5 Best Energy Stocks in July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The latest deal reached by members of the Organization of Petroleum Exporting Countries (OPEC) and its allies has debilitated oil’s latest rally as the cartel has already agreed to ramp up its crude output in the following months to partially reverse the cuts made last year at the onset of the pandemic.

As a result, the price of multiple energy stocks, particularly those in the oil & gas segment, has suffered a setback in July as reflected by the performance of the SPDR Select Sector ETF (XLE), which has retreated more than 9% amid its strong concentration in oil companies.

In this now seemingly unfavorable environment, energy stocks with robust balance sheets, appealing dividends, and strong pre-pandemic top and bottom-line growth are trading at even more attractive valuation multiples.

To help you in identifying the best candidates for taking a long position in this virus-battered sector, the following article lists five names that you may want to consider in July 2021.

67% of all retail investor accounts lose money when trading CFDs with this provider.

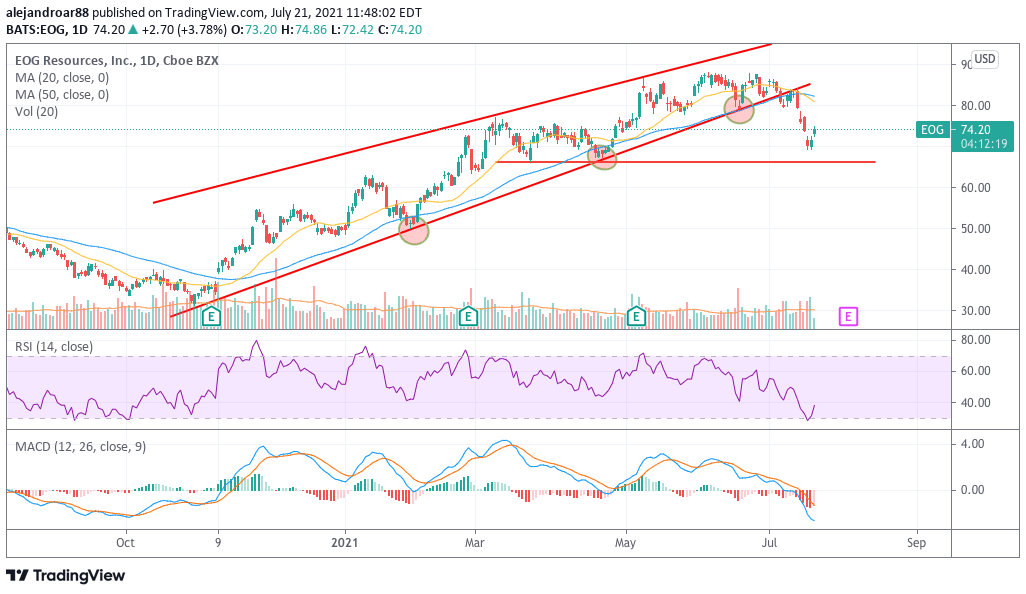

EOG Resources (EOG)

With an impressive track record of delivering solid top and bottom-line margins, EOG Resources stands as one of the strongest players in the energy sector. The company has a diversified portfolio of operations located in the United States, Trinidad and Tobago, and China and currently trades at a market capitalization of $41 billion.

Last year, the company’s results suffered from the impact of the pandemic, with revenues dropping by more than 40% while the firm swung to losses amid the downturn.

However, analysts are expecting to see EOG’s profitability bouncing to $6.69 per share this year and $7.29 in 2022 which results in an overly depressed forward P/E ratio of 10. This multiple seems even more appealing after considering that EOG’s long-term debt stands at $5 billion on assets of $36 billion that include $3.4 billion in cash.

Moreover, the firm is offering a decent 2.2% dividend yield that seems fairly sustainable based on the company’s historical cash flow generation capacity.

In my view, weakness in the oil sector may continue in the following weeks amid concerns about the impact that the Delta variant of the coronavirus could have on the demand for crude. If that is the case, there could be a chance to buy EOG at an even more attractive price if it drops to its next area of support at $66.5 per share.

Renewable Energy Group (REGI)

Renewable Energy Group is an Iowa-based company that produces biofuel from various sources including corn, used cooking oil, and soybeans, generating over $2 billion in sales in the past few years.

REGI’s business has suffered lately due to a jump in commodity prices that have made its operations more expensive. This situation is reflected by a sustained deterioration of the firm’s profit margins, with gross margins sliding from 17% in 2018 to 12.5% last year.

The company produced $123 million in earnings last year and earnings per share of $2.76 while analysts expect to see bottom-line results improving significantly in the following years, possibly landing at $4 per share and $3.6 per share in 2021 and 2022 respectively.

REGI’s finances are air-tight as the company holds a small long-term debt of $35 million on assets of $1.8 billion including $466 million in cash.

