Taylor Wimpey Share Price Forecast November 2021 – Time to Buy TW Shares?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The share price of UK homebuilder Taylor Wimpey (LSE: TW) was trading slightly lower in early London price action after the company released its trading update.

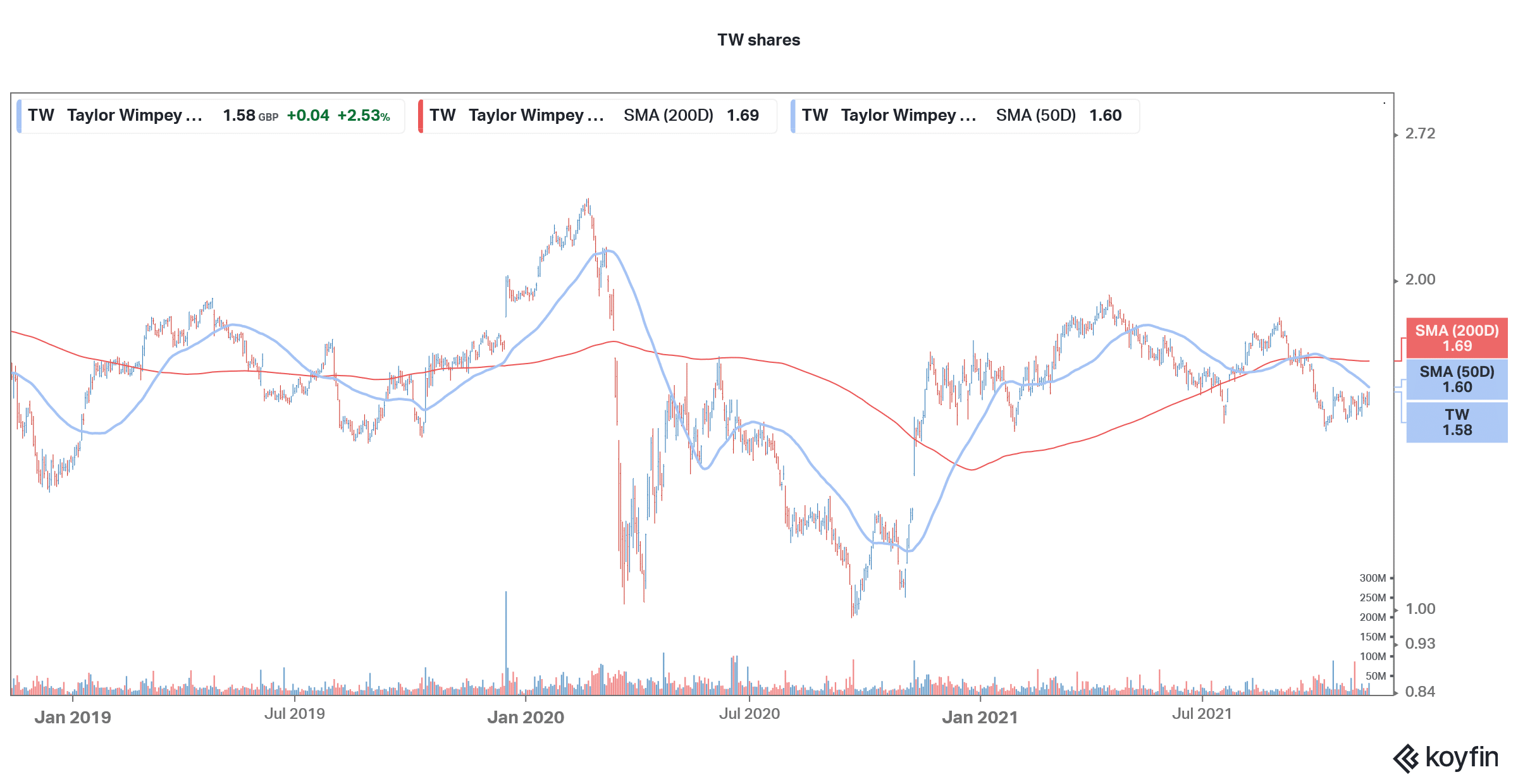

The shares trade with a YTD loss of 4.7% and are underperforming the broader markets which are limping back towards pre-pandemic highs. TW shares are down over 26% from their 52-week highs and are in a bear market territory after having fallen over 20% from the peaks. What’s the forecast for Taylor Wimpey shares and should you buy the dip?

