Chewy Stock Price Down 8% Today – Time to Buy CHWY Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Petcare company Chewy (CHWY) was trading 8% lower in US premarket price action today. The stock had fallen over 6% yesterday also and is now down 37.4% for the year.

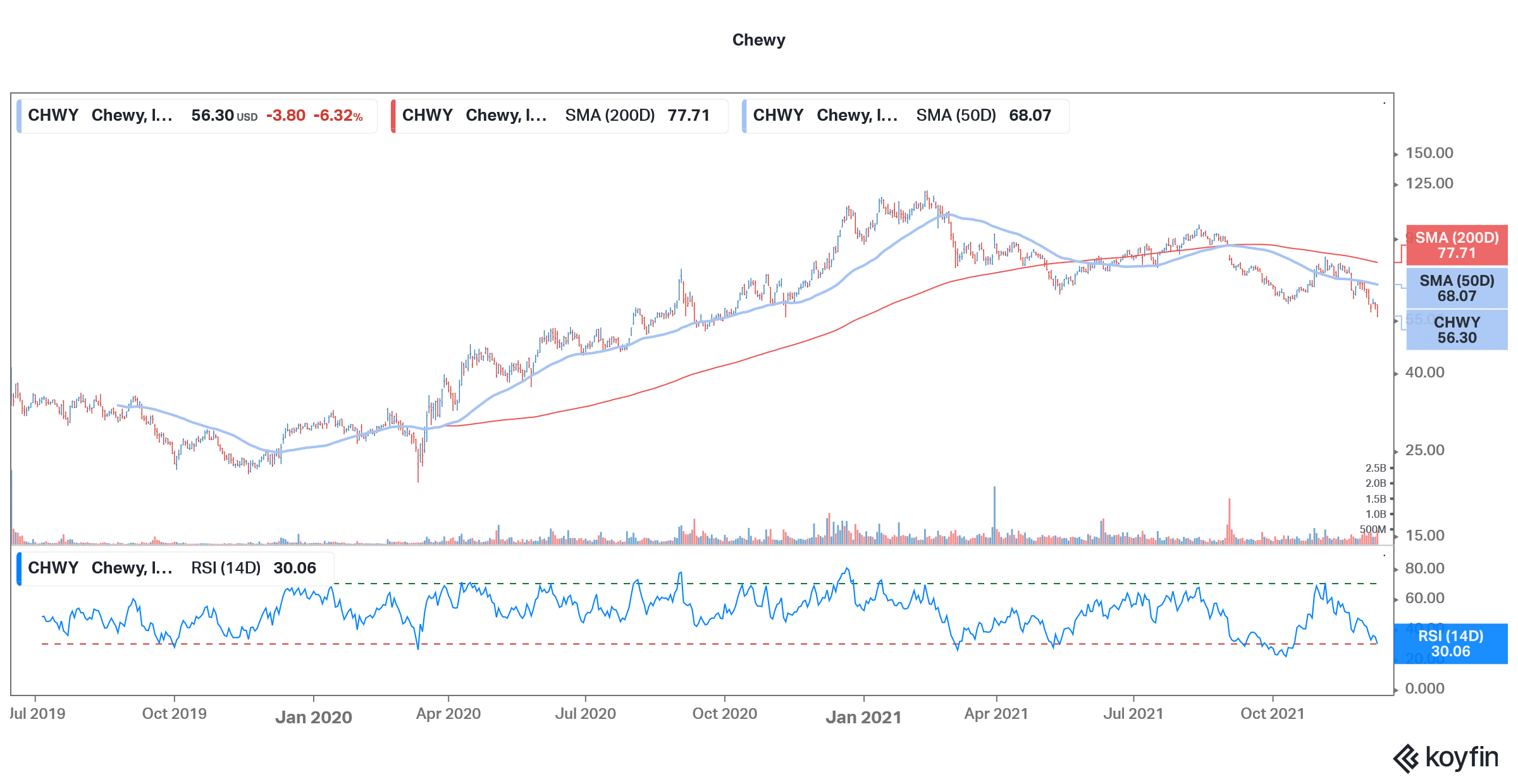

Chewy stock trades at less than half of its 52-week highs and hit a new 52-week low of $55.95 yesterday. While it managed to close slightly above the price level, it looks set to make a new 52-week low today. The stock’s dismal run is coming at a time when the broader markets are up sharply for the year. What’s the forecast for CHWY stock and should you buy the dip or the stock could fall more from these levels?

