Clorox Stock Down 12% Today – Time to Buy CLX Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Clorox stock is going down nearly 12% in pre-market stock trading action this morning after the company reported its financial results covering the second quarter of the 2022 fiscal year as earnings disappointed while the management trimmed its guidance for both revenues and profits for the entire year.

For the three months ended on 31 December, Clorox reported total revenues of $1.69 billion resulting in an 8% drop compared to the same period a year ago amid a sharp decline in business volumes resulting from a fading pandemic tailwind. Analysts had estimate sales of $1.66 billion for the period.

The health and wellness segment – the largest by revenue – took the strongest hit as sales declined 21% during the quarter at $648 million. So far this year, sales from this segment accumulate a 15% year-on-year decline.

Gross margins for the period were 1,240 basis points below the previous year at 33% due to “higher manufacturing & logistics and commodity costs” as inflation and supply-chain disruptions continued to weigh on the performance of the company.

As a result, the firm’s adjusted earnings per share suffered a 67% decline at $0.66. This figure was 25 cents below Wall Street’s consensus estimate for the quarter and it is possibly the main reason why Clorox stock is dropping this morning.

The management qualified the current cost environment as “challenging” and stated that they expected “cost pressures” to continue for what remains of the 2022 fiscal year.

What could be expected from this former pandemic winner after this disappointing quarterly report? In this article, I’ll be assessing the price action and fundamentals of CLX stock to outline plausible scenarios for the future.

68% of all retail investor accounts lose money when trading CFDs with this provider.

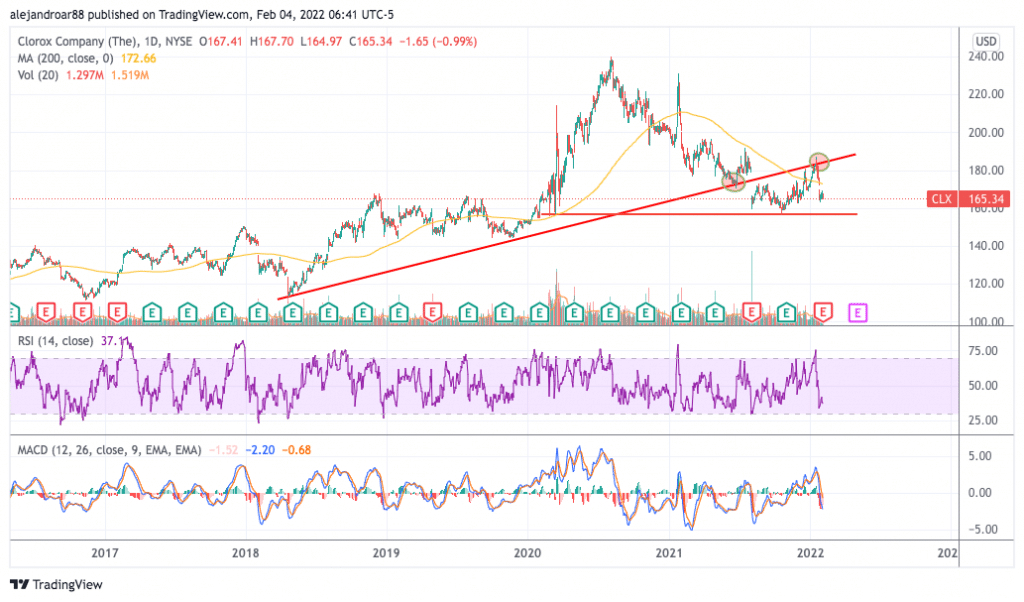

Clorox Stock – Technical Analysis

If today’s pre-market downtick spills over to the live session as-is, Clorox would now be trading 26% below its 52-week high of $197 per share from August 2020 back when the pandemic was acting as a strong tailwind for the firm’s top and bottom-line financial performance.

Moreover, the price has once again dropped below the 200-day simple moving average, emphasizing the market’s concerns about the firm’s mid-term outlook in this challenging environment.

As the chart show, the price rejected a climb above a former trend line support that now seems to be acting as resistance and that prompted a meltdown that pushed the price to its current levels.

Momentum indicators are favoring a bearish short-term outlook for CLX stock, with the Relative Strength Index (RSI) already dropping below the 50 level (bearish) while the MACD remains in negative territory and below the signal line.

Today’s decline is pushing the price below the $150 level – a crucial area of support – and the odds point to a full-blown decline toward the low 140s for a total downside risk of around 16%.

Clorox Stock – Fundamental Analysis

Clorox’s management just updated its guidance for the entire 2022 fiscal year. The company now expects to report a 1% to 4% decline in its sales and a 750 basis points reduction in gross margins.

Moreover, adjusted diluted earnings per share are expected to land between $4.25 and $4.5 resulting in a maximum 41% drop compared to the same period a year ago as rising raw materials and logistics costs keep weighing on the financial performance of the cleaning products manufacturer.

These headwinds are no small feat as they can keep the company’s valuation depressed for a long time since these supply chain disruptions are not yet showing signs of improving.

Based on the management’s EPS estimates for the year, Clorox would be trading at 32 times its forecasted earnings if we assume that the price during the live session will be similar to that of today’s pre-market session.

Clorox’s long-term debt stands at $1.9 billion on total assets of $6.2 billion including $1.6 billion in goodwill. The company reported total cash and equivalents of $192 million. A total of $300 million of the firm’s long-term debt must be repaid or refinanced this year along with another $600 million next year.

During the first six months of the 2022 fiscal year, the firm produced $113 million in free cash flows and repaid $300 million in long-term debt and $290 million in dividends.

Even though the current dividend yield seems attractive at around 3%, it seems highly unlikely that the company will be able to maintain it for what remains of the year in this current environment.

A reduction in CLX’s dividend could lead to further negative volatility down the road. Therefore, considering the confluence of multiple headwinds, the outlook for CLX stock is also bearish from a fundamental perspective.

Buy CLX Stock at eToro with 0% Commission Now!