Taylor Wimpey released the trading update

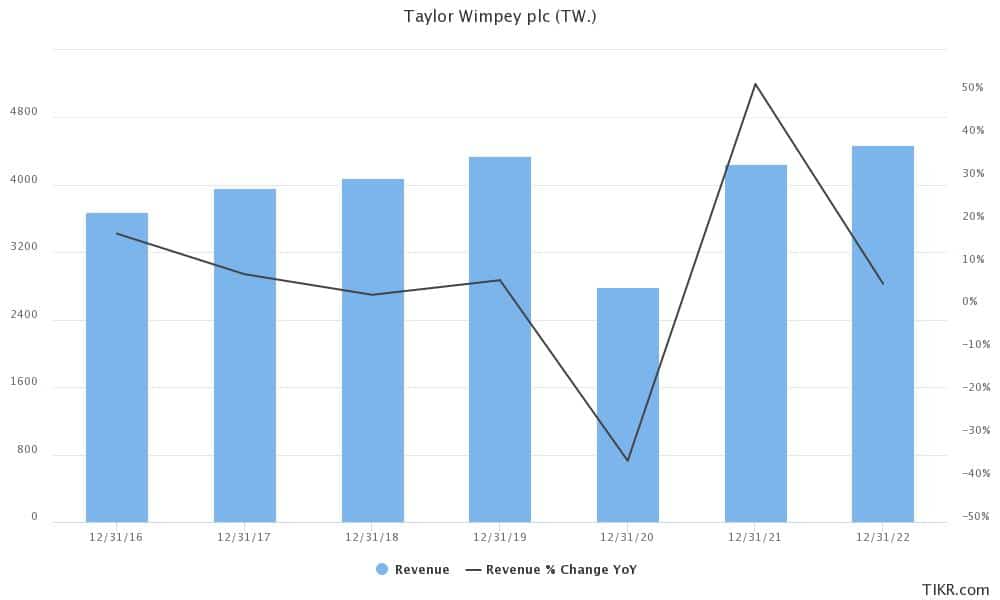

Today, Taylor Wimpey released its trading update for the second half of the fiscal year. It achieved a sales rate of 0.91 per outlet per week during the second half of 2021, which is similar to the 0.93 that it reported in the corresponding period in 2019. The metric has jumped sharply from 2020 but that’s basically due to the lower base effect.

The year-to-date cancellations were 14% and were in line with long-term averages. For instance, the cancellation rate was 15% in 2019. The opening of new outlets has also been in line with estimates and it opened 64 new outlets in the year as compared to 76 in 2019.

“Our sales rate has remained strong, and we are currently closing sales outlets ahead of schedule, with completions on these sites continuing into 2022,” said Taylor Wimpey in its release.

TW adds to its land bank

Between July and October, Taylor Wimpey added 5,431 plots to the short-term land bank which took the total short-term land bank to almost 84,000 plots. The company’s strategic land pipeline is close to 148,000 plots. Commenting on the land bank, TW said, “Our landbank will continue to grow as we process incremental land deals agreed following our equity raise in June 2020.”

Taylor Wimpey maintained its guidance

Taylor Wimpey maintained its annual guidance of 17,000-18,000 annual completions. The company is prioritizing operating profits and expects to deliver an operating profit margin between 21-22% in the medium term.

Commenting on the outlook, TW said “Market conditions remain supportive for new build homes, with continued low interest rates, good mortgage availability, and ongoing Government support for the housing market, particularly for first time buyers.”

Supply chain issues

Meanwhile, like almost all other companies, Taylor Wimpey is also grappling with the global supply chain and labour shortage. However, the company sees the situation getting better now.

“There has been easing in certain areas, and going forward, we expect conditions to gradually improve as suppliers adjust to current demand levels. We continue to effectively manage these pressures, aided by our scale and strong partner relationships and agreements,” it said in its release.