Chewy stock technical analysis

Chewy stock is looking bearish on the charts and has fallen below all moving averages including the 50-day, 100-day, and 200-day SMA (simple moving average). The stock has been hitting new lows which is also a bearish indicator. However, after the sharp fall, the stock appears oversold with a 14-day RSI (relative strength index) of 30, which would fall further in today’s price action. RSI values below 30 signal oversold positions while values above 70 signal overbought positions.

68% of all retail investor accounts lose money when trading CFDs with this provider.

CHWY latest news: Earnings miss spooked investors

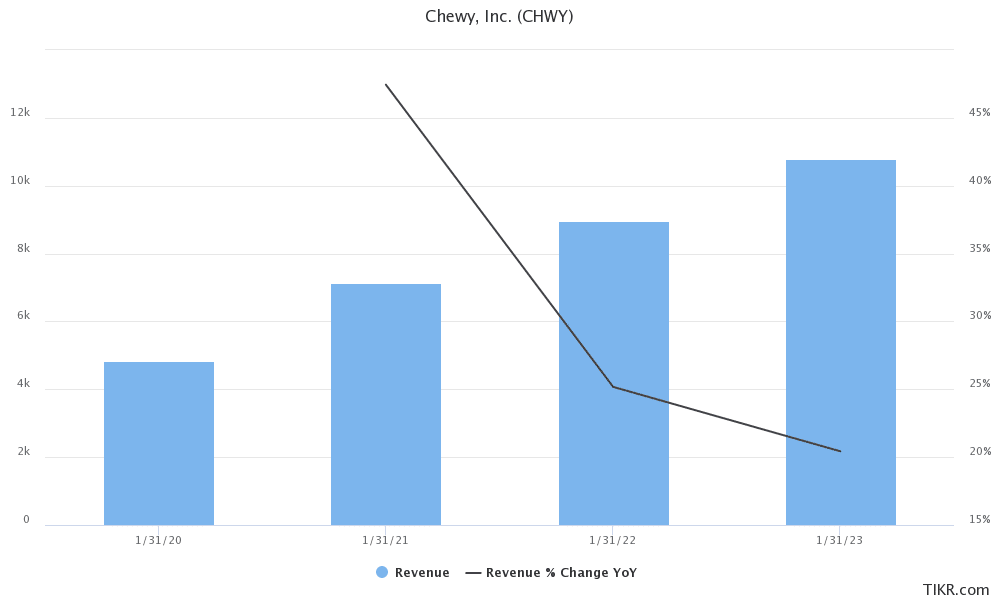

Chewy released its fiscal third-quarter 2022 earnings yesterday after the close of markets. Its revenues increased a healthy 24% and hit $2.21 billion in the quarter. The company’s topline performance was in line with its guidance as well as analysts’ estimates. However, it’s the bottomline performance that spooked investors. The company reported an adjusted EBITDA of $6 million, which was almost 10% higher than the corresponding period last year. However, it was way below the $23 million that analysts were expecting. The company’s per-share loss of 8 cents was twice what analysts were expecting.

Also, while CHWY’s gross margin in the quarter was 26.4%, which was better than the 25.5% that it reported in the third quarter of the last fiscal year, the metric was well below the 27.1% that analysts were expecting.

Chewy is facing cost headwinds

Like most other US companies, Chewy is facing cost headwinds. While prices of everything from labor costs, packaging, and logistics have gone up, many companies have not been able to fully pass on higher prices to consumers. Stock markets also gave a thumbs down to CHWY’s earnings and sent the stock south. Notably, Chewy stock had tumbled after the fiscal second-quarter earnings as well.

While Chewy CEO Sumit Singh expressed optimism on the strong sales growth, he also weighed on the margin pressure. He said, “Our third-quarter profitability reflects the impact of ongoing supply chain disruptions, labor shortages, and higher inflation.” However, Singh added, “As we work through these macro uncertainties, we remain squarely focused on the long term and on building an enduring franchise to serve millions of loyal pets, pet parents, and partners.”

CHWY guidance

Chewy expects to post revenues between $2.4-$2.44 billion in the fiscal fourth quarter which was barely in line with analysts’ estimates. Meanwhile, the company’s active customer base increased 14.7% YoY in the quarter while net sales per active customer increased 15.4%.