Trading at $67 per share, nearly half of the value of REGI is justified by its tangible assets while the value of the technology that the company uses to transform materials into biofuels is being valued at only $1.45 billion – a relatively low price for a technology that can produce $2 billion in sales a year.

Based on these numbers, REGI seems to be conservatively valued and the stock could progressively recover in the following years if the company delivers the positive results that analysts are expecting.

Cabot Oil & Gas Corporation (COG)

The downtrend seen by Cabot’s bottom-line profitability appears to have reached a bottom or at least that is what Wall Street seems to be expecting from this O&G company.

According to consensus estimates from Koyfin, Cabot’s earnings per share are expected to bounce in the following three years from a low of $0.50 per share last year to $1.47 in 2021 and $1.58 per share.

If that turns out to be the case, Cabot appears to be trading at an overly depressed forward P/E multiple of 9 despite its future growth prospects, especially if one considers that the firm’s financials are quite robust with long-term debt of $975 million on assets of $4.5 billion.

Meanwhile, the firm is offering an attractive 2.75% dividend yield on top of this upside potential and it is possible that the dividend may be boosted once the COVID-19 situation is fully under control or the company could decide to resume the stock buybacks it had performed in previous years to keep compensating shareholders.

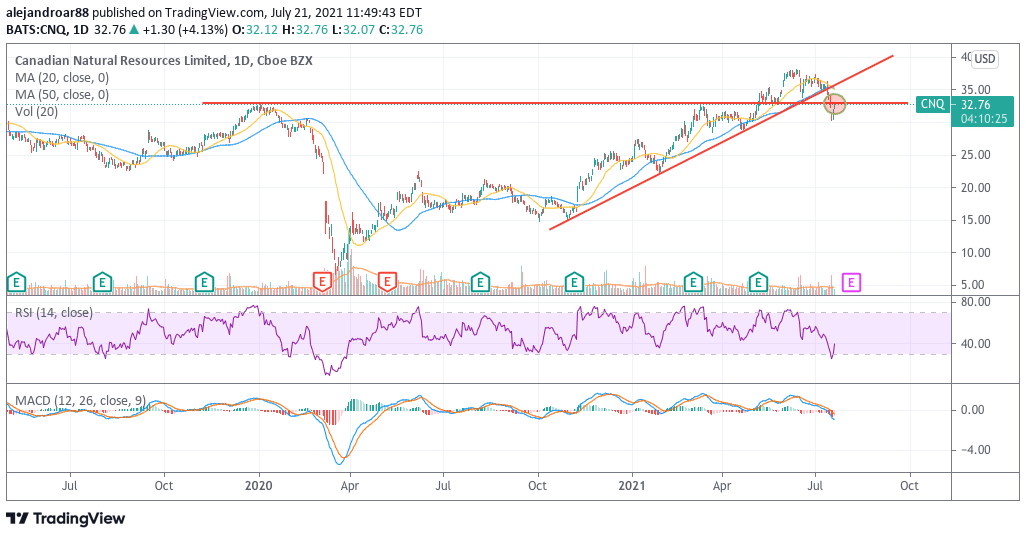

Canadian Natural Resources Limited (CNQ)

CNQ’s track record of revenue growth was quite promising before the pandemic stroke, with sales moving from $13.8 billion in 2017 to $17.6 billion by the end of 2019.

Meanwhile, this diversified energy company had been improving its gross profit margins during that same period, with top-line profitability moving from 16% back in 2017 to as much as 27% by the end of 2019, which resulted in the firm more than doubling its gross profits by the end of that year.

Even though the company’s growth decelerated due to the virus crisis, analysts are expecting to see the firm’s sales recovering their path of growth this year as they are expected to land at $21 billion for a 19% increase compared to 2019’s top-line results.

If net margins end near where they were back in 2019 at around 20%, that would result in earnings of $4.2 billion for the company, which results in a forward P/E multiple of almost 9 for a company that has a relatively low amount of debt.

Moreover, CNQ is offering a remarkably attractive 4.3% dividend yield supported by a strong cash flow generation capacity as indicated by an average historical coverage ratio of 2.5 or higher. Additionally, the firm could resume its stock repurchases this year once the market stabilizes and its finances start to perform as expected.

SPDR Selector Sector Energy ETF (XLE)

If you prefer to follow a more conservative approach when investing in energy stocks, the SPDR Selector Sector Energy ETF (XLE) provides exposure to this attractive corner of the stock market.

However, you should know that the fund’s assets are heavily concentrated in two companies which are Exxon Mobil (XOM) and Chevron Corporation (CVX). These two stocks currently account for over 45% of the fund’s total assets while the remaining assets are spread across a total of 22 other names.

The decision of concentrating most of the portfolio into these two companies could be related to their attractive dividend yields while the annual expense ratio charged by XLE is fairly low at 0.12%.

Buy Stocks at Vindax FX, the World’s #1 trading platform!