5 Best Oil Stocks to Buy in July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Oil prices have experienced a temporary rejection after tagging some long-dated technical resistances following an unexpected impasse during the latest OPEC+ meeting that led the market astray.

Meanwhile, the threat of the Delta variant of the coronavirus and the subsequent reintroduction of travel restrictions and other similar measures in many corners of the world are threatening to slow down the pace at which the global economy is recovering and this results in a depressed outlook for oil demand.

In this particularly unfavorable short-term backdrop, certain oil stocks could be trading at more attractive prices compared to a month ago and that opens up an opportunity for investors.

With that in mind, the following article lists five names that you might want to keep an eye on as they display robust financials, sound profit margins, and attractive upside potential once oil prices recover their seemingly lost strength.

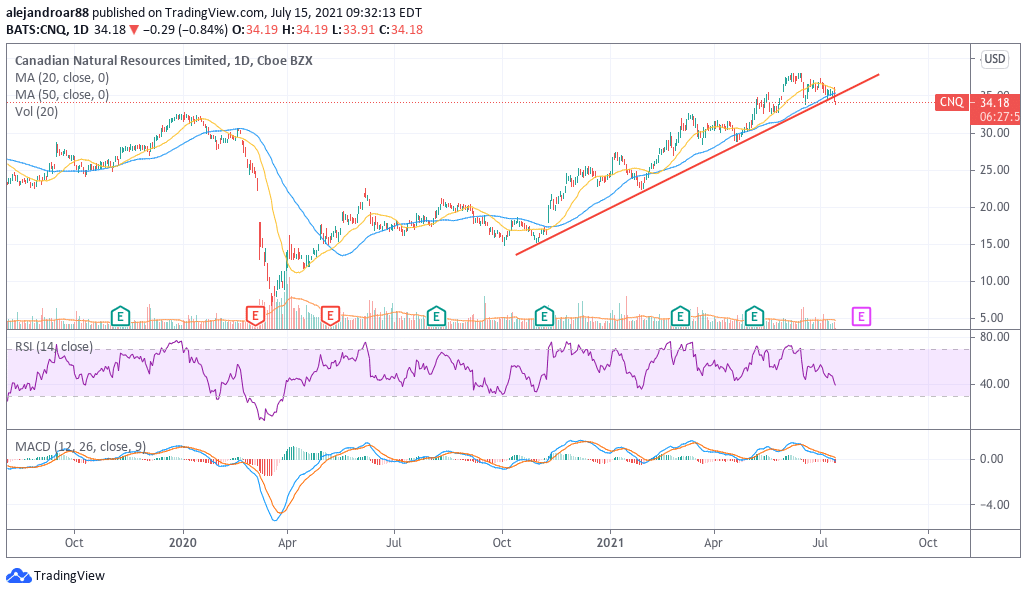

Canadian Natural Resources Limited (CNQ)

Canadian Natural Resources is a Calgary-based diversified energy company with oil & gas operations in the Alberta-Saskatchewan border and other areas of Western Canada.

Although sales declined last year due to historically low oil prices, the company had managed to grow its top-line results by the low double-digits in the two years that preceded the pandemic.

Gross profit margins for CNR were also improving before the pandemic stroked, moving from 16% back in 2017 to 27% by the end of 2019. The same trend was seen in the firm’s operating margins, which climbed from 13.4% to 24.5% during the same period.

By the end of the first quarter of 2021, CNR held a total of $15.6 billion in long-term debt on total assets of $59 billion including $468 million in cash and equivalents.

The company is currently offering an attractive 4.1% dividend yield at the moment that seems to be well covered based on its historical cash flow generation capacity and higher oil prices should continue to assist the firm in maintaining and even growing its dividend in the near future.

Meanwhile, the stock is trading at a highly conservative forward P/E ratio of 10, which creates room for further upside potential if oil prices remain at their currently elevated levels for longer than expected.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Diamondback Energy (FANG)

Currently trading at an attractive forward P/E ratio of 9, Diamondback Energy seems even more attractive than it did last month as the company managed to maintain great operating profit margins while also growing its sales at a fast pace in the three years that preceded the pandemic.

Analysts are expecting to see a resumption of this explosive growth for Diamondback in the following years, with EPS estimates currently standing at $8 per share for 2021 and $11.7 for 2022.

The balance sheet shows that the firm currently holds a net debt of $7.5 billion on assets of $22 billion while offering a 1.9% dividend yield on top of the upside potential that could come once the company starts to deliver the positive results the market is expecting to see this year.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Exxon Mobil (XOM)

Valuation multiples for Exxon (XOM) have dropped this month as a result of the latest weakness in the price of oil, which has resulted in an even more attractive dividend yield of 5.9% currently offered by the oil & gas giant.