Like other homemakers, Taylor Wimpey has also seen cost-push inflation as prices for key inputs like steel, aluminium, and cement has surged over the last year. Higher wages are also adding to inflation for companies. Meanwhile, TW said that higher home prices are offsetting the build cost inflation.

The pass-through of inflation would lead to stickiness in inflation and the UK central bank might have to act quickly to tame higher prices. However, its hands are tied amid concerns over a sagging growth. The UK GDP growth slowed down in the September quarter amid the supply-chain issues.

Taylor Wimpey share price forecast

Analysts seem bullish on Taylor Wimpey shares. It has received a buy rating from 17 of the 19 polled by the Financial Times. One analyst each rates it as a hold and sell. TW has a median target price of 210p which is a premium of almost 33% to current prices.

The UK housing market is expected to continue its recovery in 2022 also. However, there are several headwinds for the sector including a possible hike in mortgage rates.

Taylor Wimpey technical analysis

Taylor Wimpey shares are not looking bullish on the charts and trade below the 50-day, 100-day, and 200-day SMA (simple moving average). However, the shares are trading above the short-term moving averages like the 10-day, 20-day and 30-day SMA. The shares are facing resistance at the 50-day SMA and need to cross above the trendline to indicate some technical strength.

However, the 12,26 MACD (moving average convergence divergence) gives a buy signal while the 14-day RSI (relative strength index) is a neutral indicator.

TW shares look attractively priced

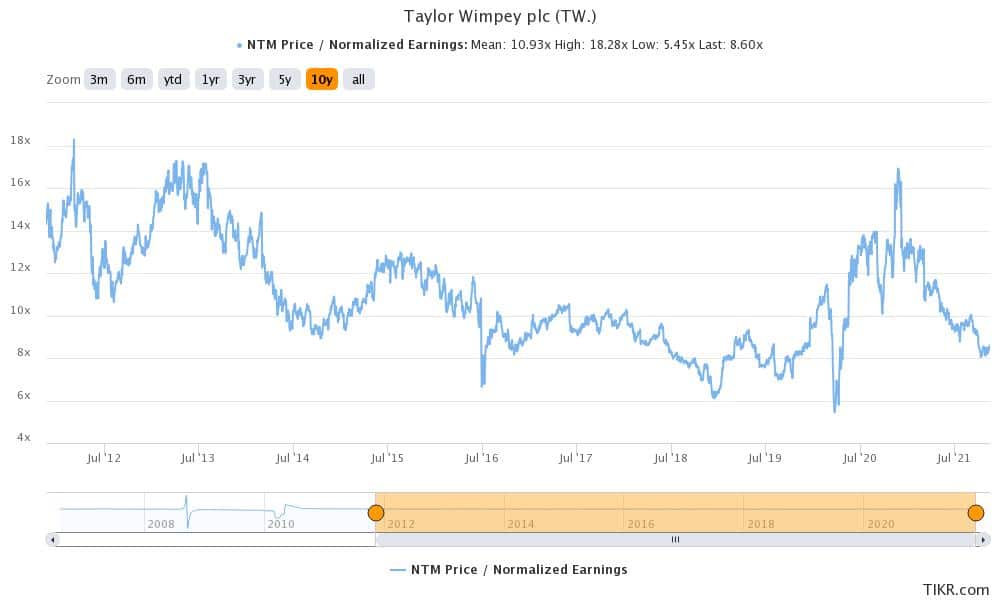

Taylor Wimpey shares trade at an NTM (next-12 months) PE of 8.6x. The multiples have averaged 9.6x and 10.9x over the last five years and ten years respectively. The valuation discount to the long-term averages looks like a good opportunity to buy the shares.

Also, if you are looking at a dividend-paying stock, TW could be a good bet with its 5.4% dividend yield which is almost four times the S&P 500’s dividend yield.

The shares look a bit risky in the short term considering the expected increase in mortgage rates. However, after the recent correction, most negatives seem baked in the prices. While Taylor Wimpey shares might remain weak in the short term, they should rebound in the medium to long term. The attractive dividend yield also adds to its investment proposition.