5 Best REIT Stocks to Buy in July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Real estate investment trusts (REITs) are vehicles through which investors can get exposure to different types of properties including health care, commercial, and specialized facilities.

REITs can deliver returns for investors in two ways. They can produce a stream of fixed income through dividend payments and they can also generate capital gains if the price of the REIT increases.

The following is a selection of 5 top REITs to buy in July that offer both an attractive dividend yield and the possibility of further price increases as the US economy continues to bounce back from the pandemic downturn.

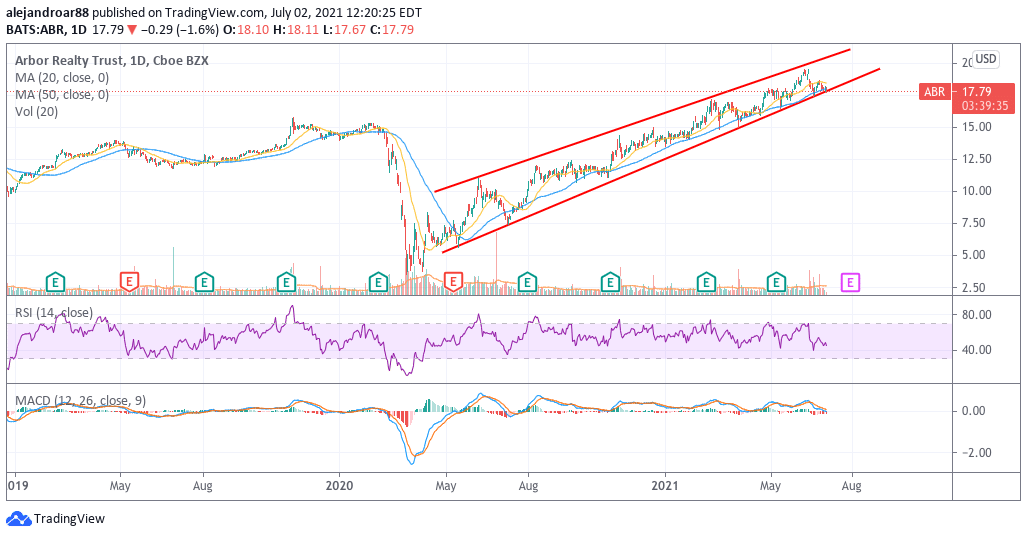

1. Arbor Realty Trust (ABR)

Dividend yield: 7.7%

Arbor is a real estate lending company – also known as a mortgage REIT – that provides financing for multifamily and single-family properties along with selected commercial deals. The company is based in New York and employs around 500 people.

More than half of the firm’s revenues come from interest income but Arbor also earns money from fee-based services and mortgage servicing. From 2015 to 2020, this REIT managed to grow its revenues from $88.4 million to $426.7 million at a compounded annual growth rate (CAGR) of 37%.

Meanwhile, during the same period, profitability has jumped from $53.4 million to $196.2 million while the company offers an appealing 7.7% dividend yield at the moment.

This dividend seems fairly sustainable based on the firm’s ability to produce cash from its operations. However, dividend coverage ratios have been hovering too close to 1, which means that investors should keep a close eye on how Arbor’s financial performance evolves moving forward to make sure that the dividend is not at risk. The company has been growing its dividend at an 8% CAGR since 2014, moving from $0.78 back then to $1.23 per share last year.

Data from Koyfin shows that analysts expect to see Arbor’s earnings per share landing at around $1.6 and $1.8 per share, which means that the payout ratio is fairly conservative to support the continuation of dividend payments in the near future.

Meanwhile, so far this year, Arbor accumulates a 30% gain while last year it delivered a 10% gain on top of its dividend payments.

67% of all retail investor accounts lose money when trading CFDs with this provider.

2. National Wealth Investors (NHI)

Dividend yield: 6.6%

NWI is a REIT that specializes in administering health care facilities including assisted living, hospital properties, and medical offices. The company’s stability is perhaps the most appealing characteristic of this REIT with revenues growing at an attractive CAGR of 16.5% for the past 9 years, moving from $83.7 million in 2011 to $329.7 million last year.