The latest failed negotiations from OPEC could open the door for higher production quotas and Exxon is particularly well positioned to benefit from this situation in the form of higher volumes on above-average prices.

Analysts are anticipating that sales for Exxon should come in above pre-pandemic levels this year at around $266 billion while earnings per share for 2021 are expected to land at $3.88, resulting in a forward P/E ratio of 15. This ratio is fairly conservative as Exxon is expected to grow its bottom-line results at a rate of around 15% for the coming two to three years on the back of higher commodity prices.

If that scenario unfolds as expected, dividend coverage should not be a concern unless the company decides to ramp up its capital expenditures dramatically. During the first quarter of 2021, the management team emphasized that capital expenditures should remain between $16 to $19 billion, which would result in a dividend coverage of around 1.

Even if the dividend is slashed by a quarter, it would still be fairly attractive at around 4.3%.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Cabot Oil & Gas Corporation (COG)

Despite the firm’s latest disappointing performance, Cabot Oil has been progressively deleveraging its balance sheet to reduce the impact of interest expenses on its bottom-line profitability.

In the past three years, long-term debt has been reduced from $1.23 billion to $976 million, which results in a more conservative debt-to-equity ratio for COG.

Meanwhile, the company’s merger with Cimarex, announced on 24 May, opens up the door for cost synergies and potential bottom-line growth in the following years on the back of economies of scale.

Market participants seem to be on board with this possibility as they are anticipating earnings per share above pre-pandemic levels for the next two to three years for COG amid improved market conditions and higher operating margins.

At the current forward P/E ratio of 10, Cabot’s shares might not be fully pricing the possibility of higher profit margins and higher sales resulting from the merger.

67% of all retail investor accounts lose money when trading CFDs with this provider.

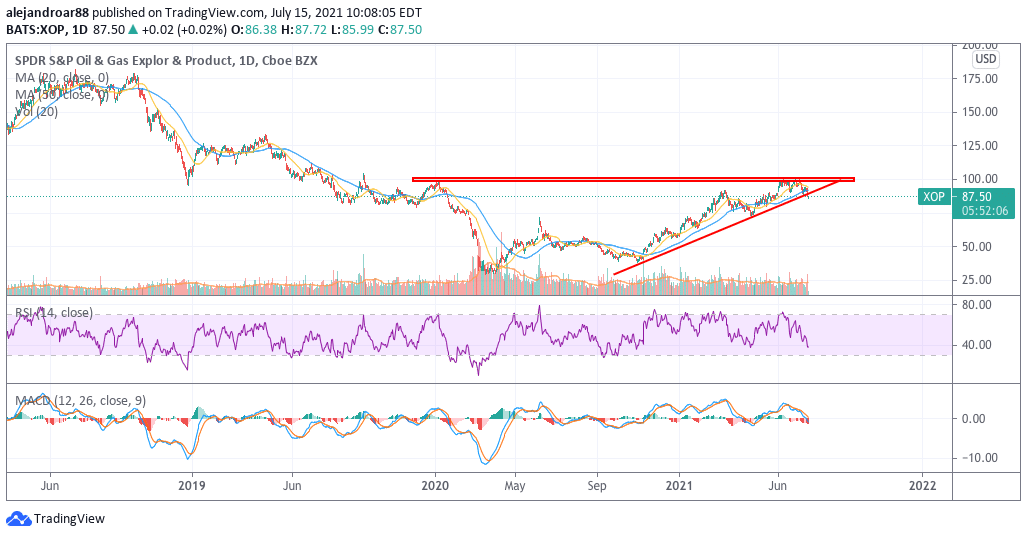

SPDR S&P Oil & Gas ETF (XOP)

For those who prefer to approach oil & gas stocks more conservatively for the time being, the SPDR Oil & Gas ETF (XOP) is offering the possibility of getting exposure to this market without having to hand pick which players will emerge as the biggest winners from the latest strength in the price of crude.

XOP is a widely diversified ETF that holds a basket of over 56 names in the O&G industry, with the top 10 holdings only accounting for a quarter of the fund’s $3.86 billion in assets under management.

The latest price action seen by this ETF has broken below a long-dated lower trend line dating back to the November vaccine-related uptick. Although this indicates a short-term weakness in the sector, analysts remain bullish on oil due to the prolonged supply and demand imbalances that the pandemic has caused.

Therefore, a correction in the price of XOP could present itself as an opportunity for those who are late to this latest energy rally as they will be able to get exposure to the sector at a relatively lower valuation multiple compared to last month.

Buy Stocks at Vindax FX, the World’s #1 trading platform!