve their customers.”

Affirm-Amazon deal

Affirm’s earnings and guidance reflect that the deal with Amazon is perhaps not as big a game-changer as markets were expecting. Notably, AFRM stock had skyrocketed when it had announced its partnership with Amazon last year. However, the incremental revenues from the partnership seem quite low than what was expected.

Jefferies downgrades AFRM stock

After Affirm’s earnings release, Jefferies, which anyways had a hold rating on the stock, downgraded it to underperform and lowered the target price by $10 to $45. “Credit normalization is likely to lead to increased losses/provisions, while rising interest rates will hurt AFRM’s GOS (gain on sale) margins, as well as increase funding costs. While this has been expected and is within guidance, these factors likely represent a LT headwind, rather than a transitional headwind, on the margins of this platform,” said Jefferies analyst John Hecht in his note.

Hecht does not see many catalysts that could take the stock higher. He added, “Given our expectations for [continued] good revenue growth along with declining margins, we find it difficult to determine what will be attributed to incremental, positive trends (in part given rising rates and losses) and thus find it hard to identify an emerging catalyst.”

Weak macro environment

Affirm’s earnings miss is coming at a time when market sentiments towards growth names are already quite negative. The fintech space has been under severe stress and investors have even sold out of profitable and established names like PayPal and Block. Signs of a growth slowdown are visible in the industry and markets are repricing the shares.

Affirm stock forecast

Meanwhile, Wall Street analysts have split ratings on Affirm stock. Of the 14 analysts polled by CNN Business, eight rate AFRM stock as a buy while five rate it as a hold. Only one analyst has a sell or equivalent rating on the stock.

AFRM has a median target price of $91.50, which implies an upside of 56% over current prices. Its lowest target price is $45 which is a discount of over 23% while the highest target price of $140 is a premium of 139% over current prices.

Like Jefferies, expect more analysts to downwardly revise their target prices on Affirm stock after the earnings release.

Should you buy AFRM stock?

Loss-making growth names have been out of favor with markets and Affirm is no exception. The stock trades at an NTM (next-12 months) EV-to-sales multiple of 12.3x. While such multiples looked attractive a few months back, markets are now wary of such valuations amid the rising bond yields.

While AFRM still remains a good long-term story, it could see heightened volatility in the short term amid the rising bond yields.

Buy AFRM Stock at eToro from just $50 Now!