Profitability has also remained fairly stable during this period, moving from $81.1 million back in 2011 to $185.1 million with net margins ranging from 50% to 60% in the past five years. Meanwhile, NHI’s long-term debt stood at $1.52 billion by the end of last year on assets of $3.18 billion.

Although payout ratios have surged above 100%in the past three years, the company’s dividend coverage ratio has stood above 1 in the past five years, which reinforces a stable short-term outlook for this REIT’s attractive yield of 6.6%.

67% of all retail investor accounts lose money when trading CFDs with this provider.

3. City Office REIT Inc (CIO)

Dividend yield: 4.7%

The City Office REIT invests primarily in commercial buildings located in 18-hour cities in the Southern and Western regions of the United States, currently owning properties in Texas, Arizona, Washington, California, and other nearby states.

The market capitalization of this REIT currently stands at $541 million and the company is based in Dallas, Texas. Although revenue growth decelerated last year amid the pandemic, the City Office REIT managed to grow its revenues from $9.1 million in 2011 to $156.3 million by the end of 2019 before the virus situation started, resulting in a compounded annual growth rate of 42.7%.

The company’s profitability has been a bit choppy since 2017 – when it started reporting positive net earnings. Since then, profits have ranged from $2 to $6 million. However, operating cash flows have grown steadily, moving from $1.1 million in 2011 to $60 million last year.

Dividend coverage ratios for City Office are decent, landing at 1.5 last year. Despite the fact that the dividend was slashed last year from $0.94 to $0.60, the current yield remains fairly attractive and sustainable – especially now that the economy is recovering progressively from the hit it took last year.

67% of all retail investor accounts lose money when trading CFDs with this provider.

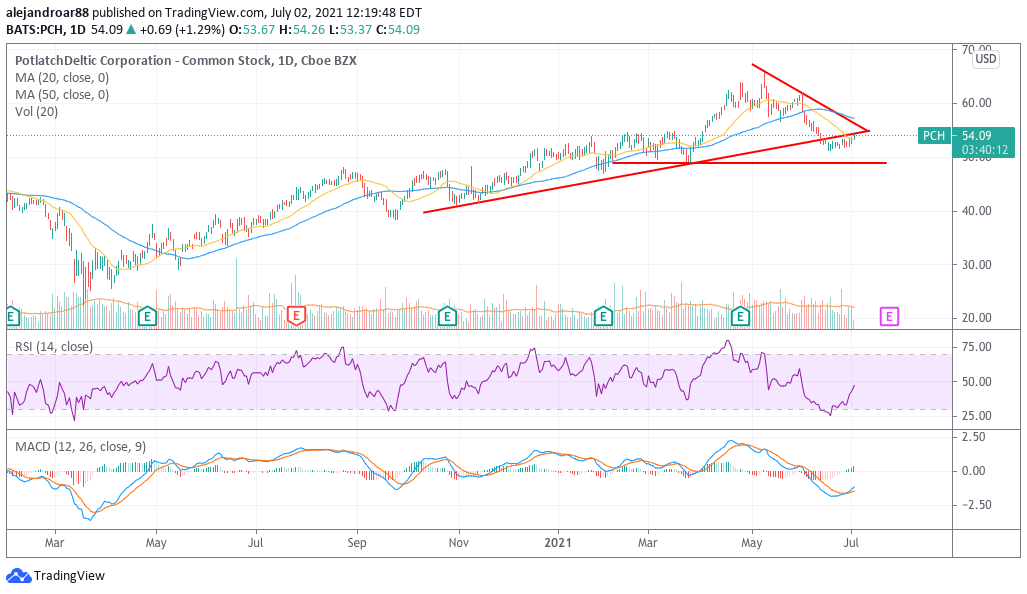

4. PotlatchDeltic Corporation (PCH)

Dividend yield: 3.0%

Even though the price of lumber has collapsed from its 2021 highs lately, PotlatchDeltic had been generating solid revenue growth for years long before prices surged the way they did this year.

