Madison Square Garden Stock Down 6% In November – Time to Buy MSGS Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Madison Square Garden stock is down 6% so far this month following a disappointing quarterly report in which the company missed analysts’ revenue estimates for the period.

For the three months ended on 30 September, the firm reported revenues of $18.8 million resulting in a 67% drop compared to the same period a year ago while its adjusted operating loss was 58% higher at $28.1 million compared to $17.8 million it reported a year ago. Analysts had estimated revenues of $35.1 million for the firm.

The company cited “declines in league distribution revenues and local media rights fees” as the primary cause for this decline in its top-line results.

Meanwhile, the owner of the New York Knicks NBA basketball team reported GAAP net losses of $16.4 million resulting in a per-share figure of minus $0.68. Analysts had estimated losses of $1.04 per share for the quarter.

On a positive note, MSG announced last week that it signed a marketing deal with BetMGM to make this online sports betting platform its official partner for the Knicks, Rangers, and Madison Square Garden Arena.

What can be expected from this entertainment stock following the sharp decline seen so far in November? In this article, I’ll attempt to answer that question by assessing the price action and fundamentals of Madison Square Garden stock as we keep heading toward the end of the year.

67% of all retail investor accounts lose money when trading CFDs with this provider.

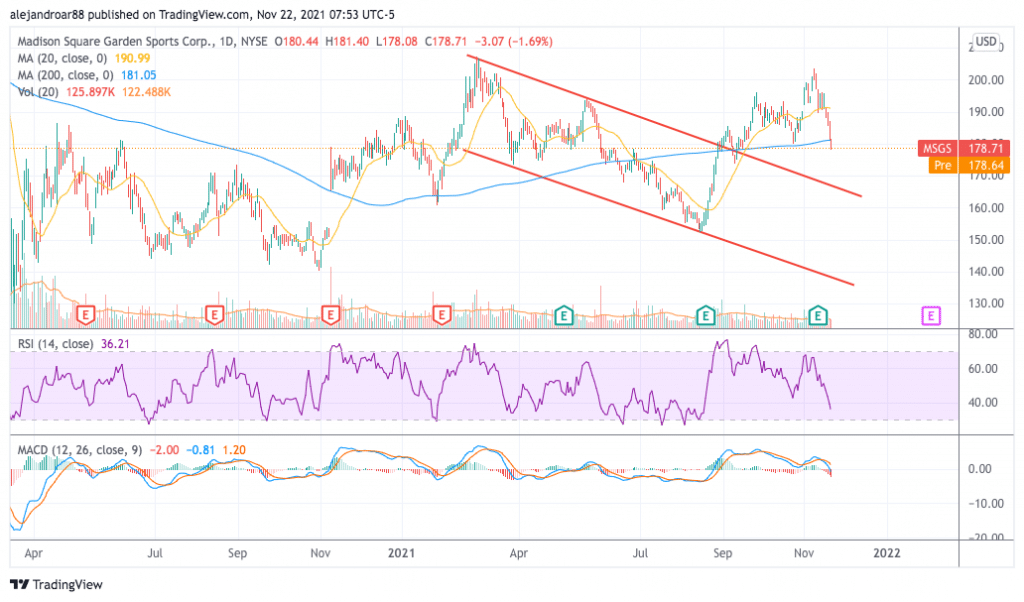

Madison Square Garden Stock – Technical Analysis

Even though the price of MSGS stock managed to reverse the downtrend that started in March this year amid the rapid spread of the Delta variant in the United States, it is still far from where it was before the health crisis started.

Meanwhile, this latest quarterly report has plunged the stock below its short-term moving averages and last Friday’s price action broke below the 200-day moving average as market participants appear to have been discouraged after these latest quarterly results came out.

Thus far, the stock has gone down in 7 out of the past 9 trading sessions. However, trading volumes have not been necessarily worrying as they have remained near or below the average in most of those days.

Momentum indicators are all pointing to a bearish outlook with the Relative Strength Index (RSI) currently standing at 36 following a pronounced bearish divergence while the MACD has just crossed below the signal line. This move is being accompanied by steadily increasing negative histogram readings.

All things considered, the outlook for Madison Square Garden stocks seems bearish based on its current technical setup. The next area of support if the price remains below the 200-day simple moving average would be found at around $170 per share – the trend line’s resistance now turned to support that is shown in the chart.

Madison Square Garden Stock – Fundamental Analysis

Revenues for MSG had been steadily declining even before the pandemic started, moving from $1.32 billion back in 2017 to $729.4 million by the end of the 2019 fiscal year ended in June that year. Moreover, the firm’s GAAP operating profits have been negative in the past 10 years.

Meanwhile, the company had to take on $350 million in long-term debt during the pandemic to survive the downturn and this weakened its financial health and could be an issue for the business down the road.

At its current market cap of $4.33 billion, MSGS is being valued at 5.7 times its forecasted sales for the next 12 months while its EV/EBITDA ratio is standing at 106.5x.

Most of this valuation is supported by the value of the strong brands owned and operated by the firm including the Knicks, the Rangers (NHL), and the Madison Square Garden Arena.

According to data from Statista, the Knicks are considered the most valuable basketball brand in the NBA with an estimated price tag of $5 billion. That brand alone may justify the current valuation assigned to the company.

That said, it would take an acquisition or another similar transaction for shareholders to receive the full value of their investment as the market seems to be currently appraising the firm’s profit-generation capacity instead of the sum of its parts.

Buy MSGS Stock at eToro with 0% Commission Now!