Antofagasta Share Price Forecast November 2021 – Time to Buy ANTO Shares?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The share price of Chile-based copper miner Antofagasta (LSE: ANTO) has sagged this year and is up only about 3%, underperforming the FTSE 100. What’s the forecast for ANTO shares and is it a good time to buy it now after the recent underperformance?

The UK market is home to several miners. Apart from Antofagasta, Anglo American and Glencore are the other major miners with sizeable copper operations. Rio Tinto and BHP Billiton are the other UK-listed miners. While both these companies have significant copper operations and BHP is among the leading copper miners globally, they get most of their revenues from iron ore.

Antofagasta recent developments

Last month, Antofagasta released its third-quarter production report. Usually, mining companies release production reports on a quarterly basis and financial results on a half-yearly basis. The company produced 181,100 tonnes of copper in the quarter which was 1.5% higher than the corresponding period in 2020. While the production at its Los Pelambres mine was lower, it was more than offset by the increased production at Centinela.

In the first nine months of the year, the company produced 542,600 tonnes of copper which were 0.2% higher than the corresponding period last year. The company maintained its annual guidance of 710-740,000 tonnes of copper.

Antofagasta produced 66,800 ounces of gold in the third quarter, which was 8.8% higher than the previous quarter. The company’s molybdenum production however fell 7.1% over the period. Both gold and molybdenum are the byproducts in copper production and help copper miners lower their unit cash cost after by-product credit.

Net cash costs rise for Antofagasta

Antofagasta reported net unit cash costs of $1.16 per pound in the quarter, which was 2.7% higher than the corresponding quarter in 2020. Notably, copper mining companies are battling cost pressures. While labour costs have gone up, higher energy prices are also adding to the costs for miners. Diesel is a key input for copper miners but prices have spiked this year as crude oil prices have surged to multi-year highs.

Meanwhile, despite the cost pressures, the company expects its full-year net unit cash costs to be below its previous guidance of $1.25 per pound. “While we expect the extraordinary global supply chain events and energy crisis to ease over time, we remain focused on controlling costs while progressing our current and future growth projects,” it said in its release.

Antofagasta expects production to fall in 2022

Meanwhile, Antofagasta expects its production to fall to 660-690,000 tonnes next year due to the weather conditions and lower grades at Centinela operations. Notably, mining companies globally are struggling with lower ore grades even as new mine development has lagged. While mining companies, in general, had cut down on their capex, some of the new mines have been facing issues related to environmental issues and protests by local communities.

