The Return of the Rater

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

27 April 2011.

Standard and Poors’ decision to cut its outlook for US debt to “negative” came as a surprise to many market watchers. The unprecedented move has reaffirmed the role rating agencies have in determining the prospects of national economies, much to the chagrin of many politicians. One main reason the S&P’s pessimism rattled markets was its novelty.

27 April 2011.

Standard and Poors’ decision to cut its outlook for US debt to “negative” came as a surprise to many market watchers. The unprecedented move has reaffirmed the role rating agencies have in determining the prospects of national economies, much to the chagrin of many politicians. One main reason the S&P’s pessimism rattled markets was its novelty.

Since it began issuing reports on the outlook for US bonds in 1989, the agency had not once suggested it could lower the “AAA” rating of the world’s largest economy. Now S&P warns the chances the US will lose its bulletproof credit vest are one in three over the next two years.

According to its estimates, the US debt-to-GDP ratio will range from 80 percent to 90 percent by 2013. The main concern focuses on continued political intransigence in Washington and the divisive nature of US presidential campaigns. Prospective republican candidates are already toeing the political waters and lambasting President Barack Obama even though the election is still 19 months away.

The chance that Republicans and Democrats could remain deadlocked on fiscal policy to reduce the deficit and debt or introduce a plan that will fall short has left the agency no choice but to tell investors that the US may become an unreliable borrower.

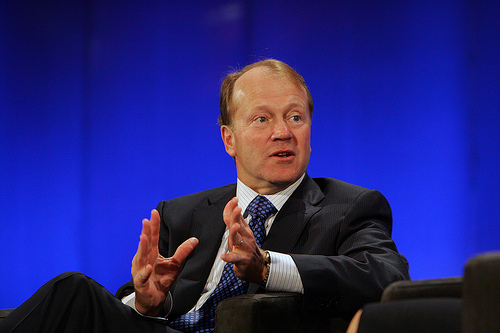

During a conference call after the announcement, John Chambers, an S&P managing director and chairman of the sovereign ratings committee, said the downgrade focuses on one thing: “The capacity and willingness of an issuer, in this case, of a government, to pay its debt in full and on time.”

Opinions on the announcement have varied widely. US Treasury Secretary Timothy Geithner took the rah-rah route by saying there is “no risk” of his country’s bonds losing their current status. One of his subordinates said S&P had “underestimated” the ability of US politicians to reach across the aisle and take the necessary steps to reduce overspending and pare what it owes.

Then the private sector weighed in.

Maverick investor Jim Rogers told Investment Week that the US will lose its AAA rating due to the country’s rising debt. Deutsche Bank’s economists suggested S&P may not have gone far enough. In a report, they equated the riskiness of owning US debt “about on a par with the euro periphery.” Based on economic fundamentals, Deutsche Bank says the risk rating for US public debt is higher than Spain’s.

The report even warned that in 2013, the US bond market could face a “Minsky moment.” The term is based on an economic theory that suggests a massive sell-off of certain investment products following a long bull market during which investors take increased risks, and it has happened recently.

The time was April 27, 2010, the place was Greece and the spark was an S&P downgrade of the country’s bonds to non-investment grade, i.e., junk.

It looks S&P made the right call. Eurostat, the European Union statistics office, announced Tuesday that Greece’s 2010 deficit was higher than expected, and the country’s debt last year reached nearly 143 percent of GDP.

The sector needs even more such correct predictions. Agencies have been criticized for overrating a range of corporations ahead of the 2008 collapse of the the US real estate market and a number of US banks, and the economic soothsayers have been trying to regain their credibility ever since.

Their gimlet-eyed views on the prospects of the eurozone periphery have been a boon to investors and the bane of European politicians. One of their most vocal critics in Europe funnily enough also runs the worst debtor in the eurozone. In a statement on a Greek government website late last week, Prime Minister George Papandreou said ratings agencies “are seeking to shape our destiny and determine the future of our children.”

This was just the latest salvo in his ongoing attacks on the messengers at a time when he should probably be using his time to deal with his country’s out-of-control spending. The EU has weighed in, too. A spokesman said the European Commission does not agree with S&P’s most recent downgrade of Greece, which lowered the country’s rating to BB, two short steps above “highly speculative.”

Unfortunately, ratings agencies may have reached their apex in Europe. The EU is currently finalizing regulations for the industry, and lawmakers are reportedly considering making raters liable for inaccurate downgrades. This could force their exodus and leave European debt an even riskier investment.

Read The Deutsche Bank report.

Eric Culp

EconomyWatch.com