Chewy stock forecast

Wall Street analysts are bullish on Chewy stock, and it has a consensus buy rating. Overall, of the 24 analysts covering the stock, 13 have rated it as a buy while nine have a hold rating. The remaining two analysts rate the stock as a sell or some equivalent.

Chewy’s median target price of $92.50 is a premium of almost 79%. The street high target price of $133 implies an upside of 157%. After the recent crash, Chewy even trades 27.7% below its street low target price. Meanwhile, Wall Street analysts might revise down their target price on the stock amid the margin pressure. Usually, analysts update a stock’s target price and ratings after the earnings release.

Notably, ahead of the earnings release, Wedbush had downgraded CHWY stock from outperform to neutral and lowered its target price to $70. “CHWY is well-positioned to capture market share given a long-term secular channel shift in the pet retail industry, but we now expect at best in-line results for 2H21 and growth below consensus in 2022,” said Wedbush analyst Seth Basham in their note.

Chewy stock long-term forecast

To be sure, like a lot of stay-at-home companies, CHWY is also battling a growth slowdown. However, the long-term forecast for the pet care industry looks positive. The company is also diversifying the business and earlier this month it partnered with Trupanion to expand into pet insurance. While there are short-term growth and margin concerns, the long-term growth story for Chewy looks solid. Also, even as the company’s growth is arguably coming down, analysts expect the company’s revenues to rise by more than 20% in the next fiscal year also. As cost pressures ease, its adjusted EBITDA is expected to jump over 85% in the next fiscal year.

Should you buy CHWY stock

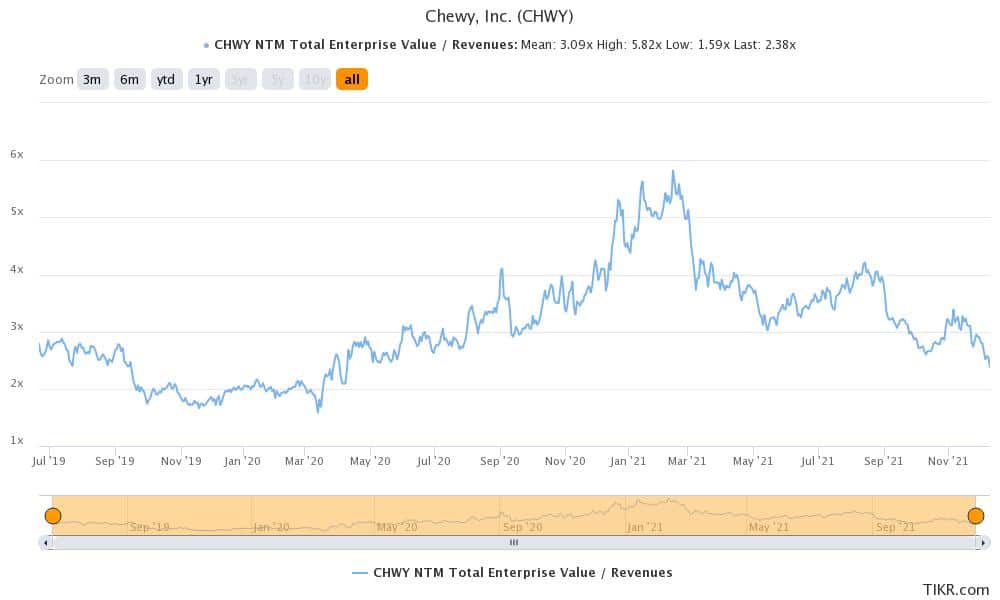

Chewy stock trades at an NTM (next-12 months) enterprise value-to-sales multiple of 2.38x. The multiple has averaged 3.09x since the company was listed. It hit a low of 1.59x in March 2020 as the US stock markets tumbled amid fears over the COVID-19 pandemic and hit a high of 5.6x in February 2021. Notably, growth stocks have been weak since February 2021.

While there are concerns over slowing growth, the monetary policy tightening by the US Federal Reserve is not helping either. Higher future interest rates are negative for growth names like Chewy.

All said, at current valuations, the growth slowdown largely looks priced in the stock. It might be prudent to buy the dip in CHWY stock and add more shares if it were to dip further. If you want to play the growing pet care market in the US, Chewy stock looks among the best bets.

Buy CHWY Stock at eToro from just $50 Now!