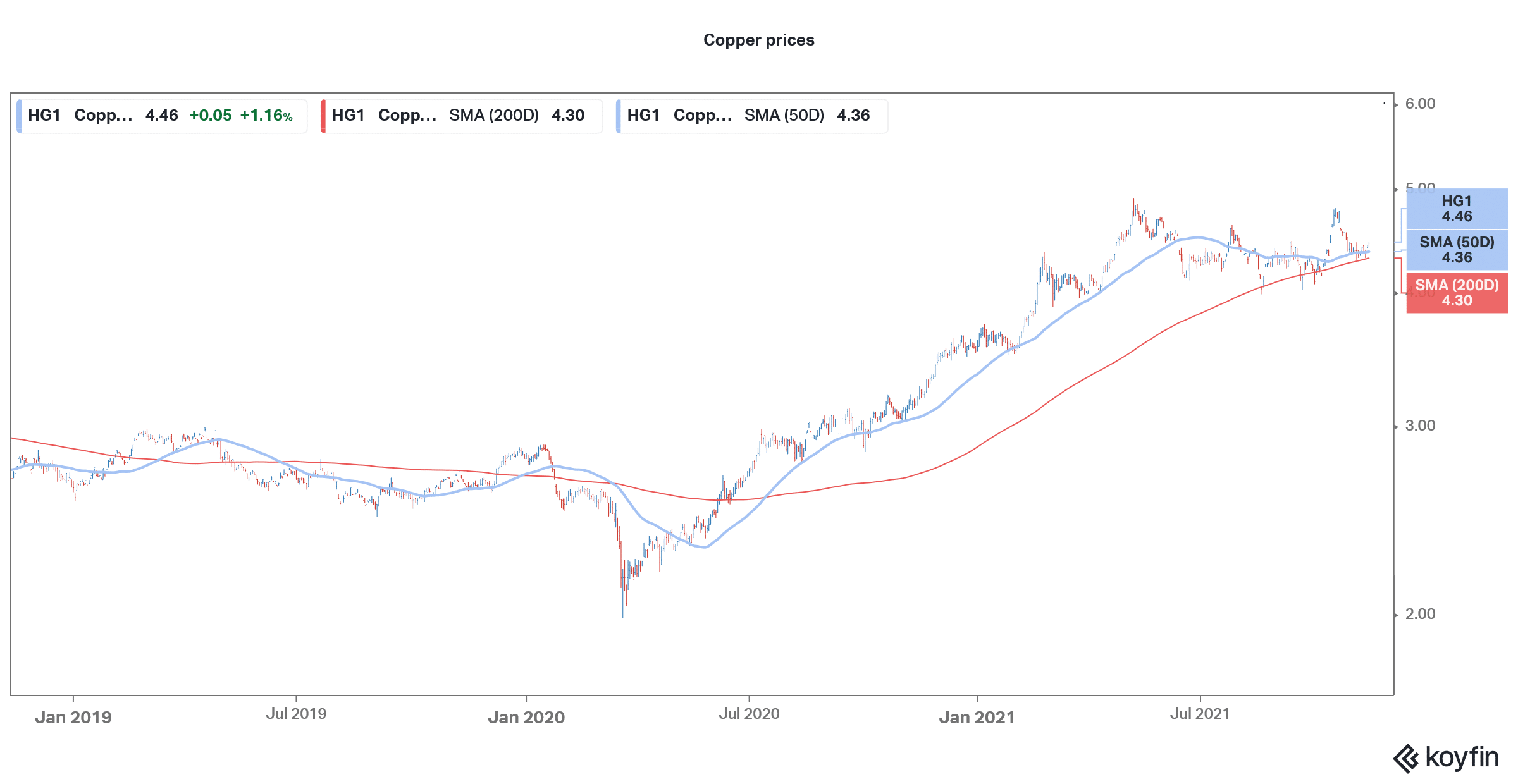

Copper’s outlook looks positive

Copper’s outlook looks positive. The copper intensity in electric cars and renewable energy is higher than ICE (internal combustion engine) cars and non-renewable energy generation respectively. As the world transitions towards a greener future, copper assets would be in demand. Given the relative scarcity of pure-play copper mining companies, companies like ANTO can attract a valuation premium. Also, big miners might also look at acquiring pure-play copper miners in a bid to shore up their copper portfolio.

Goldman Sachs expects copper to run even higher

There is a general belief that copper would see a supply scarcity as demand sours from electric vehicle companies. Goldman Sachs expects copper prices to rise to $15,000 per tonne by 2025 and called it a new oil. “Discussions of peak oil demand overlook the fact that without a surge in the use of copper and other key metals, the substitution of renewables for oil will not happen,” it said in its note.

During Freeport-McMoRan’s third-quarter earnings call, CEO Richard Adkerson said that the “fundamental outlook for copper is incredibly favorable.” He also called copper a “strategic metal” and said it is essential for tackling climate change.

Notably, the demand for electricity, and by its extension investment in the grid and other infrastructure would rise as the world moves towards electric vehicles. This would mean more demand for copper and support higher prices.

