5 Best Blue Chip Stocks to Buy in July 2021

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

With so much attention being caught by meme stocks and short-squeezed low-volume issues, blue-chip stocks have taken the back seat in today’s cash-flooded stock market.

However, the fact that the public is not paying that much attention to companies that are natural winners in their respective markets is opening up opportunities for disciplined investors who focus on long-term results instead of short-term, and often short-lived, gains.

The following list presents five high-quality stocks with decent upside potential despite their huge size and long-standing reign.

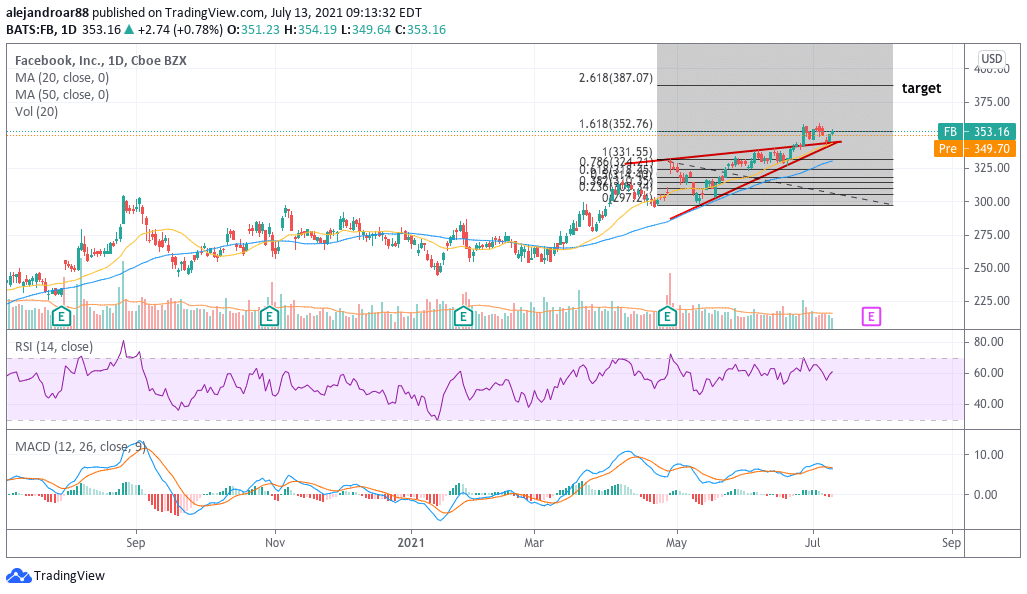

1. Facebook (FB)

A favorable ruling for the company in an antitrust claim brought up by the Federal Trade Commission (FTC) has allowed Facebook (FB) to finally climb above the $1 trillion valuation threshold.

Meanwhile, although market participants remain concerned about the government’s seemingly hostile attitude toward the company’s practices, it is hard to deny that Facebook is one of the most profitable and successful companies of the last decade.

Facebook sales have grown at an accelerated pace and may continue to follow this path in the following years as more and more businesses realize the power of digital advertising while there are still many untapped avenues of revenue for the social media giant including the potential monetization of its popular messaging platform WhatsApp.

Meanwhile, trading at a fairly conservative forward price-to-earnings ratio of 23, Facebook stock can be qualified as a bargain based on the company’s historical earnings growth, robust fundamentals, and debt-free balance sheet.

67% of all retail investor accounts lose money when trading CFDs with this provider.

2. Intel Corporation (INTC)

Once the almighty ruler of the chip industry, the value of INTC has declined sharply lately as competitors continue to eat up chunks of the company’s market share. However, according to data from Statista, Intel remains the leader of the industry, currently amassing a 15.6% share of the global semiconductor market.

The firm’s historical revenue growth demonstrates the fruitfulness of that leadership at a time when large-scale shortages are providing a short-term tailwind for the entire industry, with sales of the Santa Clara-based chipmaker rising nearly 8% last year.

That said, bottom-line profitability for Intel has not grown at the pace one would expect for a company in such a thriving sector as Intel’s net income has failed to climb above the $21 billion threshold in the past three years at least.