The company’s revenues started to jump rapidly from 2016, moving from $575.3 million back then to as much as $1.04 billion last year for a compounded annual growth rate of almost 16% as the demand for lumber has skyrocketed.

Meanwhile, net earnings have jumped from $11 million back then to $166.8 million last year while cash from operations has grown consistently from $102.1 million to $335.3 million during the same period.

The company’s historical dividend coverage ratios are quite good, ranging from 1.5 to 3 times in some cases. However, dividends have stood nearly the same since 2019 as the company decided to maintain its distributions unchanged amid the uncertainty caused by the pandemic.

Based on the firm’s historical coverage ratios, chances are that the management could ramp up the annual dividend this year once all the virus-related uncertainty fades.

67% of all retail investor accounts lose money when trading CFDs with this provider.

5. EPR Properties (EPR)

Dividend yield: 0%

EPR’s revenues were heavily battered last year amid the company’s exposure to the most virus-battered sectors of the economy. ERP’s portfolio of properties includes 178 theaters, including a significant portion leased to AMC Entertainment, and 55 eat & play properties, among many others.

Now that most physical locations in the United States are fully reopened, it could be expected that EPR’s performance in the near future should progressively improve. Meanwhile, one of EPR’s biggest tenants is AMC Entertainment, a company that has greatly benefited from the latest meme stock frenzy by successfully raising billions in capital to survive the virus downturn.

AMC seems to be much better positioned now to keep paying rent to EPR while many other properties held by this REIT should start to perform better once the virus situation becomes an item in the rearview mirror.

As for its solvency, EPR’s balance sheet is conservatively financed, with its long-term debt currently standing at around $3.4 billion on total assets of $6.2 billion. Meanwhile, the firm held $538 million in cash by the end of the first quarter of 2021.

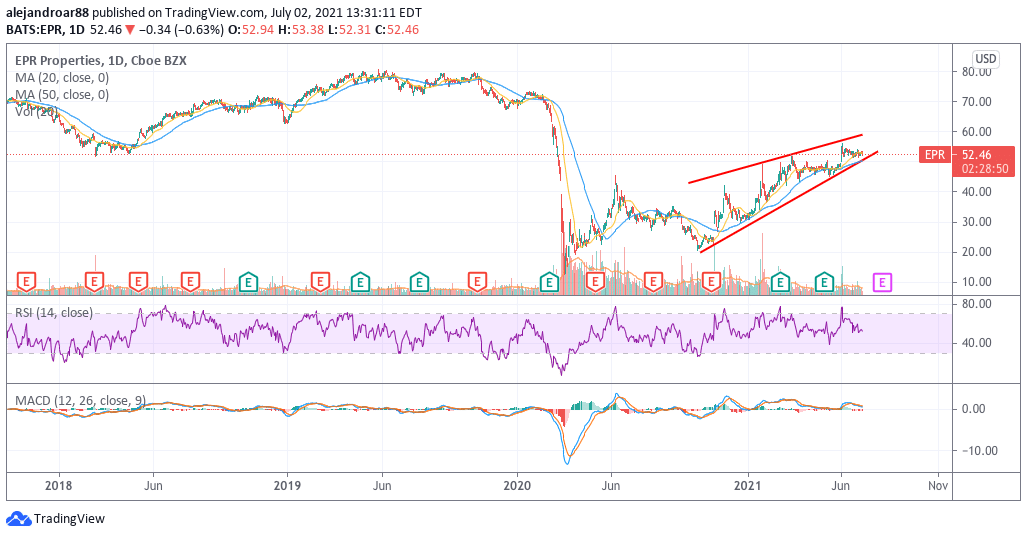

As reflected in the chart above, the upside potential for EPR is quite promising as the REIT could return to its pre-pandemic levels once the economy fully recovers.

Buy REIT Stocks at eToro, the World’s leading Trading Platform