Antofagasta share price forecast

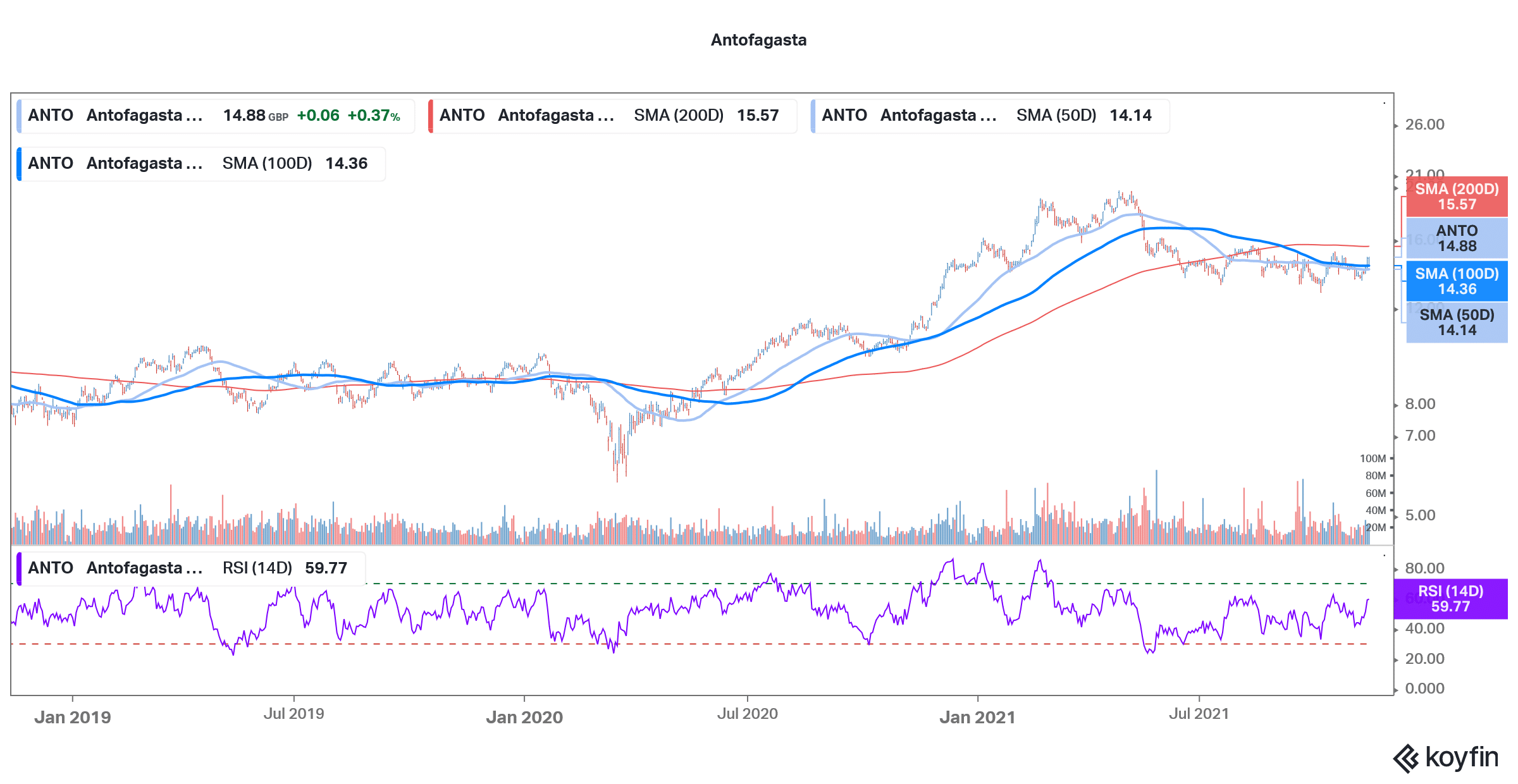

Of the 17 analysts covering Antofagasta shares, four rate them as a buy while nine have a hold rating. The remaining four analysts have a sell rating on the shares. It has a median target price of 1,468.5p which is a discount of 1.3% from these levels. Its street high target price of 1,689p is a premium of 14.1%.

Brokerages don’t look too optimistic on Antofagasta shares. However, pure-play copper mining companies like ANTO look for a good way to invest in copper. Given the relative scarcity of pure-play copper mining companies, companies like ANTO can attract a valuation premium. Currently, the shares trade at an NTM (next-12 months) EV-to-EBITDA multiple of around 5x which looks reasonable.

Looking at the charts, Antofagasta shares have crossed above their 50-day and 100-day SMA (simple moving average) which is a bullish technical indicator. However, they still trade below the 200-day SMA. The 14-day RSI (relative strength index) of 59.7 is a neutral indicator.

All said, the outlook for copper and copper miners looks positive. If you want to get exposure to copper, you can do it by directly trading in copper. An alternate approach would be to invest in shares of copper mining companies.

Antofagasta has a good position on the global copper cost curve. With their reasonable valuations, the shares look like a good buy for the long term.