Meanwhile, the company expects to see its net earnings shrinking almost 10% this year to around $4 per share while sales are expected to land at $77 billion – nearly the same figure reported by Intel last year. At these forecasted levels, INTC stock is being valued at only 14 times the firm’s forecasted earnings for the year.

Despite this temporary weakness in the company’s ability to grow its top and bottom-line results, Intel remains a conservatively financed blue-chip stock that currently offers an appealing 2.5% dividend yield.

This dividend, along with billions of dollars in share buybacks made by the company every year, should provide enough support to the price of INTC to withstand the current negative momentum until the management figures out a way to bring the company back to a path of sustained growth.

The downside risk at this overly depressed valuation multiples is fairly low while the dividend should compensate shareholders for waiting until a turnaround happens – in which case the upside potential for Intel could be sizable.

67% of all retail investor accounts lose money when trading CFDs with this provider.

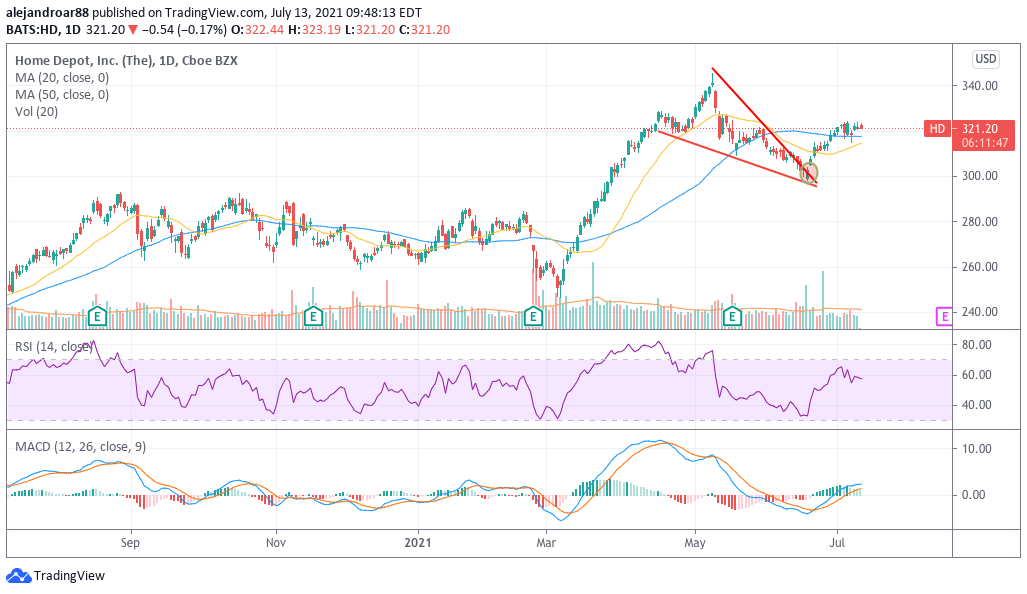

3. Home Depot (HD)

The pandemic seems to have generated a long-lasting tailwind for Home Depot’s business as consumers spent their time improving their homes while they remained confined within them.

Sales for the home improvement giant rose 20% last year to $132.1 billion while net income was pushed from $11.2 billion in 2019 to $12.9 billion by the end of 2020.

A booming housing market could further catalyze Home Depot’s financial results in the coming quarters as more renovations will probably be performed by first-time buyers and property flippers while historically low mortgage rates could prolong this trend for longer.

In this overly positive environment, Home Depot sales should continue to thrive and the market seems to be expecting this as both revenues and earnings are expected to grow at an accelerated pace this year compared to the company’s historical growth rates.

Currently being valued at only 23 times its forecasted earnings per share for the next twelve months while offering a 2% dividend yield, Home Depot shares are offering the best of both worlds – a conservatively valued blue-chip stock positioned in what could be a high-growth industry in the current environment.

Meanwhile, the firm’s ample free cash flows could open up opportunities to acquire promising businesses, repurchase more shares, or hike the current dividend, with any of these three outcomes possibly setting the stage for further upside for the stock.

67% of all retail investor accounts lose money when trading CFDs with this provider.

4. Microsoft (MSFT)

Microsoft (MSFT) has managed to keep pushing its revenues higher at a rate that may have been unthinkable for a business of its size due to its ability to adapt and respond quite precisely to the needs of the market.

In this regard, the firm’s Intelligent Cloud segment has been the tip of the spear for Microsoft’s latest growth and sales show the impact of this strategy as top-line results for the company founded by Bill Gates has surged at an average of 13% in the past four years at least.

Meanwhile, profitability has nearly doubled during the same period while profit margins have improved dramatically. Gross margins have moved from 64% in 2017 to 68% last year while net margins have risen from 26.5% to 31% during that same period.

The same goes for other profitability ratios including the firm’s return on equity(ROE), which has risen from 29% to 40%.

The diversified nature of Microsoft’s business alongside the positive contribution of the cloud segment to the firm’s top and bottom-line results is a perfect combination that makes this company one of the most promising blue-chip stocks out there.

With Microsoft’s forward P/E and P/FCFs ratios currently standing at around 40, Microsoft appears to be an undervalued stock based on the rate at which the company has managed to grow its net earnings in the past four years at least.

67% of all retail investor accounts lose money when trading CFDs with this provider.

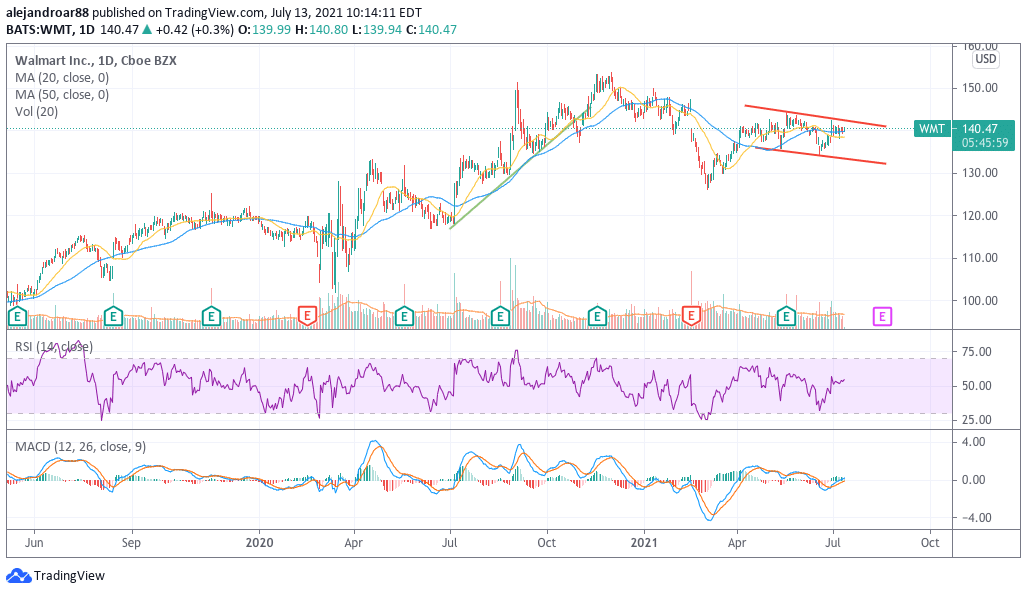

5. Walmart (WMT)

Walmart emerged as a pandemic winner as the company managed to grow its sales by 6% last year, effectively overturning a trend of declining top-line growth seen by the business in the three years that preceded the health crisis.

The positive performance of its e-commerce unit could possibly be a game-changer for Walmart and the market seems to be acknowledging that possibility as analysts are expecting higher earnings for the firm despite forecasting stalled revenue growth for the coming years.

Meanwhile, the big-box retailer is being valued at just 20 times its 2020 free cash flows, which is a fairly conservative multiple for a company that could put its ample cash reserves to use at any given point to further boost the performance of its business.

Moreover, currently offering a 1.6% dividend yield, Walmart seems like a much better place to park money than a bank and, for those who are patient enough, the company could deliver sizable capital gains if its e-commerce strategy and upcoming cash deployments deliver the kind of growth that could keep accelerating the firm’s earnings growth over the coming years.

Buy Stocks at eToro, the World’s #1 trading platform!